Yesterday, Fairfax published an interesting article, Sell the family home: PM’s aged care shake-up, which highlights one of the key longer-term challenges facing the Australian housing market: the impending retirement of the baby boomers.

JULIA GILLARD will prepare the ground today for the biggest shake-up of aged care in decades with a speech calling for a more sustainable and flexible system to cope over the long term with the rapidly ageing population.

The Prime Minister will say Australia is about to have two senior generations – retired baby boomers and their parents – and she will point to the release next Monday of a major report by the Productivity Commission which is expected to recommend controversial measures to keep aged care sustainable.

These include selling the family home to use as a bond when moving into aged care.

The Herald understands the commission finds the cost of aged care is discouraging much-needed new investment in the sector to provide for the increase in the elderly population as baby boomers begin to retire.

Consequently, the cost of aged care will need to increase to create incentive to provide services. The commission is expected to recommend a raft of measures which include selling the family home to provide a bond, borrowing against the value of the home to pay a bond, or making periodic payments. In each case, a bond would be returned to the next of kin when the aged care resident passes away.

The retirement of the baby boomer generation, and the associated selling-down of their assets to fund retirement, is a topic that has received significant attention on this blog (for example, see here & here).

In a nutshell, the past 40 years has been a golden era for the housing market in Australia as the large baby boomer cohort – defined by the Australian Bureau of Statistics (ABS) as those born between 1946 and 1965 and comprising 25% of Australia’s population – first moved into home ownership en masse and more recently undertook large-scale purchases of investment properties and holiday homes as they reached peak earnings age of 45 to 54 years old (see below chart).

The baby boomer’s accumulation of Australia’s housing assets is illustrated by the most recent ABS Household Wealth and Wealth Distribution survey, which shows that the baby boomers hold 45% of owner-occupied dwellings and 51% of other dwellings (investment properties and holiday homes). Further, those aged 65+ hold a further 21% of Australia’s housing assets, taking the older cohort’s (those aged over 45) share of Australia’s housing stock to 67% (see below chart).

However, 2011 marks the year when the oldest members of the Baby Boomer generation – those born in 1946 – turn 65 and reach official retirement age. From each year going forward, the number of retirees in Australia is expected to grow significantly:

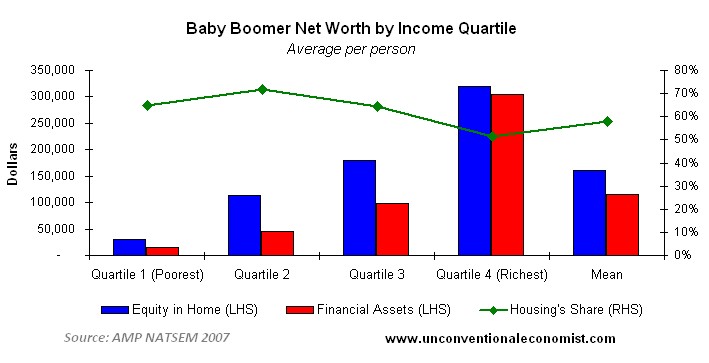

Since Baby Boomers are heavily exposed to housing and hold relatively little in the way of financial assets – certainly not enough to fund a comfortable retirement – it is highly likely that many will look to sell their investment properties/holiday homes and/or downsize in order to finance their retirements. The reforms to aged care flagged in the above Fairfax article will only exacerbate these trends.

{kind=link}

The incentive to sell-out of property will also likely intensify once the baby boomers realise that there is every likelihood that home price will stagnate or fall over the foreseeable future and that superior risk-adjusted returns can be achieved by investing in cash and fixed interest. These incentives to sell will be maximised where investment properties held by the boomers are negatively geared, which is: (i) a loss-making activity in a stagnant housing market; and (ii) no longer feasible once retirement is entered, since negative gearing requires taxable interest to offset losses with.

Therefore, demographic demand for housing is likely to slow significantly (albeit gradually) over coming decades as Australia’s population ages, which should act to slow house price growth.

Supporting evidence:

The above analysis is supported by a Bank for International Settlements (BIS) working paper, published last year, which examined the impact of changing demographics on asset prices (particularly housing) in 22 advanced nations over the next 40 years. The results suggested that ageing will lower real house prices compared to neutral demographics (i.e. where the age profile of the population remains constant) over the next 40 years in all 22 countries in the sample.

The below BIS chart, which shows the demographic impact on house prices over the past 40 years (1970 to 2009) and the next 40 years (2010 to 2050), is particularly relevant for Australia’s housing market.

According to the BIS, as the baby boomers reached working age and started buying housing from 1970, they helped to push-up property prices throughout the world. In Australia, over the past 40 years the Boomers increased real house prices by around 30% compared with what would have occurred had our age structure remained neutral. However, the ageing of the baby boomers is projected to reduce Australia’s real house price growth by around 30% over the next 40 years compared to neutral demographics. This is because the baby boomers will reduce their housing stock as they enter retirement by liquidating their investment property holdings and downsizing, thereby depressing house prices.

The impact of Australia’s changing demography on asset prices and investment is a topic that has to date received little attention from the commentariat. This is possibly because demographic shifts are inherently slow moving, so their impacts are gradual and tend to go unnoticed for extended periods of time. Nevertheless, these longer-term dynamics are significant and are likely to significantly alter the growth trajectory of asset valuations in the decades to come.

It therefore pays to consider Australia’s changing demographics when planning any long-term investments, as well as policy decisions that could exacerbate these trends.

unconventionaleconomist@hotmail.com