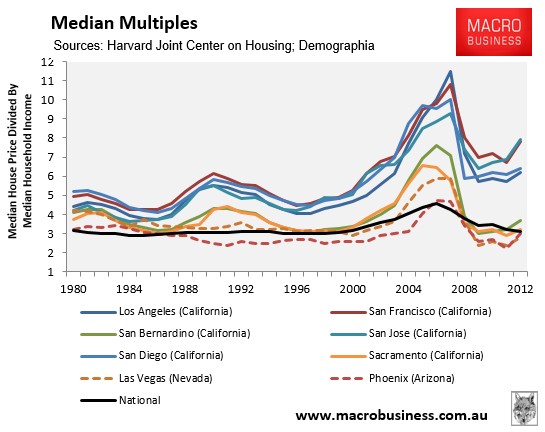

When analysing the 2000s US housing bubble, a handful of states stand-out for the way in which home values rose into the stratosphere before crashing and burning. Included amongst these are California, Nevada, and Arizona, where house values rose particularly aggressively and then fell sharply as demand collapsed (see next chart).

While many readers will disagree, the key factor that separates these bubbly markets from those where values rose less aggressively is that land supply was restricted via a combination of strict planning and geographical barriers (California), or a lack of private developable land (as was the case in Nevada and Arizona) due to high levels of ownership by the federal, state and/or Indian communities (thus creating a virtual growth boundary). These constraints on land supply effectively acted to steepen the supply curve for housing, resulting in faster price rises as demand rose and then steeper falls as demand fell away.

Advertisement

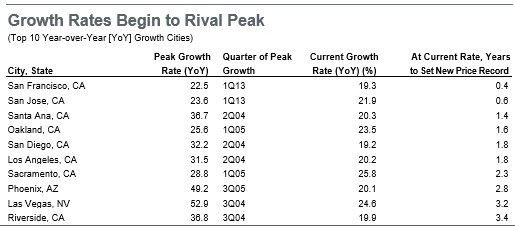

Overnight, Fitch Ratings Agency released its quarterly Sustainable Home Price and Economic Risk Factor Reportwhich warns that history may be repeating itself, with several cities across California, Nevada and Arizona once again approaching inflated bubble-year peaks:

U.S. home prices have risen 13%. However, Fitch sees the growth as unsustainable. In fact, national prices are approximately 17% overvalued as per Fitch’s Sustainable Home Price (SHP) Model. Many of those cities, not surprisingly, are in California, according to Director Stefan Hilts.

‘Home prices in San Francisco have gone up over 20% year-over-year, the highest rate of increase than at any point in the last 10 years,’ said Hilts. ‘In fact, San Francisco and San Jose will set new home price records in the next six months.’ Fitch’s SHP model currently identifies much of coastal California to be more than 20% overvalued. Other California cities nearing bubble-year peaks include Oakland, San Diego and Los Angeles.

Perhaps the biggest concern is that recent home price gains appear to be the product of rising investment sales and practices such as ‘flipping’ (buying and selling a home within a short time). All-cash sales have risen dramatically since last year and are now at nearly 50%. ‘Cash sales are often indicative of investor behavior so the concern is that home price increases are being driven more through speculative buying than from increasing demand,’ said Hilts.

Broadly speaking, home price growth is pushing through despite rising interest rates, which is starting to affect the affordability of new mortgages. Since May, rates have risen to 4.3%, though the effects of this increase which have not yet manifested in the latest available home price data. Fitch expects interest rates to continue rising through next year, which will strain affordability if home prices remain elevated and are still growing.

…based on the historic relationship between home price levels and the primary drivers of supply and demand in the market, there is a misalignment. A continuing recovery and exuberant home-buying population could well push prices further for many more quarters, or even years. However, Fitch identifies a bubble risk in continuing price rises and sees several factors which could halt or even reverse recent gains in the market.

Fitch is particularly concerned about Coastal California, which avoided the worst of the downturn, but is now participating fully in the recovery and recording rapid price growth. Moreover, much of this growth appears to be driven by speculators rather than by fundamental demand:

Advertisement

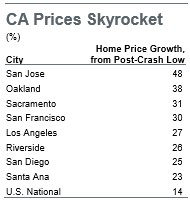

In San Francisco, prices hit a bottom in 2009 at nearly 125% above 1995 prices and have grown another 30% from that point. In San Jose, prices are up 48% from their post-crash trough and are now only 11% away from setting new highs…

Most concerning, there is growing evidence that recent gains have been bolstered by an increase in investment sales, both to institutions and local investors. Buying a selling a home within a short time window (flipping) is on the rise and the percentage of all-cash sales has risen dramatically from a year ago, standing now at nearly 50%. Cash sales are often indicative of investor behavior and the concern is that housing prices are being driven up more through speculative buying than from an increasing base demand…

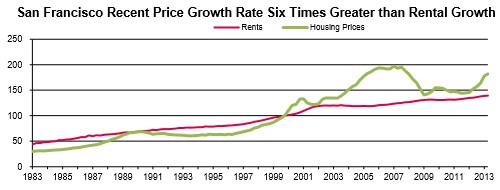

…increases in home prices have significantly outpaced growth in rents. In the past year, as prices have risen by 20% in San Francisco, rent costs rose by only 3%. In absence of rental yields or other significant economic growth as a driving force for price gains, there will remain concern that current growth levels are unsustainable.

They say history never repeats. But in the case of the US housing market, it sure does rhyme.

The full Fitch report can be downloaded for free (after registration) here.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.