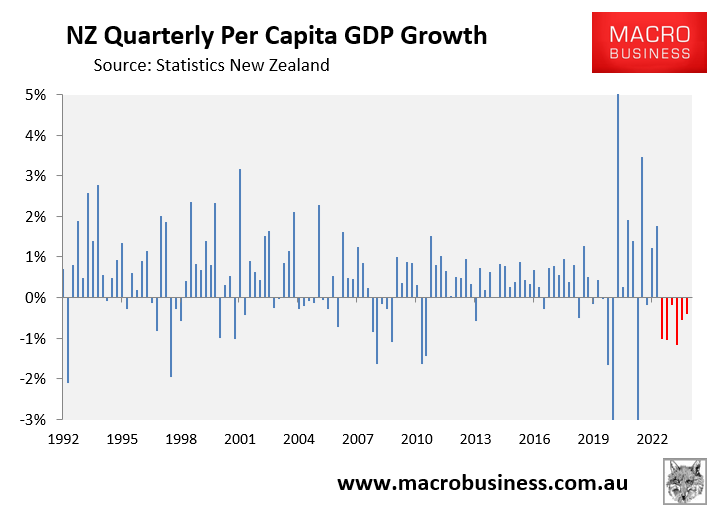

It’s been obvious for months that the New Zealand economy was falling apart. Six consecutive quarters of per capita recession do not lie:

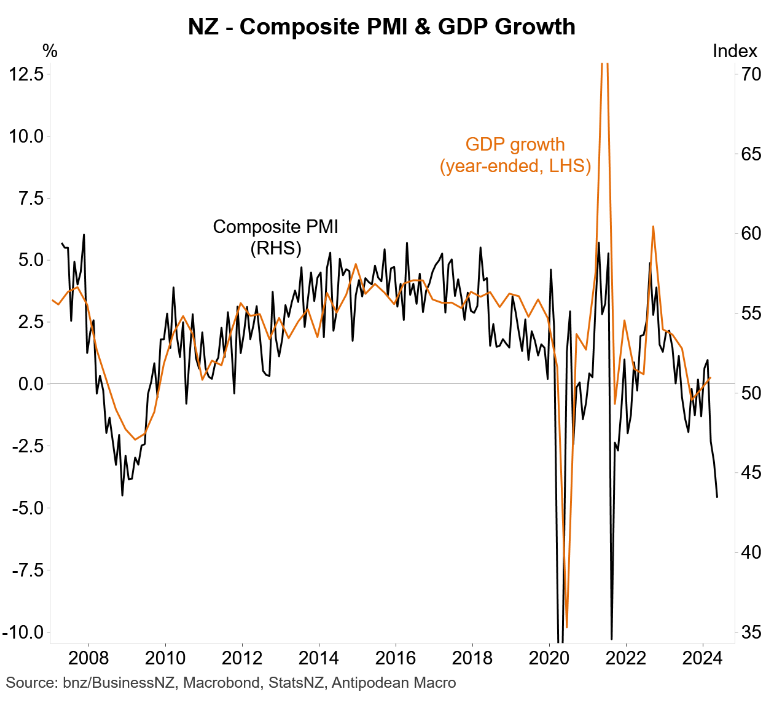

Leading soft data is even worse:

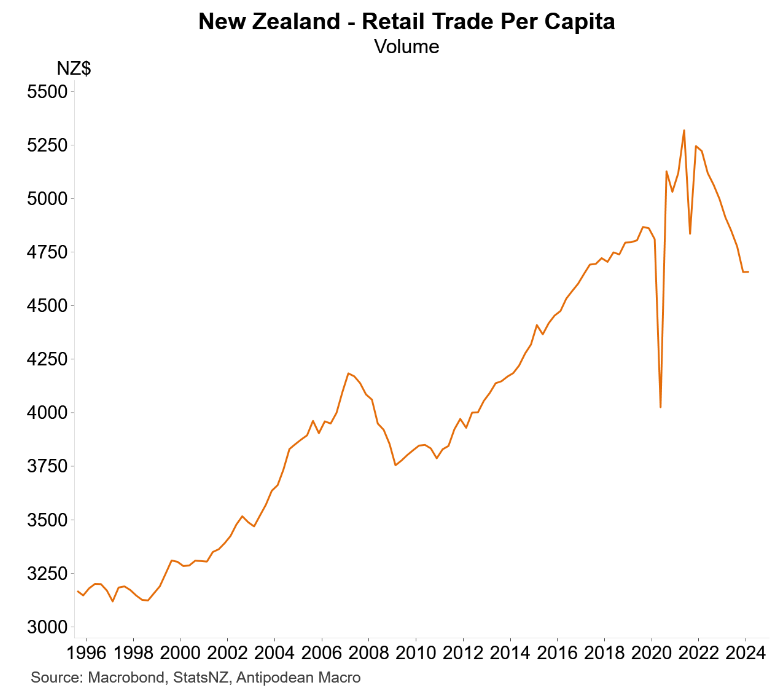

And households, the mainstay of the economy, long ago capitulated:

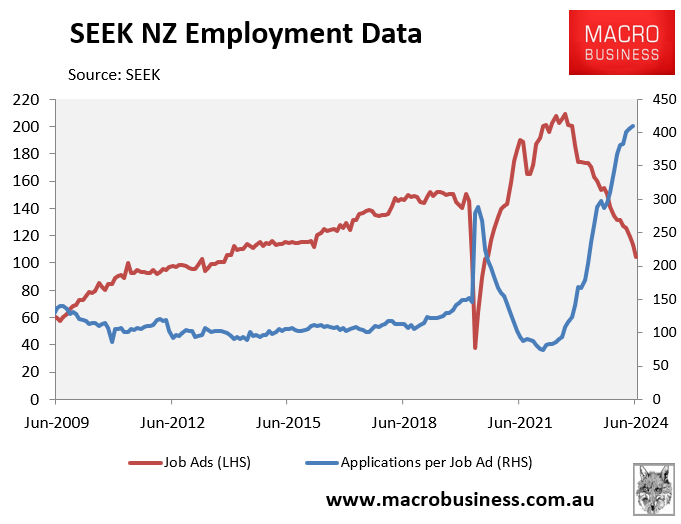

As did the labour market:

Given the degree of supply-side inflation, which was always going to revert, this demolition of demand was neither necessary nor wise.

Now Bloomberg finally gets something right by having a crack at overly hawkish RBNZ:

The Reserve Bank of New Zealand undertook a pivot for the ages. The authority went from projecting a very hawkish view of the world in May to executing a surprise quarter-point trim in its main interest rate — and intimating a meatier cut was contemplated.

It’s wise to shift when circumstances change, but have they really changed that much in three months? The economy has been in the doldrums for a while, in large part as a consequence of the aggressive tightening that began in late 2021. The slowdown is likely to be protracted. The RBNZ confirmed what many private-sector economists already figured: The country is facing not just a double-dip recession, but a triple crown.

…Orr could have done with expressing a little more empathy while cameras were rolling. What did the bank recognize now that wasn’t apparent last time, he was asked? Did officials make a mistake? He should have been prepared for such a grilling: It’s part of the modern central-banking game. He urged journalists to read the documents and reminded them — forcefully — that forecasting is an imprecise exercise. Abandoning the effort just because you might be proved wrong isn’t the solution.

Some of the discourse was unnecessarily combative and the responses cringeworthy. He came close to framing recession as a win.

The RBNZ should be cutting in 50bps increments and apologising while it does so.