Citi has note out today looking at the effects of Dalian iron ore futures:

Interest in physical arbitrage between the Dalian contract and non-customs cleared ore (tracked by TSI and IODEX indices) is high. Differences in treatment of alumina and Fe content provide additional opportunities even beyond normal arbitrage trading. However, the lack of a cap on water content presents a danger that undesirable ore will be delivered, impairing the utility of the exchange as a physical market mechanism.

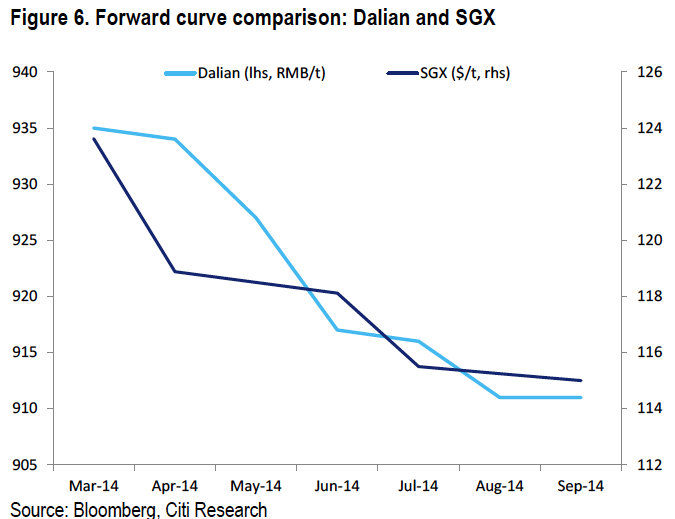

The launch of Dalian iron ore futures has boosted trading in SGX iron ore futures, but has not done the same for swaps or options. It raises the prospect of futures trading overtaking swaps thanks to arbitrage trading between Dalian and SGX. However, the concentration of trading on three contracts per year in Dalian will hinder this process. Arbitrage trading between Dalian futures and international futures & swaps contracts is likely to be more complex than that seen for copper, gold, and other commodities due to differences in underlying terms between Dalian and the TSI (and IODEX) index.

The availability of domestic iron ore futures has also boosted trading for SHFE rebar, Dalian coke, and Dalian coking coal futures. The availability of such futures offers mills the ability to hedge the most important components of their operating margins (this can also be done via international iron ore securities combined with FX swaps), providing a powerful tool to control risk akin to that utilized by soybean crushers and international oil refiners.

Hmmm, much of the press has focussed on the question of whether or not the index will give China more pricing power over iron ore. Futures are a vexed question for me but in theory at least they should reduce volatility in the underlying market price given they provide speculators an opportunity to trade a commodity without physically hoarding it. That doesn’t mean they’re any less likely to form bubbles or drive prices to extremes at times – that is, the underlying price discovery is not improved at all – but it does mean less boom and bust.

To that extent, Dalian futures could encourage a further drawdown in the steel mills iron ore inventory levels over time and perhaps mitigate stocking cycles without exposing them to the whim of the Australian cartel. In an environment of expected supply increases that will drag the price lower more smoothly but not necessarily more quickly.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.