Europe, the home of the most damaging gas shortage in the world, now has cheaper gas than Australia:

In Europe, S&P Global Commodity Insights assessed its daily North West Europe LNG Marker (NWM) price benchmark for cargoes delivered in March on an ex-ship (DES) basis at $8.286/mmBtu on Jan. 18, a $0.749/mmBtu discount to the March gas price at the Dutch TTF hub.

Argus assessed the price at $8.30/mmBtu , while Spark Commodities assessed it at $8.126/mmBtu.

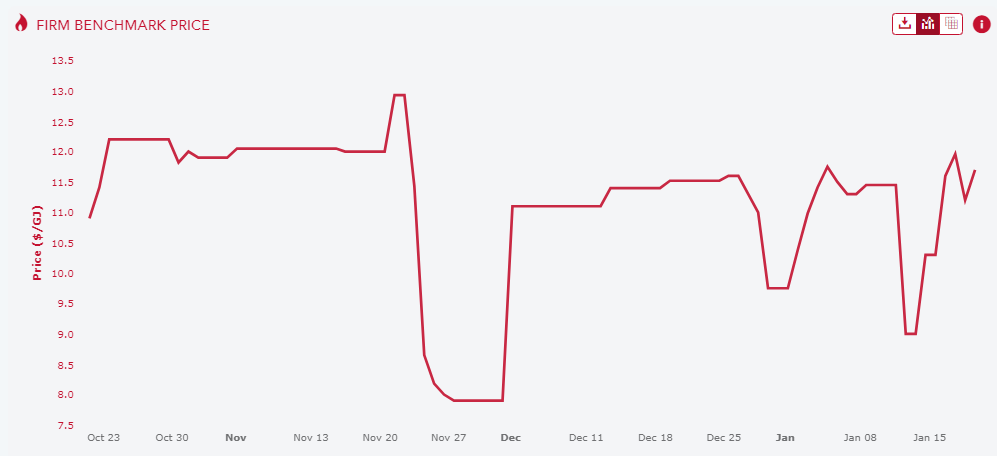

That is a net-back Aussie price of roughly $11.50Gj. And guess what? The local spot price is $11.70Gj:

This is because the home of the most damaging gas shortage in the world is not gasless Europe. It is cheap and abundant gas Australia.

That’s the fruit of a straightforward policy failure.

Post-GFC, when China beholden foreign capital built LNG export plants without a domestic reservation policy, it unleashed an out-of-control gas export cartel that has ravaged the economy for a decade.

Because gas-fired generation sets the marginal cost of wholesale electricity, the shock has often been amplified in power prices.

Like today, as summer electricity demand spikes prices anew:

The spaghetti bowl of gas regulation is manifestly insufficient:

- The ADGM, a retrospective domestic reservation regime, has never been used.

- We have price caps on gas of $12Gj, which have turned into a price floor.

- We have a mandatory code of conduct that is about as useful as Albo himself.

- We have a permanent ACCC monitoring regime that achieves nothing.

The economic consequences are dire:

- The hollowing out of manufacturing.

- Raging inflation for wider households and businesses via utility bills and spillovers.

- The permanent derailment and politicisation of the energy transformation.

It is so maddening because the answers are so simple:

- Cut the price cap in half.

- Apply export levies to gas exporters above $6Gj.

- Activate the ADGSM!

But no, as the global gas glut that has years to run pushes offshore prices below Australian, the local economy will again be gouged tens of billions by a handful of evil carteliers on behalf of China, which takes three-quarters of the gas.

Not even Aussie gas imports will prevent it because the export cartel (which includes Origin Energy) has also dominated those volumes and will ship more local gas offshore to keep the market tight:

Construction of an LNG import terminal in South Australia has begun amid fears Australia’s east coast soon will suffer shortages, forcing users to rely on supplies imported from Western Australia or the Northern Territory.

Venice Energy is looking to establish an LNG import facility in what has been dubbed a “tolling” infrastructure project. Under the scheme, customers book capacity at the plant and source their own LNG, paying a fee to the terminal owner for processing – eliminating the difficult task of aligning gas supply agreements with end-user demand.

Venice Energy in October struck an early stage agreement with Origin Energy for Australia’s largest gas and electricity retailer to potentially underwrite the development and become the terminal’s sole user for at least 10 years.

Now, let’s get back to your regular programming and the culture war de jour.