The desperation for stimulus at outlets like Bloomberg is foolish, but even they are catching up to reality:

China’s latest batch of data featured continued declines in consumer prices, flat import growth, and a slowdown in the pace of lending — all suggesting sluggish domestic demand will again top the nation’s economic challenges in 2024.

Adding to concerns: economists are pessimistic about whether Beijing’s response to the challenge will prove sufficient. While they see officials responding with monetary easing, the impact may be limited by low confidence levels and a struggling real estate sector. That leaves fiscal policy, but China’s government isn’t scheduled to make its full spending plans clear until March.

For the rest of the world, that raises the odds of lower demand from China for goods and commodities, as well as persistent export price declines — which can help ease inflation, while adding to trade tensions.

Correct. Decades of it. The Chinese economy is not coming back.

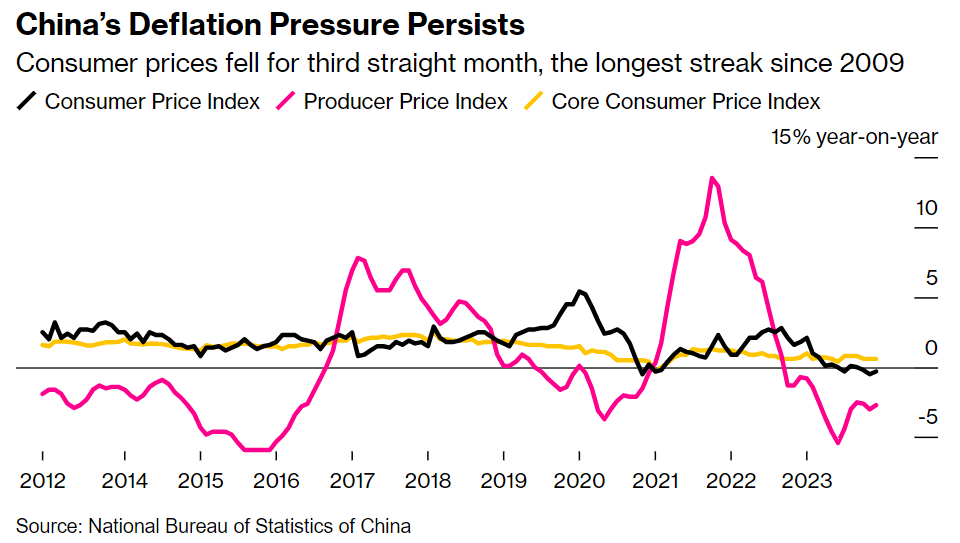

Despite various stimulus announcements, housing supports and fiscal deficits, the Chinese economy is mired in deflation.

December numbers out late Friday were -0.3 for the CPI year on year and only 0.2 annually.

PPI was -2.7% year on year,

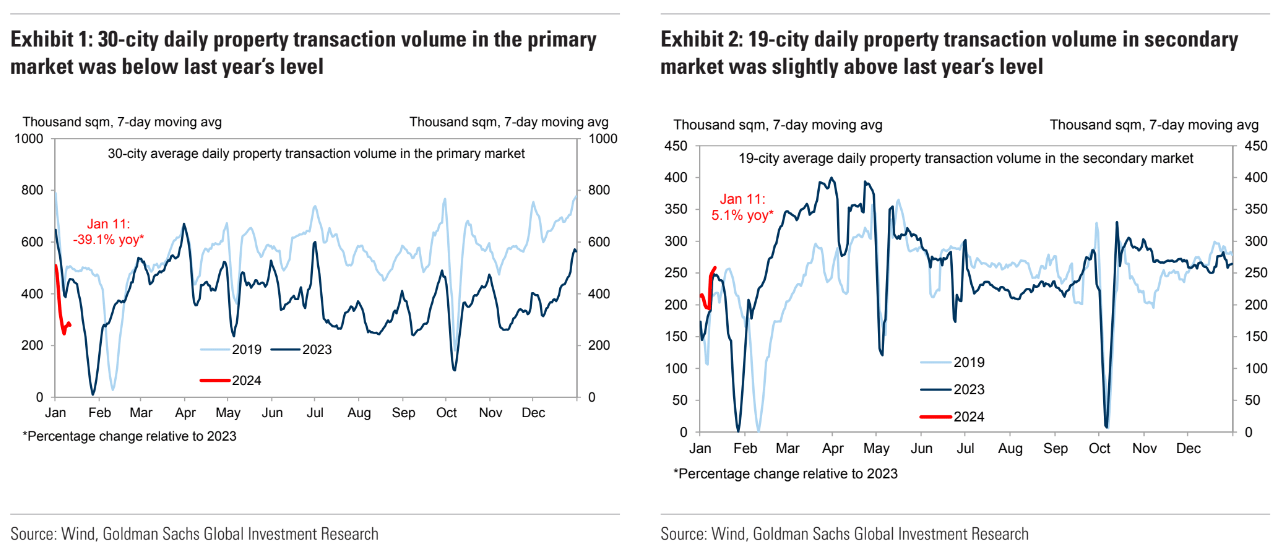

This is not about to stop. The property crash is still in full roar:

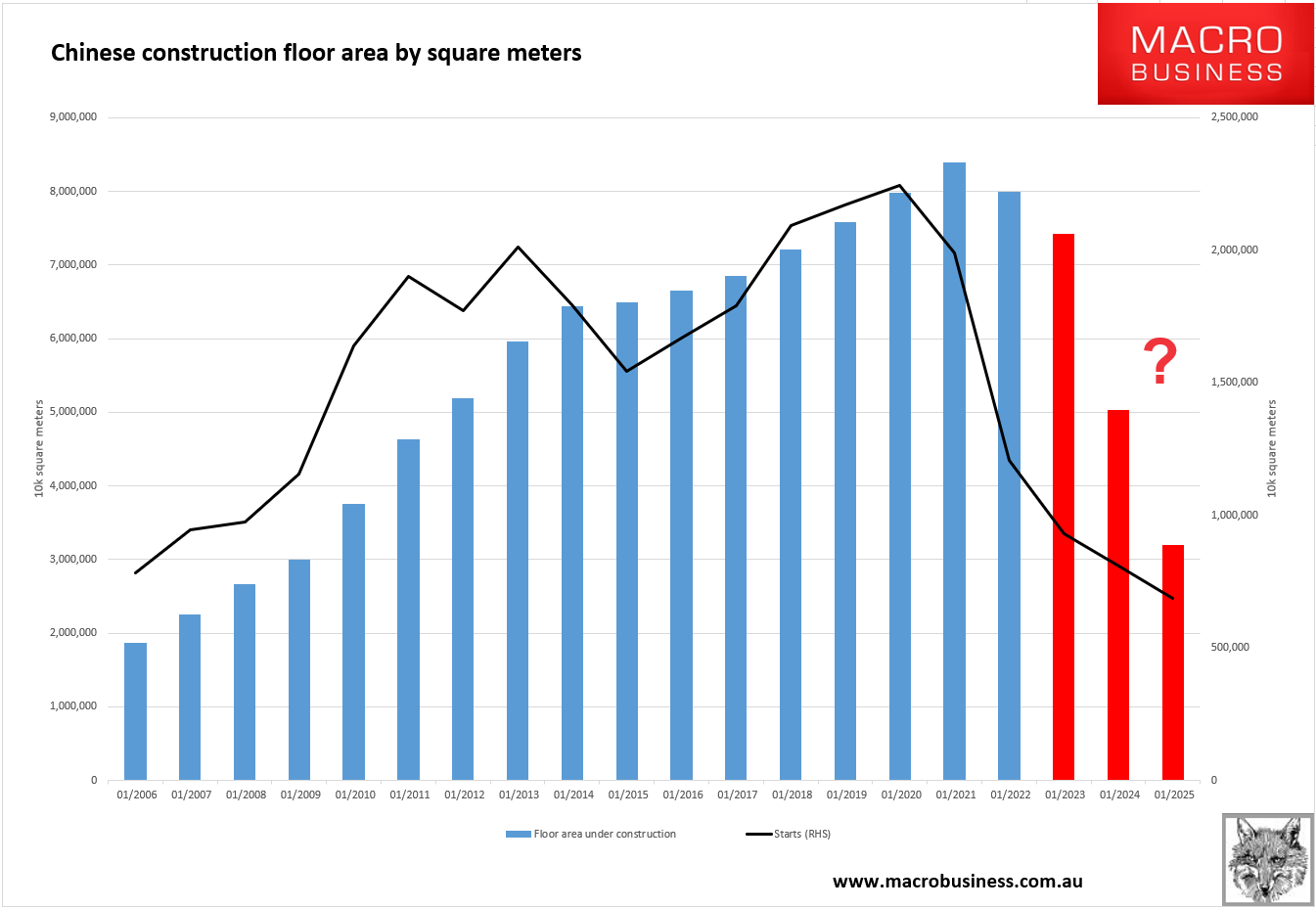

And backward efforts to revive construction via the PSL public housing push will only worsen private sales as expanding glut crowds out demand. More:

China’s property downturn may continue for two more years before gaining stability, according to a former central bank official.

New-home sales nationwide will likely shrink by another 50 million square meters both this year and next year, with 2025’s annual total plateauing at around 850 million square meters, Sheng Songcheng, a former director of the People’s Bank of China’s statistics and analysis department, said at a forum in Shanghai on Saturday.

That sounds about right, with no rebound at the end of it.

But the critical calculation is not sales; it is the stock of construction, which is still far higher at 7.7tr square meters. It must catch down to crashed sales and starts eventually:

The speed of decline will be determined by public support for completions. There must be a risk of sudden and steep demand shocks:

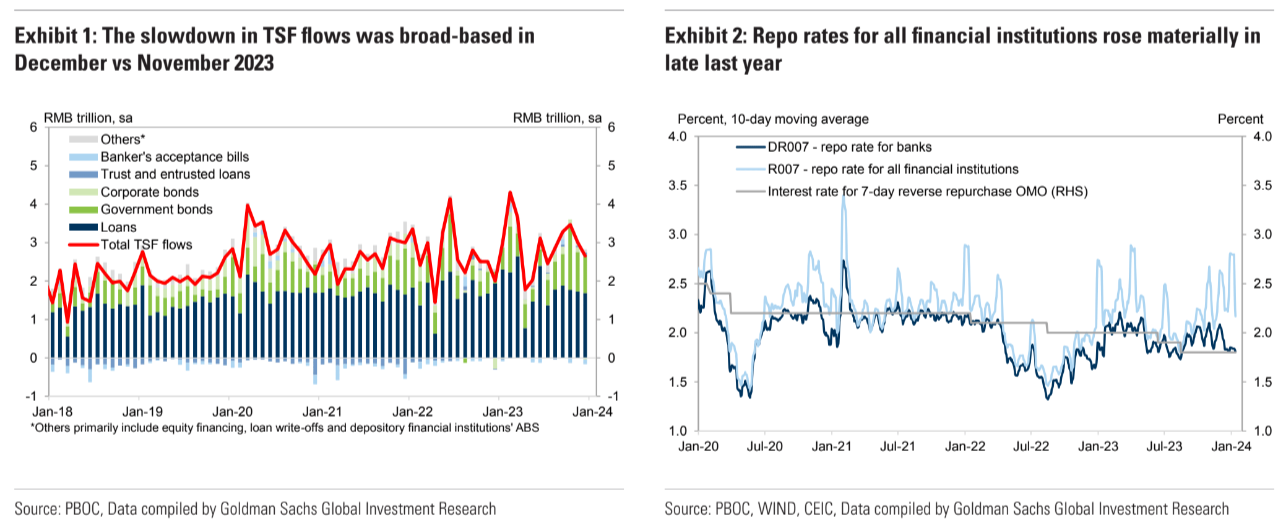

Unsurprisingly, credit demand is still in the toilet. Goldman:

December’s new RMB loans, TSF and M2 data all came in below expectations, showing sluggish credit demand despite the accommodative policy stance.

The composition of loans data painted a slightly less disappointing picture than the headline loan number – based on our seasonal adjustment, both corporate and households’ RMB loan growth improved slightly in December from November last year, but the residual component, which includes loans between financial institutions, likely contracted in the month and dragged on overall RMB loan growth.

In addition, corporate medium to long term loan growth accelerated while bill financing slowed by contrast.

The slowdown of TSF growth was broad-based across different debt instruments – besides lower new loan flows, bond net issuance and shadow banking credit also moderated.

The authority recently warned against funds circulating within the financial system and kept repo rates for financial institutions relatively high in late last year.

This likely contributed to the contraction of loans between financial institutions and shadow banking credit in December.

We saw incremental monetary policy easing signals in recent days, including PBOC’sstatements that they would utilize various monetary policy tools such as “open market operations, medium-term lending facility, relending, rediscount, and RRR adjustments” to “ensure TSF grows rapidly throughout the year”.

Taken into consideration these comments and the deposit rate cuts by commercial banks late last year, we continue to expect the PBOC to cut policy rates (7-day OMO rate and1-year MLF rate) in this quarter, followed by two more RRR cuts and one more policy rate cut in the rest of the year.

It won’t matter. The liquidity trap has snapped shut while the cause of it, the property crash, shows no sign of slowing.

To avoid Japanification, China needs more stimulus than is humanly possible.