JP Morgan has a bullish note out for iron ore that is worth a read.

Despite market concerns over a repeat of the significant price correction that occurred in the third quarter of last year, we see no evidence of seasonality in iron ore. We believe Chinese port inventories are currently too low to cause the destocking event that resulted in the September 2012 crash. Furthermore, an update to our iron ore cost curve analysis incorporating higher China steel production sees marginal costs remaining above US$125/t to at least 2015.

No apparent seasonality in iron ore: In this note, we have looked at seasonal trends in China steel production, iron ore imports, steel inventories, and port stocks. With the exception of China steel production, which typically peaks in the summer months, there is little evidence of any seasonality in the other data series.

The destocking event that drove iron ore prices lower in 2012 is not likely this year: In 2012, a significant port destocking event caused iron ore prices to decline materially in the second half of the year. Iron ore stocks at Chinese ports peaked at 100Mt in July 2012 but subsequently declined 25% to 75Mt in April 2013. While this led to a significant decline in iron ore prices in the third quarter of 2012, the capacity for this to reoccur in 2013 is very limited given current port stocks remain low at 76Mt.

Updating our cost curve analysis: Within this note, we have also taken the opportunity to revisit our iron ore cost curve analysis, which we last published in March 2013. Significantly, our recent research (link) suggested that Rio Tinto’s Pilbara 360 Project is likely to reach capacity later than previously expected pushing out the “wall of supply.” Furthermore, with China steel production annualizing at 800Mt in the first half of the year, our China Metals & Mining team has increased J.P. Morgan’s forecasts, with positive implications for iron ore demand.

Marginal cost analysis suggests prices will remain high for longer: Incorporating our latest forecasts into the cost curve model implies marginal cost of production will remain above US$125/t CFR China to 2015 and above US$100/t to 2020 (see Table 1on page 6). We note this is well above our current house forecasts implying upside risk to our estimates.

Australian iron ore producers likely to be the greatest beneficiaries: Given a weakening A$, we believe the Australian producers are likely to be significant beneficiaries of stronger iron ore prices.

Regular readers will know that I’ve already softened my own view on the Q3 falls this year. Of greater interest here is the contention that supply is coming on more slowly and demand rising more swiftly than previously thought.

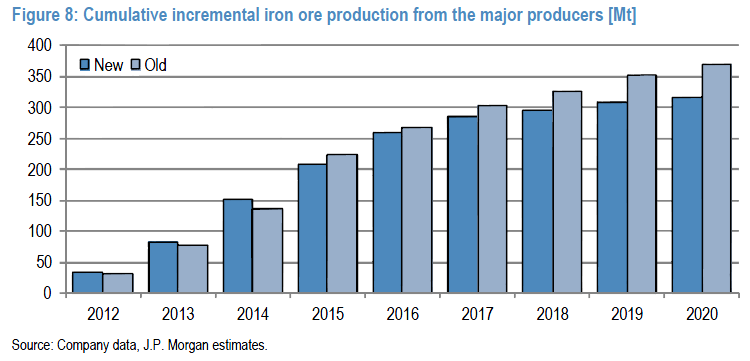

Iron ore production growth forecasts have been reduced again

Figure 8 below shows the incremental production growth from Vale, Rio Tinto, BHP Billiton, Fortescue, the Australian small cap iron ore stocks, and West Africa that we have used in this analysis.

As shown in the chart, the slower than expected ramp up of Rio Tinto’s Pilbara 360 project (as detailed in our report of 10 July 2013 – Pilbara 360 – a detailed review of project options and key issues facing management) results in lower production forecast from 2016-20.

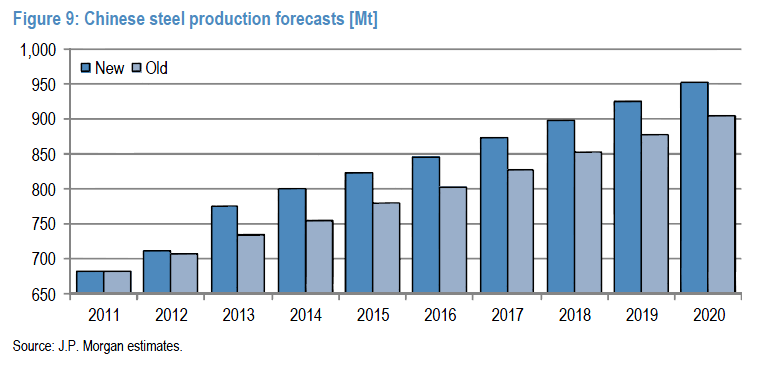

Chinese steel production growth forecasts have increased

As shown in the table below, our J.P. Morgan house forecasts for Chinese steel production growth have increased significantly since our last update. With production rates annualizing at 778Mt year-to-date, we now forecast China steel production of 775Mt in 2013 (versus 735Mt previously), and 801Mt in 2014 (versus 755Mt previously).

Advertisement

Do these change my view of the coming price adjustment? The steel production growth rates are ahead my own but not aggressively. They’re three percent and trending down. The Chinese are committed to reducing this over-production. Actually succeeding in doing so is proving more difficult for any number reasons but I still expect them to get there slowly. So I expect a lower growth rate but JPM’s forecasts are not unreasonable.

Even if the higher steel production materialises it will be far short of the iron ore supply deluge for 2014-16. Basically, it’s 25 million tonnes of new demand per year versus 75 million tonnes of new supply. As the Chinese are clearly showing right now in its chronically over-producing steel sector, assuming that more expensive Chinese iron ore production will be swiftly displaced is a troubled notion so expect seaborne demand to slow.

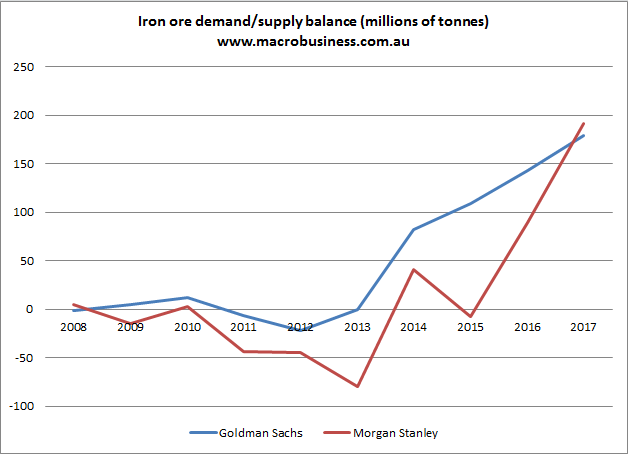

Whether you buy this bullish case really depends upon this underlying assumption, that demand for seaborne iron ore will grow strongly by displacing Chinese production. Here is my chart from GS and MS forecasts with Pilbara 360 removed completely:

Advertisement

The MS team has an aggressive 5% growth forecast for seaborne iron ore demand. GS sees it at 3% and declining. If you remove Pilbara 360 the difference is stark. For MS, the oversupply is mitigated (though not removed) for two years. This is the difference between iron ore at $110 and $80. My own view is that the GS figures are more accurate on the supply side and the MS figures for the growth in seaborne demand are too aggressive as China slows.

To my mind JPM’s delays to Pilbara 360 are questionable. The scenario in play is not one of mad miners running to produce. It’s a game of securing market share for the long-term future. If Rio doesn’t get some significant portion of Pilbara 360 to market by 2015 then others will move immediately to fill the gap and leave Rio with more competitors. I share the view of Deutsche Bank that it’s better to control more of the production in the long run.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.