The July PMIs are all in now and, with developed counties rebounding, the impression given is that global growth is beginning to accelerate. Let’s test that thesis. Here is the JPMorgan Global Manufacturing PMI:

The global manufacturing sector made a subdued start to the third quarter. At 50.8 in July, the JPMorgan Global Manufacturing PMI™ – a composite index* produced by JPMorgan and Markit in association with ISM and IFPSM – remained only slightly above the no-change mark of 50.0.

Rates of expansion in production and new orders were broadly unchanged from the modest levels signalled during the second quarter of the year. July nonetheless saw output and new orders rise for the ninth and seventh successive months respectively.

National PMI suggested that the Asia region was the main drag on global manufacturing growth during July. Production volumes declined in China, India, Taiwan, South Korea and Vietnam, stagnated in Indonesia, while growth slowed to a five-month low in Japan. Elsewhere, Spain, Brazil, Russia, Mexico, Australia and Greece also reported contractions.

In contrast, output growth hit a four-month high in the US, near two-and-a-half year high in the UK and returned to

expansion for the first time since February 2012 in the eurozone. Eastern Europe also faired better, with production rising in both Poland and the Czech Republic. The upturn in Canada extended into its third successive month.

So, growth in manufacturing is roughly where it was eigtheen months ago but the mix is different with emerging markets the major drag and developing economies the major growth force. Now services:

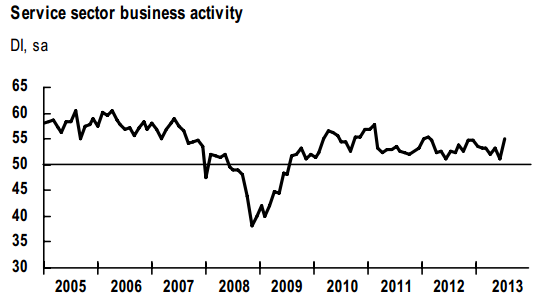

July PMI data pointed to a solid acceleration in the rate of expansion of the global service sector. However, this was largely centred on the US, as the rate of increase outside of the US was (on average) broadly unchanged from June.

At 54.9 in July, the JPMorgan Global Services Business Activity Index – a composite index produced by JPMorgan and Markit in association with ISM and IFPSM – rose to a 17-month high. Moreover, the month-on-month gain in the headline index (3.8 points) was the sharpest since February 2008. The latest expansion extended the current sequence of growth to four years.

Growth in the US surged to an seven-month high in July, and hit a six-and-a-half year peak in the UK. The eurozone moved to the cusp of stabilisation, as the expansion in Germany accelerated and the downturns in France, Italy and Spain all eased. Asia was a weaker spot, however. The upturn in Japan eased to a nine-month low, growth was unchanged in China, while India and Hong Kong both reported contractions. Russia also saw output fall.

Advertisement

Same story then. Global services growth is back to where it was 18 months ago but the mix has reversed. Finally, global growth itself:

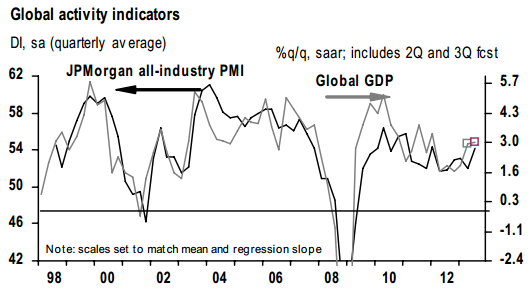

Global economic growth accelerated sharply at the start of the third quarter. The rate of expansion in output hit a 16- month high, as manufacturers and service providers benefited from improved inflows of new business.

The expansion remained uneven by region, however. Stronger growth was registered in the US* and the UK, while the eurozone stabilised. This was partly offset by weaker performances in Asia and a number of emerging markets. The Global All-Industry Output Index – produced by JPMorgan and Markit in association with ISM and IFPSM – posted 54.1 in July, up from 51.2 in June, to extend the current unbroken sequence of expansion to four years.

Rates of output expansion in the US and the UK were the fastest for seven months and 16 years respectively. Moreover, the all-industry PMI output indices for both the US and the UK were almost ten points higher than the average for elsewhere in the global economy. Output growth in Japan eased to a five-month low, while contractions were signalled for China, India, Brazil and Russia.

That’s be bye, bye BRICS and hello Anglosphere!

Advertisement

A number of different factors are at work here. The Anglosphere currency wars and austerity drives have increased competitiveness for years. As well, the BRIC block and emerging markets’ competitiveness generally has eroded sequentially on high inflation and rising currencies since the GFC.

As result, European export growth is now rising, the US less so but emerging market export growth has been falling steadily and that suggests that there are also big (bigger) dividends for developed market growth in import competing sectors.

A final factor at work has been the revival of developed economy housing markets which will put a rocket under service sector growth.

If developed economy authorities can exit their stimulus programs without crashing the edifice (one huge IF) and developing economy authorities can manage their transitions to internal demand (another huge IF), the new trend can take the globe to a better and more sustainable economy.

Advertisement

The globe is probably setting up for modestly better growth at around 2.5-3% in the year ahead. Not tearaway but reasonable. More importantly, it is growing differently, undergoing the very same rebalancing that is coming to China, and Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.