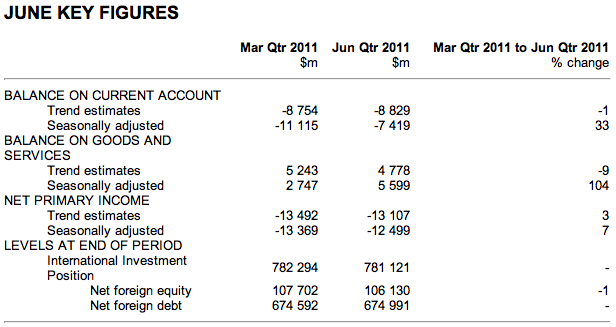

The Australian Bureau of Statistics (ABS) released current account figures for the June 2011 quarter (emphasis added) today:

In seasonally adjusted, current price terms, the current account deficit fell $3,696m (33%) to $7,419m in the June quarter 2011. Exports of goods and services increased $5,837m (8%) and imports of goods and services increased $2,985m (4%). The primary income deficit fell $870m (7%).

In seasonally adjusted chain volume terms, the net goods and services deficit rose $1,643m (19%) to $10,224m in the June quarter 2011. This is expected to detract 0.5 percentage points from growth in the June quarter 2011 volume measure of Gross Domestic Product.

Analysts had forecast a $7.1 billion deficit, instead of the $7.4 billion result and only a 0.1% reduction in GDP growth, not the 0.5% result.