Goldman wraps issues with CNY.

1.Recent developments of the RMB?

Sluggish activity growth and widening unfavorable interest rate spreads have weighed on the CNY exchange rate, and the PBOC has been more aggressively defending the currency in recent weeks.

2. Risk of large capital outflows?

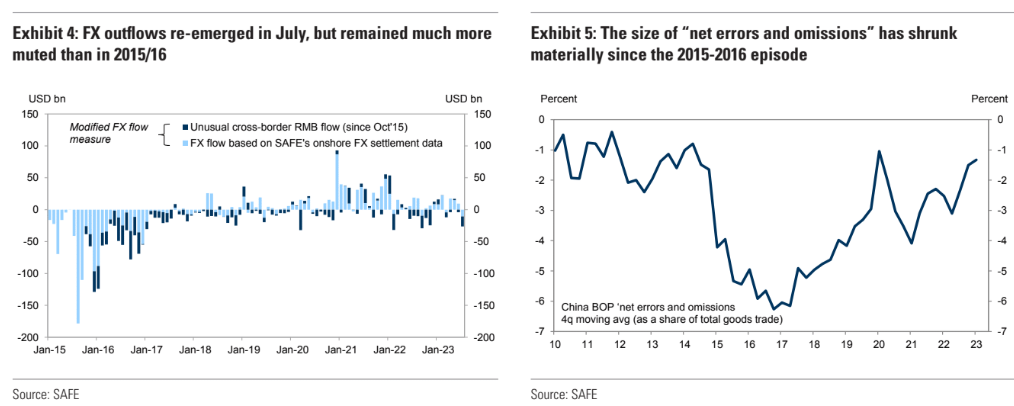

While we expect outflows to continue in the rest of the year, due to uncertainty in the growth outlook and negative interest rate spreads, we continue to expect overall capital outflow pressures to be well-managed and do not expect a repeat of the large-scale outflows and reserve losses seen in the 2015-2016 episode.

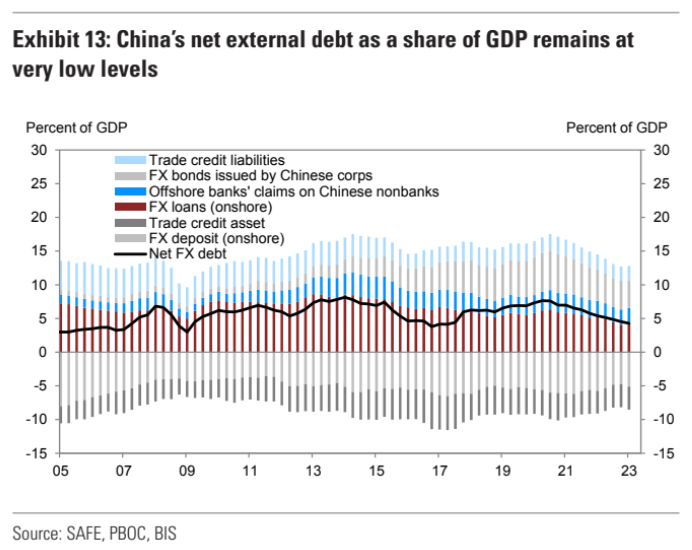

3. Implication for official reserves?

China’s commercial banks accumulated FX from 2H 2020 to 2021, which can serve as a buffer for capital outflows. The impact of capital outflows on official FX reserves could be smaller this time around.

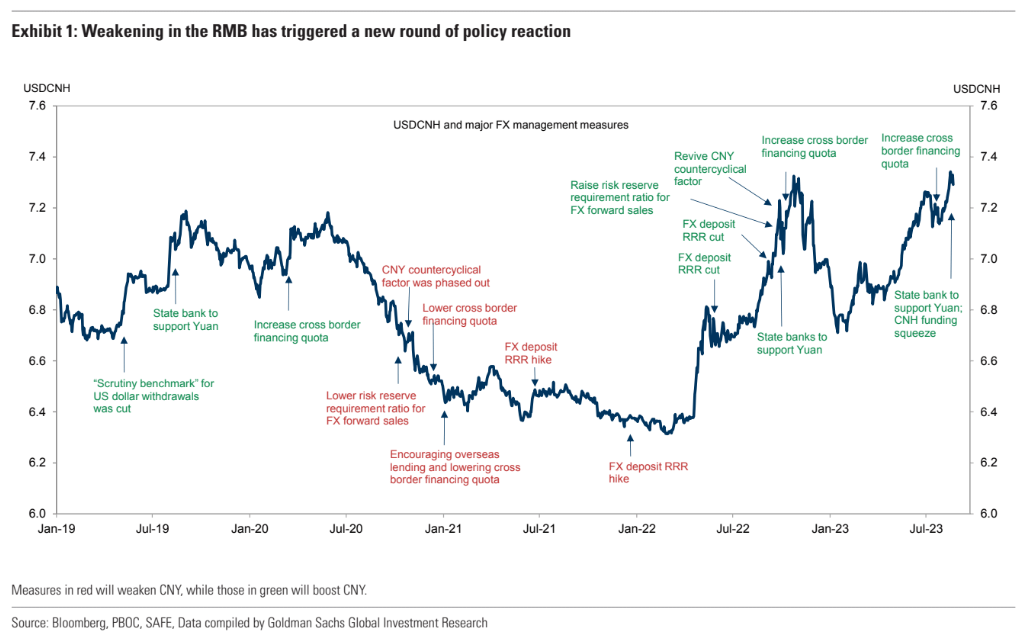

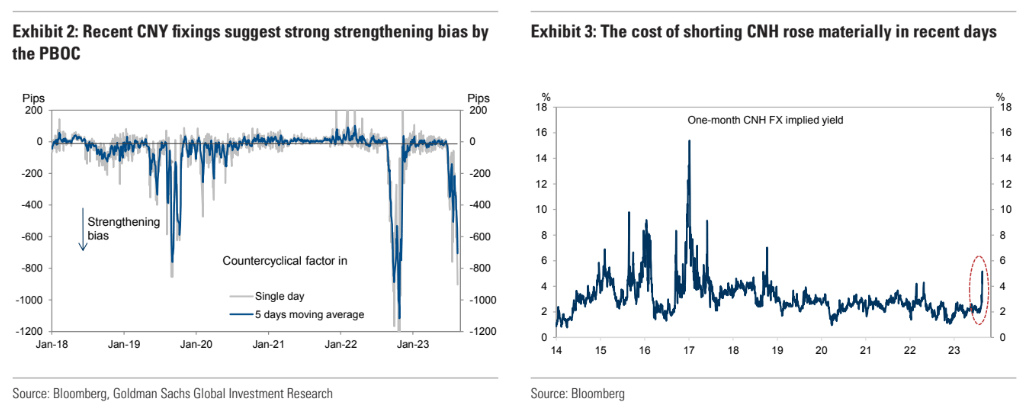

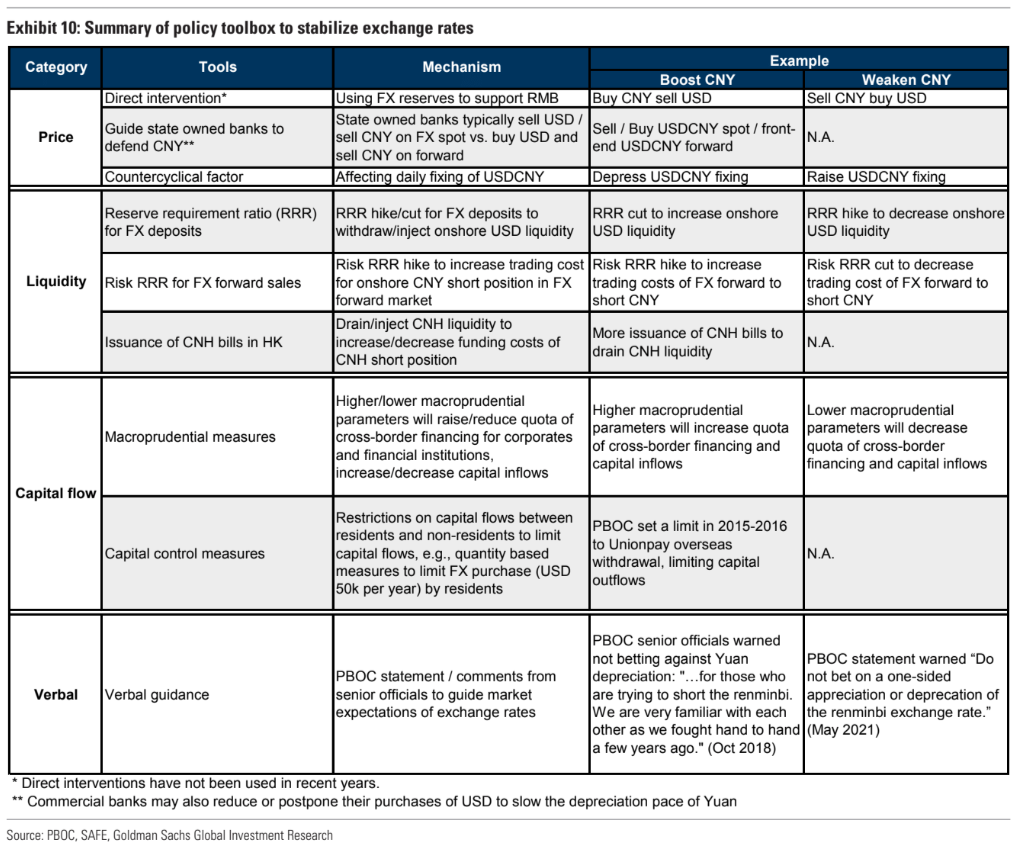

4. New pattern of PBOC’s FX management?

The authorities typically signal discomfort over a sharp depreciation via strong CNY fixing (i.e., a negative CCF) initially, later adding other macro-prudential measures focusing on capital flows, followed by liquidity management if the pressure continues.

5. Growth, inflation implications and the side effects of a weaker currency?

Further depreciation of the currency on a trade-weighted basis, as long as the pace is well-managed, may be welcomed by policymakers amid recent deflationary risks and sluggish activity growth. The side effects from well-managed depreciation appear limited, due to the small size of China’s external debt.

6. Forecast for future exchange rate path and related policy reaction?

The RMB will continue to face depreciation pressures in the near term, in our view, and we expect policymakers to continue supporting the currency when necessary, but mainly aim to avoid “excessive moves” rather than defending a specific level of exchange rate.

My answers to the six questions are below.

- Growth will get much worse and not rebound. CNY is untested in the environment of a structural shunt lower in growth. The interest rate spread will plunge to levels never before seen.

- Capital outflows will intensify as creditworthiness is repeatedly tested in property, LGFVs and provincial banks. The capital account had to shut in 2016 to prevent a run, and still is. Expect more tightening.

- Reparition of FX reserves can work for a while but not if it is structural.

- The PBoC can only slow the tide, not stop it.

- External debt is not the issue with a falling CNY. Rather it is feedback loops with other currencies that matter. As CNY falls, so does EUR, and DXY will rise, choking off financing for EMs just as they have to compete more with China. The last few weeks are an example of how this dynamic crashes markets. It will feed back to China via falling global growth.

- I expect CNY to fall a long way from here. China has structured its economy as a combined export powerhouse and property Ponzi scheme. Without the latter, the former must grow, yet it can’t owing to geopolitical blowback. Meaning an even lower currency.

- China’s excess savings must also go somewhere, and if is not going into increased consumption, then it must be offshore. A falling CNY only makes this pattern worse.

The totality of this makes me wonder why anybody thinks CNY will substitute DXY as a reserve currency. Forget it.

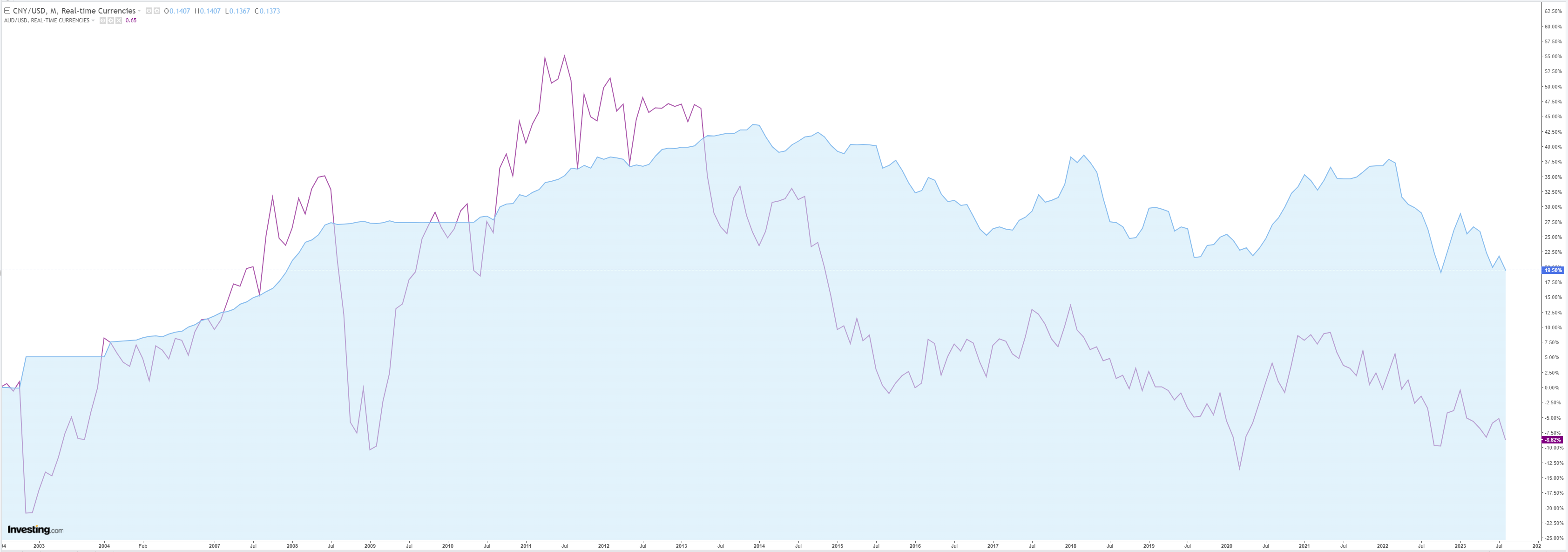

So, how far does it fall? I would have thought back to WTO accession levels in 2003 when Shanghai began the great build-out:

Which would give us an AUD around 0.48 cents. Lower if there’s a crisis.

How long? If Xi gets it wrong and either provincial bank NPLs or LGFV defaults trigger counterpart risk shocks, it will be within a year.

If Xi goes for extend and pretend then five years.