Morgan Stanley with the note.

China – More signs of weakening

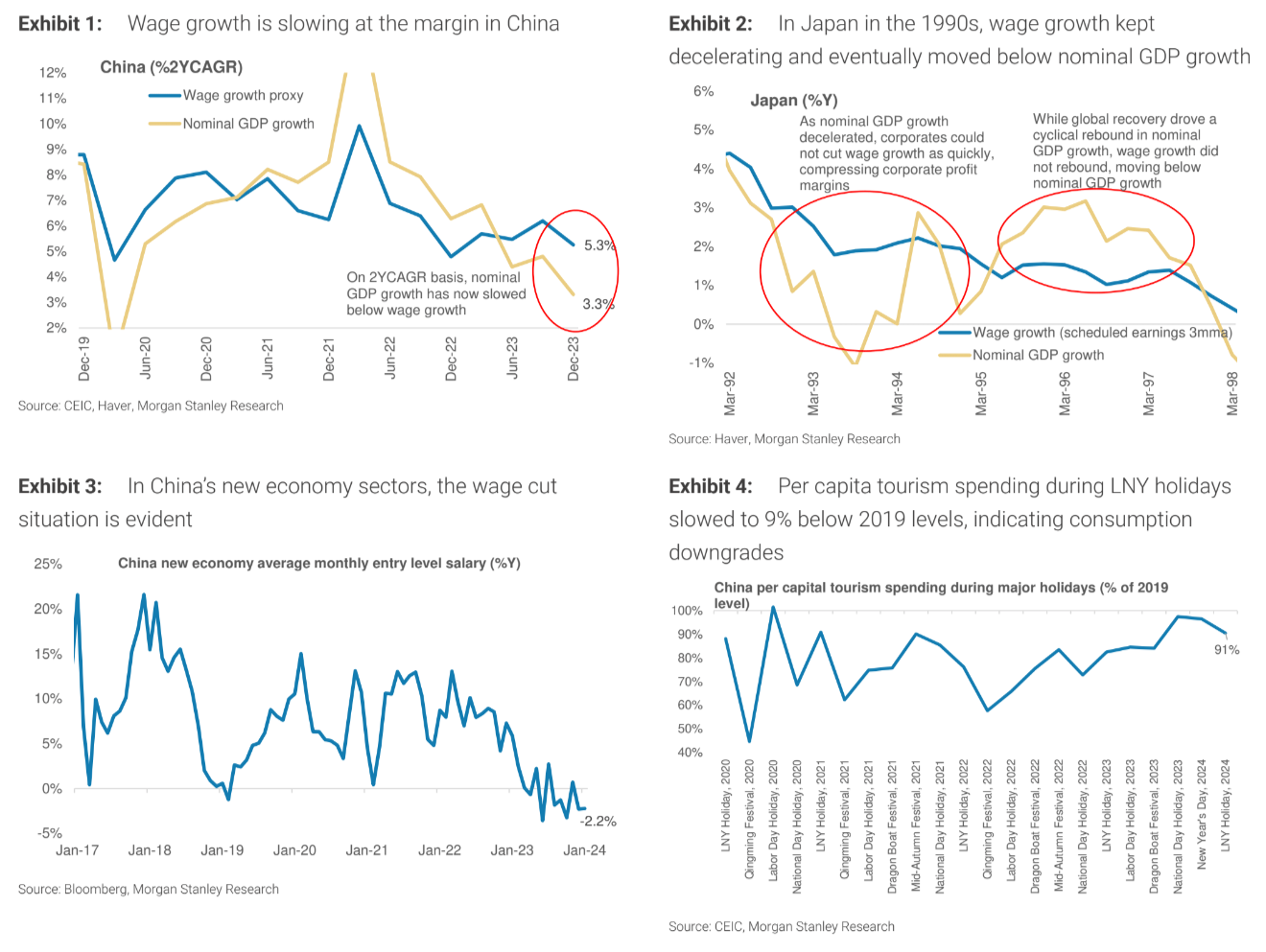

Wage growth has slowed: As it is, aggregate wage growth – proxied by household income– has already slowed to 5.3% on a 2YCAGR basis (to adjust for Covid-related base effects), down from 6.2% in 3Q23 and from 9% pre-Covid (2017-19 average).

While wage growth is still tracking above nominal GDP growth (Exhibit1), our past work suggests that in a deflationary environment like we saw in Japan in the 1990s, companies were initially slow to cut wage growth but eventually had to, so as to protect their margins.

Eventually in Japan, wage growth kept decelerating (Exhibit2) and reached a point where wages were adjusted only based on seniority with no increase in base-up component.

In China’scontext, nominal GDP growth has already slowed from the pre-Covid average of 9.8%Y to an estimated 3.3%Y in 1Q24, and so we believe that the corporate sector is under pressure to cut wage growth.

Indeed, wage cuts are being reported in certain sectors and segments of the workforce.

For example, according to media reports, there are wage cuts of 15-40% in the investment banking sector, as well as bonuses and base pay cuts by some local governments.

Migrant workers, which at ~300mn account for 31% of China’s working age population, have also faced wage cut pressures.

It is also the case that new economy sectors have now seen wage growth under pressure (Exhibit3).

According to Caixin data, the average monthly entry-level salary in new economy sectors declined 2.6%Y in Jan-24, and the premium of entry-level salaries over economy-wide salaries has narrowed to an 18-month low of 102.8%.

Similarly, according to data from China online recruitment platform Zhaopin, average new hire salaries offered in 38 key cities have also turned negative on a %Y basis since 2Q23, and tracked at -1.3%Y in 4Q23 amid elevated youth unemployment rates.

Weaker wage growth is impacting household spending and consumer sentiment: Our January AlphaWise Chinese consumer survey flagged that the risks of salary cuts and job losses remain top concerns for households.

With workers continuing to face downward pressure on wage growth, a deflationary mindset appears to be setting in with households responding with consumption downgrades.

For example, per capita tourism spending during the Lunar New Year Holidays slowed to 9% lower than in 2019 (Exhibit4), compared with just 2% lower than in 2019 during the National Day Holiday in Oct-23.

Our China consumer team has also cited weakness in spending in restaurants with a higher price point as evidence of a continued consumption downgrade trend.

Considering that we believe China needs to boost aggregate demand with consumption growth accelerating, this slowdown in wage growth will make it all the more challenging.

Risk of unanchoring of household wage and inflation expectations to the downside: As consumption slows amid weaker wage growth and asset price deflation (household wealth) and weighs on aggregate demand, this would result in deflationary pressures persisting in the economy.

The risk would be if households’ expectations for wage growth then become unanchored to the downside, it could continue to exert deflationary impulses on the economy.

Yep. As I keep saying, depression economics of this nature is being priced into Chinese yields and its yield curve:

Next up: unrest.