Goldman with an excellent report that nicely summarises where China is headed now.

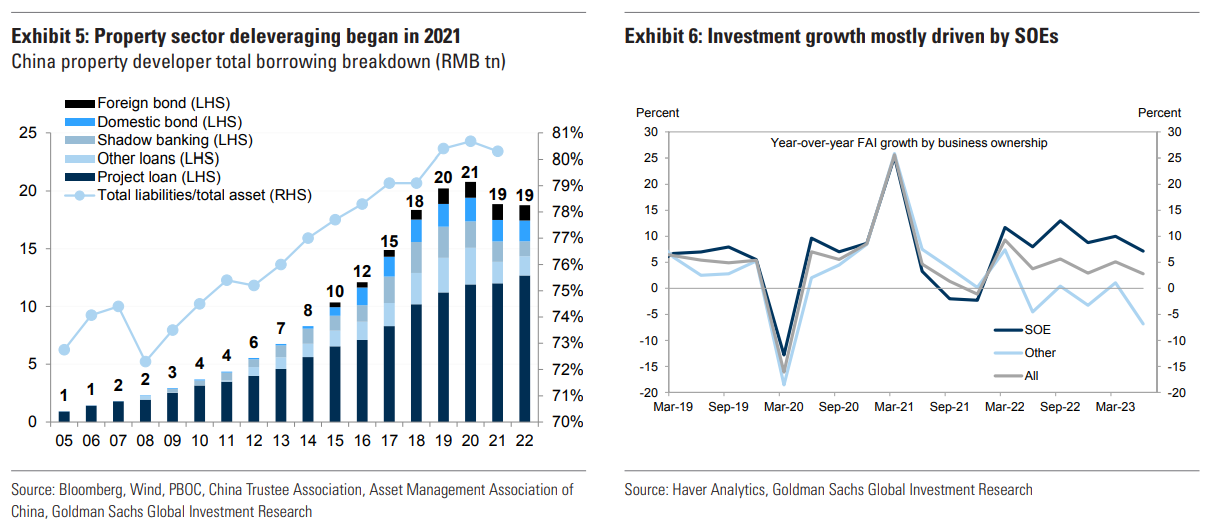

Still reining in the “Gray Rhinos”. In our China Debt Map published in 2021, we expected credit clean up to be a key policy objective, with policymakers looking to rein in “gray rhino” risks in the financial system – obvious risks that may lead to large credit problems. Specifically, we noted three areas that policymakers will focus on: (1) controlling leverage within the property sector, (2) resolving implicit debt within local governments, and (3) continued risk reduction in shadow banking. Following the COVID releveraging over the past few years, we believe reining in the “Gray Rhinos” remains important for policymakers going forward. With shadow banking lending substantially

lower now compared with 5 years ago, we believe the focus will be on managing the deleveraging process in the property sector, and to step up LGFV debt cleanup.

Adjusting to an L-shaped path for the property sector. The latest downturn in the China property sector originated in late 2020 with the introduction of the “Three Red Lines”, measures aimed at restricting the amount of financing available to property developers based on satisfying three leverage metrics. But unlike previous downturns, policymakers have not introduced significant policy easing to reflate the sector and reverse the slump. To us, it is clear that this time is different. We believe policymakers are unlikely to revert to large stimulus, as they seek to diversify away from credit-driven real estate development as a major engine of growth, and given that the demographics fundamentally point to the need for a smaller developer/property sector. Furthermore, there have been meaningful shifts in sentiment from homebuyers, as expectations of pricing appreciation have been eroded and heightened defaults have led to reduced appetite to purchase pre-sold, unbuilt properties. Our China economics team are assuming an “L-shaped” path for the property sector in coming years, estimating that the property weakness will likely be a multi-year growth drag for China, with continued (but diminishing) negative impact to headline GDP growth in the coming years.