History doesn’t repeat but it does rhyme and, very occasionally, it inverts.

Today’s advancing global recession is the mirror image of the Global Financial Crisis of 2008.

Let’s recall that COVID was not a natural end to the last business cycle, so today’s inverted GFC is a successive business cycle ending shock.

What am I talking about? The death of Chimerica.

Advertisement

In the days before the GFC, the Chimerican beast was born. This illusory animal was the rise of a Chinese export giant feeding on the consumption giant of the US.

It was illusory because the capital flows of Chinese savings into US debt that made it work were also an enormous macroeconomic imbalance.

Sooner or later, the American property bubble Chimerica relied upon would burst, and so it did in the GFC.

In the subsequent years, the US crashed its interest rate structure and printed squillions to enable deleveraging. Lots of that free money flowed out and mobilised investment in other nations.

Advertisement

In particular, it helped inflate the post-GFC Chinese property bubble. A building boom so vast that it produced an astonishing 14k apartment blocks per year.

Sadly for Chimerica, this was also an illusion. The construction mania came at the end of the Chinese development path, just as its demographic and urbanisation pulse peaked.

As in the case of the prior US boom, the bubble enormously overshot underlying demand and sooner or later, it was also going to burst.

Advertisement

Today it has. We have seen household-name Chinese developers default and go under for two years. It’s goodbye to another today:

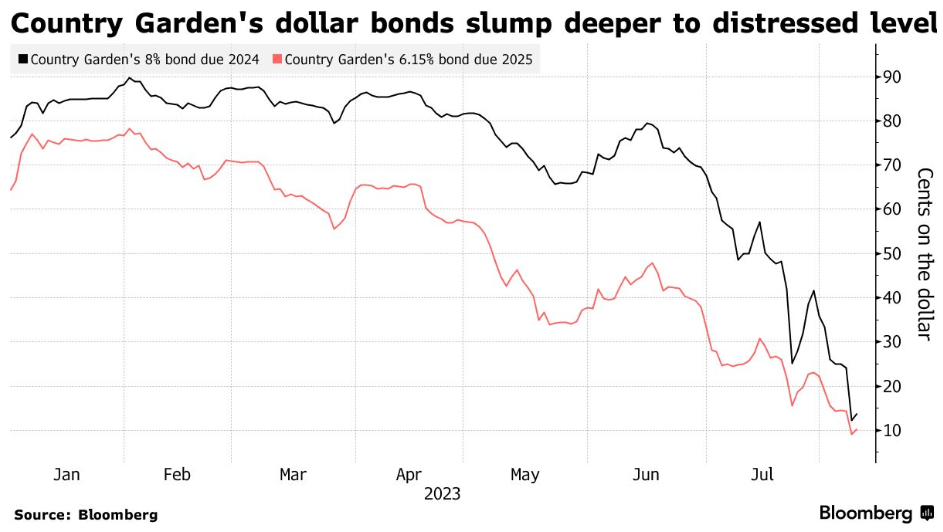

Country Garden Holdings Co., helmed by one of China’s richest women, Yang Huiyan, has left investors in the dark after dollar bondholders said they’ve yet to receive coupon payments effectively due Monday. That puts the firm—which had 1.4 trillion yuan ($199 billion) of total liabilities at the end of last year—on course for its first public default if it doesn’t make the payments within a 30-day grace period.

Formerly the nation’s largest private-sector developer by sales, the builder of more than 3,000 housing projects in smaller cities is a household name and employed about 70,000 people at the end of last year. That status had given it the firepower to withstand an industry cash crunch that led to record defaults since Evergrande first missed bond payments in 2021. But tumbling industry home sales and soaring refinancing costs are threatening that streak.

Projects in small cities are the primary toxic assets, not a source of strength!

Advertisement

So, will we see another global debt shock on the scale of 2008? Probably not. In the inverted GFC, the shock will be rendered invisible at the point of a rifle:

Taking the pulse of China’s $18 trillion economy is getting tougher for foreign visitors who previously could count on holding informative meetings with key policy makers.

While “old friends” such as Bill Gates and Henry Kissinger have gained access to the highest rungs of power in widely publicized visits this year, it’s been a different story for bankers, economists and businesspeople returning after three years of closed borders.

Accounts from more than a dozen people, some who asked not to be identified to speak freely, describe dinner invitations that were seen as potential ethics breaches and politely declined, silence around taboo topics such as deflation and bland party speak replacing the honest exchange of ideas. Once-familiar officials, they said, are now fearful of breaching newly broadened anti-espionage laws as President Xi Jinping grows more wary of the US and its allies.

So far, the imploding debt within the Chinese bubble has been rationalised via defaulting dollar bonds of Chinese developers. This has been nasty for some hedge funds and has helped drag down global equities.

Advertisement

The developers also have huge liabilities with regional Chinese banks, which will soon appear as a balance sheet shock within China. This will be hidden via policy bank extend and pretend, plus takeovers and a new round of bad banks.

But that is only the beginning. Again like the US experience, China’s post-GFC bubble took in municipal governments. Indeed, in China, it is much worse.

$9tr of debt has been issued by local governments in China for dubious infrastructure purposes. These debts must also be rationalised because urbanisation is falling away before households are rich enough to make the projects economic.

Advertisement

These must be addressed via debt swaps with Beijing in another great exercise of extend and pretend. Expect huge federal deficits as China churns its savings, ala Japan.

The inverted GFC probably won’t happen like the GFC did. It probably won’t flow outwards as a sudden insolvency shock that takes down global money centre banks resulting in the lowest interest rates in 500 years and QE everywhere. China owns its own banks.

But, equally, in an inversion of the GFC, China cannot deflate itself externally as the US did. It is trapped by excess savings that want to escape, a banking system that cannot afford to lose them, and a currency that cannot fall lest it trigger a crisis.

Advertisement

Instead, China’s inverted GFC will deflate internally via falling asset prices supported by public debt, perpetually weak consumption supported sporadically by public debt, endless and fruitless bursts of wasteful construction and, most importantly, big falls in GDP growth.

These, too, will be hidden. Just as they were in Q2 when deflation boosted headline GDP while the nominal economy shrank. The recent falls in labor demand and rise in youth unemployment are structural.

Like an invisible man going swimming, the inverted GFC will be visible in the ripples it creates in the global economic pool.

Advertisement

The waves will be most apparent in shocking falls in commodity demand, deflation in goods, reduced Chinese capital and falls in assets reliant upon Chinese demand, as well as a permanent shunt lower in the pace of global GDP growth.

And, if the inverted GFC so disables the Chinese economy that its people grow restive, its last wave will be war.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.