You wouldn’t know from the idiot MSM, but the AEMO reported last night that Albo’s coal and gas price caps have delivered significant falls in wholesale energy prices.

Here’s what Domain (and most others) reported:

A record-breaking volume of renewable energy has driven the price of electricity generation down 24 per cent, cutting the use of more expensive coal power and raising the likelihood of significant cuts at the next round of price-setting for household energy bills on July 1.

Here’s what the AEMO said:

Wholesale price pressures decreased with more capacity offered at lower prices

- Changing coal market conditions and policy interventions since last Q4 saw black coal-fired generators offering larger volumes of energy at lower prices, with an average additional 1,382 MW offered at price levels below $100/MWh. There was an increase in the frequency at which this generation set the price to 30% of dispatch intervals (from 28%), however this occurred at a much-reduced price of $58/MWh compared to $113/MWh in the same quarter last year.

- A record high of 20% of intervals experienced negative or zero wholesale spot prices across the NEM, with New South Wales and Victoria reaching their highest ever number of intervals with negative or zero prices, at 12% and 29% respectively.

In short, it was mainly coal that dropped prices, not renewables.

But hey, coal is cancelled, so lying is okay.

I’m not sure why the AEMO did not mention the year-on-year crash in gas prices, which was also critical to falling prices, not least because renewables increased their penetration, demanding more gas-fired power to fill the gaps.

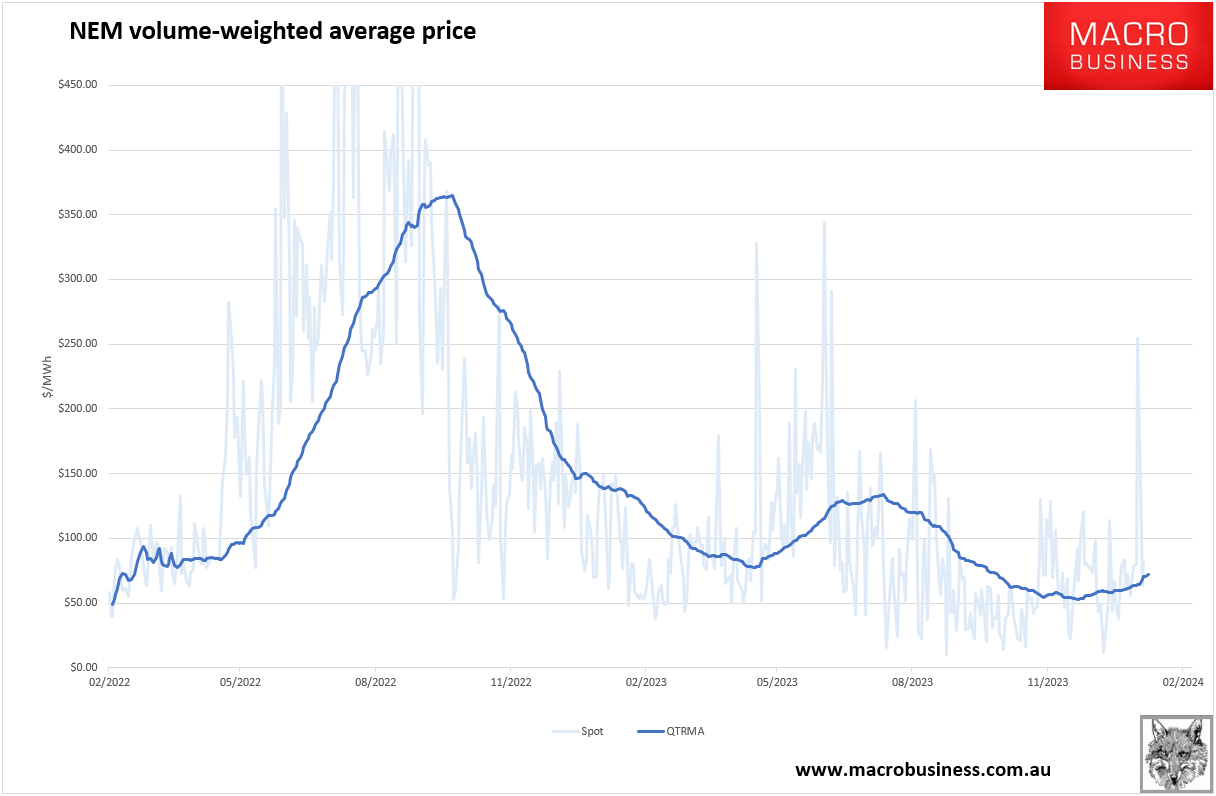

Speaking of which, as the iMSM makes stuff up, today’s power prices continue to climb:

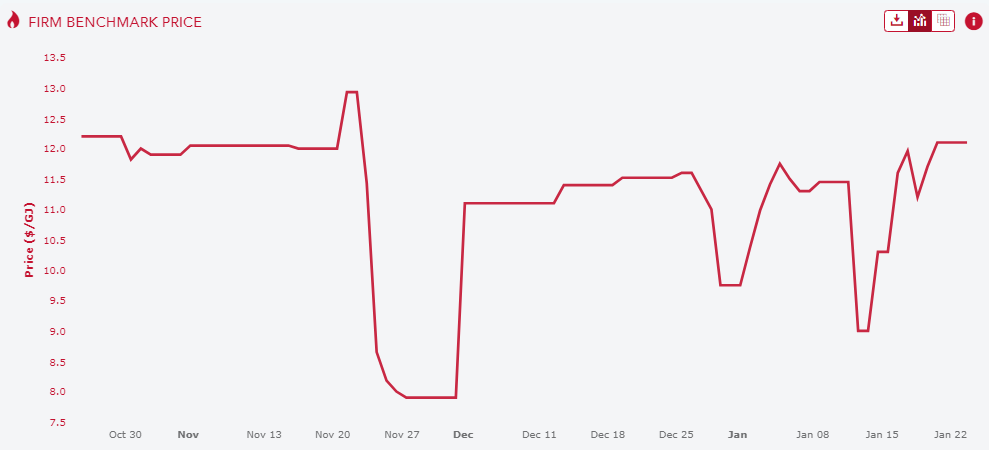

Because gas prices have rebounded since the Q4 dump:

These prices are above what you can buy Australian gas for in Europe thanks to a rampaging gas export cartel that is partying like it’s 1999 to keep the local market tight as a drum.

Also from the AEMO:

- Gas demand increased by 3% this quarter compared to Q4 2022, solely driven by higher demand for Queensland LNG exports (+24 petajoules (PJ)). AEMO markets demand decreased (-12 PJ) and there was slightly lower usage for gas-fired generation (-1 PJ).

- Domestic gas supply shifts observed in Q2 and Q3 2023 continued, again mainly driven by declining production from gas fields connected to the Longford Gas Plant in Victoria. Production from Longford fell by 20 PJ compared to Q4 2022, and it has now been overtaken by QCLNG’s Woleebee Creek production facility in Queensland as the largest gas production facility on the east coast in terms of annual production. This supply decrease was offset by the reduction in domestic demand, with Queensland domestic supply also lower (-2.9 PJ).

As more coal closures loom and more renewables are deployed, the shift in the balance of East Coast gas production from VIC to QLD will increase the power of the export cartel and power prices. This is what power futures are screaming about:

As the iMSM reports from a perspective lodged in its own anus, there is nothing to stop it.