Societe General with the snippet:

This week, the RBA kept rates on hold (as expected), but the statement said that “a further increase in interest rates cannot be ruled out”. The market is still pricing half a cut in March, and the RBA’s explicit hawkish bias is at odds with most G10 central banks. As low FX vol tends to sustain a pro-carry environment, a higher repricing in AUD rates would benefit the currency.

Wrong. The RBA knows how sensitive its rate trigger is. Owing to floating rate mortgages, it is the most sensitive in the developed world. That’s why interest rates are so much lower than in the US.

Above all else, the RBA is a housing bubble manager. So, the bank does not want to give the all-clear for fear of rapid increase in borrowing even before cuts. So, it will keep the jawbone tight while its finger is on the easing trigger.

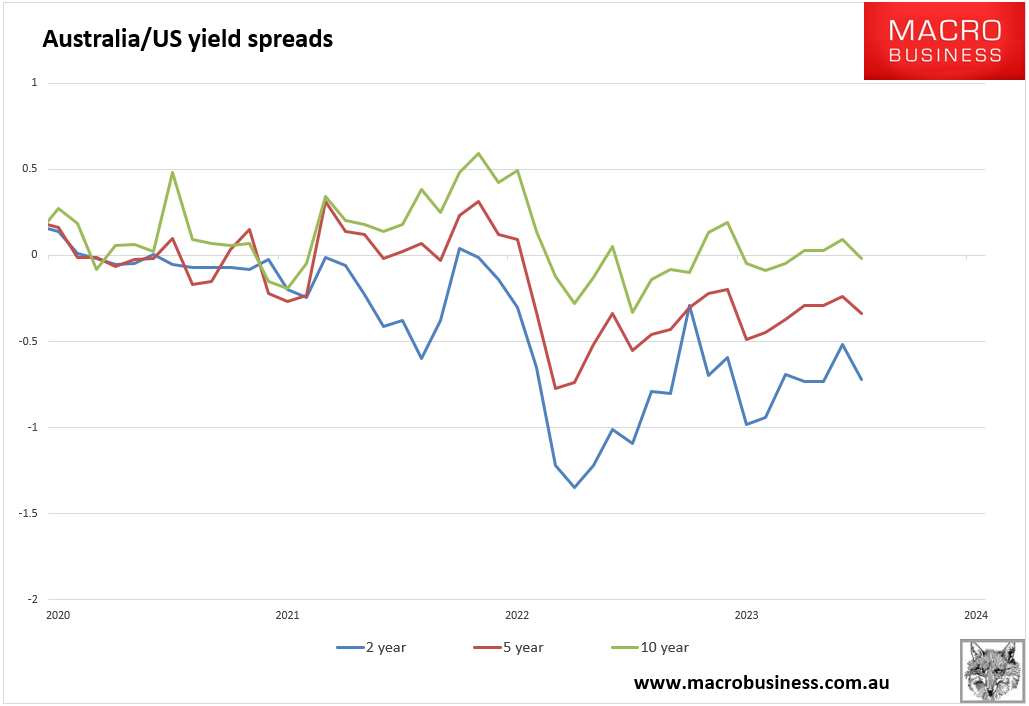

Bond markets since the last RBA meeting bear this out. Spread to the US have compressed and inverted at the long end:

This is the opposite of the RBA being more hawkish unless the market is pricing a policy error.

I don’t think so. The Aussie economy is much closer to Europe now than the US, and the RBA is shifting towards easing.

It will come suddenly and is not AUD bullish.