Negative gearing allows taxpayers to deduct any losses they make on investments (including mortgage interest) from their overall income when they calculate their tax liability.

Under the proposed reform, investors would no longer be able to deduct these losses against wage income. However, they would be able to carry forward any losses and deduct them against any capital gain they make when the investment is sold.

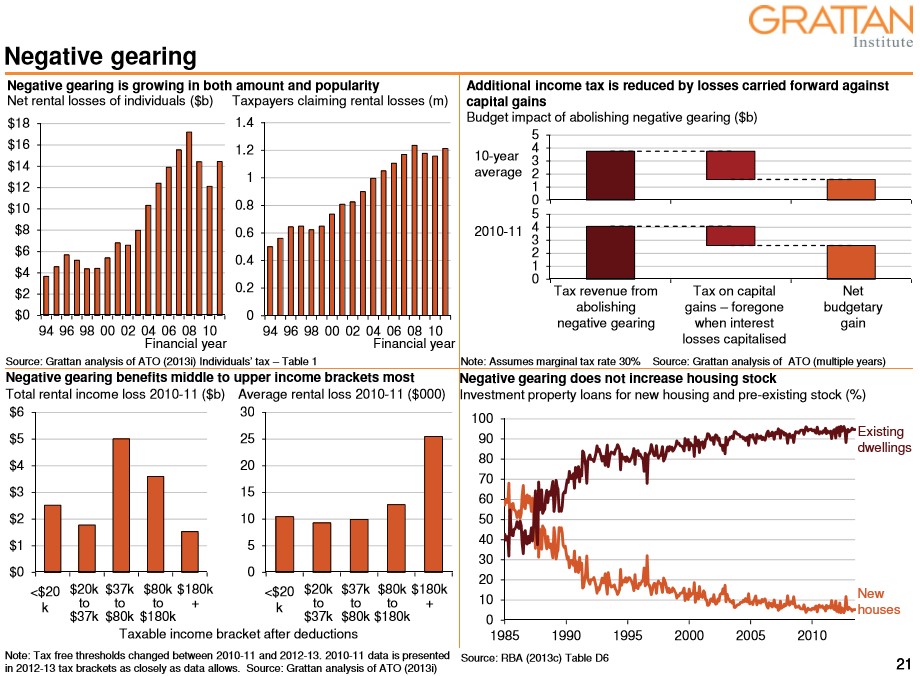

The proposal would contribute about $4 billion a year to the budget in the short term, falling to approximately $2 billion a year in the long term as losses accumulate, reducing capital gains tax.

If the proposal induced property investors to invest in other assets, tax revenue would be even higher. Alternative investments will not usually produce a tax deduction against income – indeed any switch to investments that generated a positive return would increase the tax collected.

Advertisement

Grattan highlights a number of non-budget (social) benefits from reforming negative gearing, namely:

increasing home ownership rates by reducing returns at the margin for landlords relative to first homebuyers; and

increasing investment in other more productive assets.

The report also debunks claims that reforming negative gearing would raise rents, since “for every landlord that sells, there would be a renter that buys and becomes a home-owner. The supply of rental properties would fall at the same rate as the number of renters”. It also does not believe that the construction of dwellings would be materially affected, since “almost all of investment property loans are now for existing dwellings”.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.