Honestly, Bloomberg is useless on this.

China is ramping up pressure on banks to support struggling real estate developers, signaling President Xi Jinping’s tolerance for property sector pain is nearing its limit.

Developer stocks and bonds rallied in China this week on bets that authorities may introduce some of the most sweeping measures yet, creating a draft list of firms eligible for bank support while weighing a plan that would allow banks to offer them unsecured loans for the first time.

The moves are aimed at easing the real estate industry’s cash crunch, people familiar with the matter said, underscoring the anxiety among China’s top leadership over the protracted crisis. Beijing also wants to ensure developers have enough cash to finish the millions of homes under construction, even if it means added risks for its banks.

“The new round of measures to support the property sector would be powerful to break the vicious cycle of widespread defaults and avoid the spread of systemic risks,” said May Zhao, head of equity research at Zhongtai Financial International Ltd.

Balls. Xi property shenanigans have been a disaster since his ascension and this is no different.

Chinese property was already way overvalued and overbuilt when he rose to power in 2011. Xi knew this so he began a program of reform known as “rebalancing” from investment (that is, building empty apartments) to consumption (making households richer).

But he only got a few months into it when he got spooked by falling property prices and weak GDP growth so juiced another round of speculation.

He tried again to stop property in 2015 and lasted a little longer before the economy crashed and he again juiced another round of speculation.

This time, however, a combination of growing moral hazard and stupid policy triggered the greatest property construction bubble in the history of the world. Ponzi-developers went mad. Selling enormous volumes of property but never building it and siphoning off the deposit capital (which is 100% of the purchase price in China) into crazy rich Asian bullshit.

Then along came Xi in 2020, who decided to tackle it again. Seemingly unaware that he was now confronting a tens of trillions of dollars problem in ponzi-developers, unfathomable overbuild, immeasurable unfinished builds, and a credit mess so large that it had spawned such global monetary monstrosities as Tether and crypto.

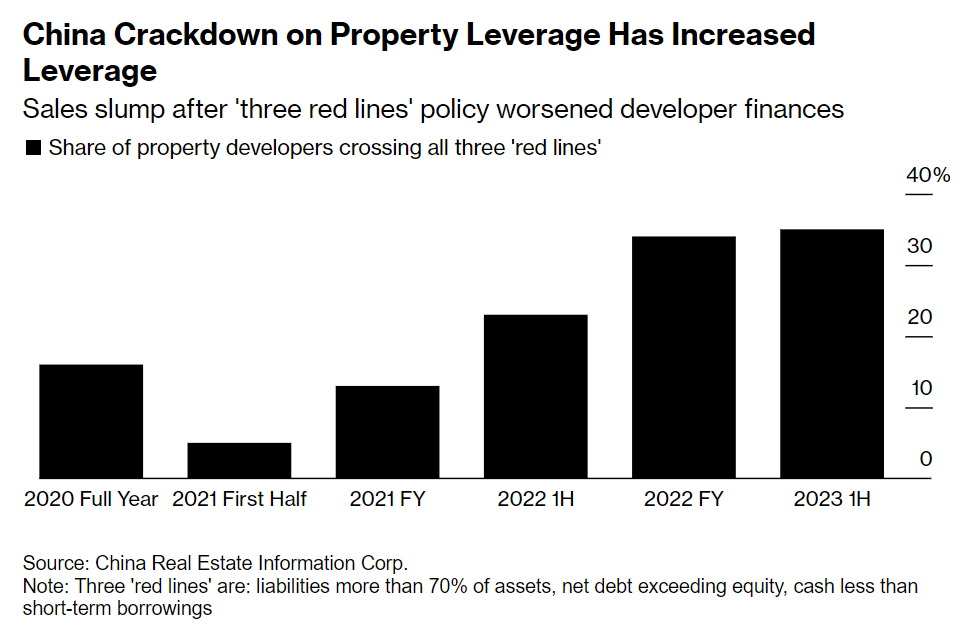

When policymakers applied leverage ratios to developers in late 2020 – the three red lines – they pulled the wrong stick and, kerplunk, the whole pyramid began to collapse on itself.

As a result, leverage is now far worse for developers as falling prices, falling sales, falling funding, and rising unfinished construction turn them into credit black holes:

This situation is no longer about “Xi’s tolerance”. It is about the total collapse of the largest credit and construction bubble in the cosmos. It can be slowed, but it cannot be reversed.

Look at the proposed solutions:

- Offer privileged developers unsecured expensive short-term to pay off long-term debt. I mean, is this a serious suggestion?

- Force resistant (that is, sane) banks to lend without collateral to bowel-shakingly insolvent ponzi-developers in the hope that completing a few extra projects will revive sales.

- Build, like, heaps more government-funded apartments to replace shantytowns. Increasing supply into the world’s largest glut to revive sales, even as prices fall even more.

- All of this as the real problem – collapsing demographics and exhausted urbanisation – gets worse every year, reducing the numbers of buyers and household formation.

- And a truly stupid dictator flops around like a headless chook, changing his mind about property every few minutes.

The problem is still being treated like it is some kind of cyclical sentiment downturn. It is not. It is a structural brick wall. The end of the Chinese catch-up growth period as the one-off modernisation build-out of property and infrastructure is complete.

Bizarrely, this simple truth is why Xi tried to stop property in 2011. Now, he seems unable to grasp it at all.

The truth is this: for anybody still breathing, there is no investment case for Chinese property. It is the most significant single “sell” on earth and will remain that way for decades as the population halves.

Which means China’s growth period is over. It will grow at 5% only with full fiscal support and a GDP deflator of -1.5.

If nominal growth is stuck at 3.5% and we calculate the writeoffs for its unimaginable capital misallocation the way developed economies do, then on the ground, Chinese growth is more like 1.5% hereon in.

China is done.