Let’s begin with Michael Hartnett at BofA.

Zeitgeist: “Every billionaire minting same long T-bills, long Nasdaq barbell…biggest Q3 pain trade is lower yields, lower Nasdaq, plus higher Yen…no one has that on.”

The Price is Right: Cosmo AM&T (005070 KS), Wistron (3231 TT), EcoPro (086520 KS) only stocks on planet that have outperformed Nvidia’s 188% YTD gain.

Tale of the Tape: UK issues 2-year gilt yielding 5.7%…invest $1bn in asset with 5.7% yield, you’ll make $57mn next 12 months & double your money by 2036.

Tale of the Tape II: bonds are big, fat & trendy…big levels breaking in 2-year yields & 5-year real rates (now highest since 2008); more interesting is yield curve steepening despite off-the-clock US jobs data; steeper yield curve would be big Q3 recession tell.

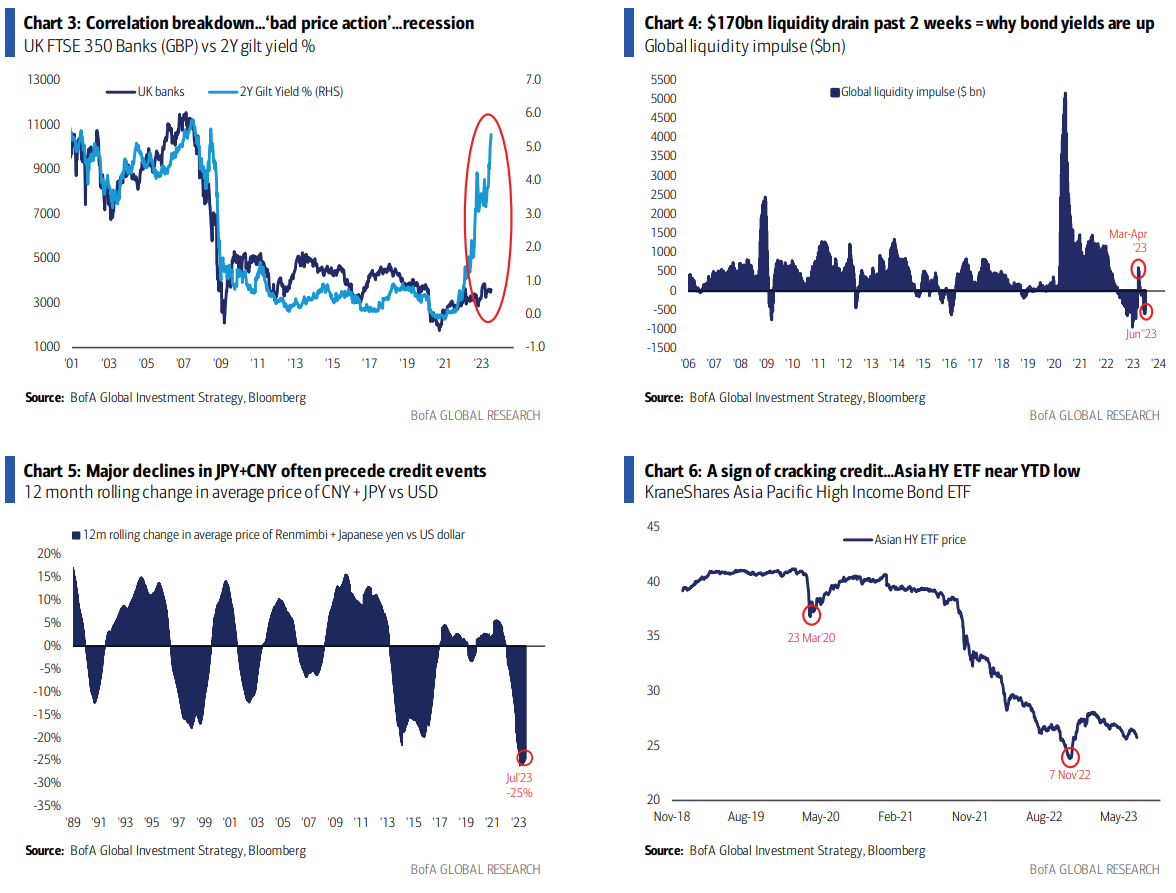

The Biggest Picture: FX so often the origin of deleveraging…v few see new rates shock as sinister but should big FX carry-trades (none bigger than long Mex peso-short Japan yen – Chart 2) start reversing bigly & US dollar pops, we see some proper risk-off.

Weekly Flows: $29.0bn to cash, $13.0bn to equities, $9.8bn to bonds vs $0.6bn from gold funds.

Flows to Know:

x Cash: 1st inflow to money market funds in 4 weeks…total cash AUM now monster $7.8tn;

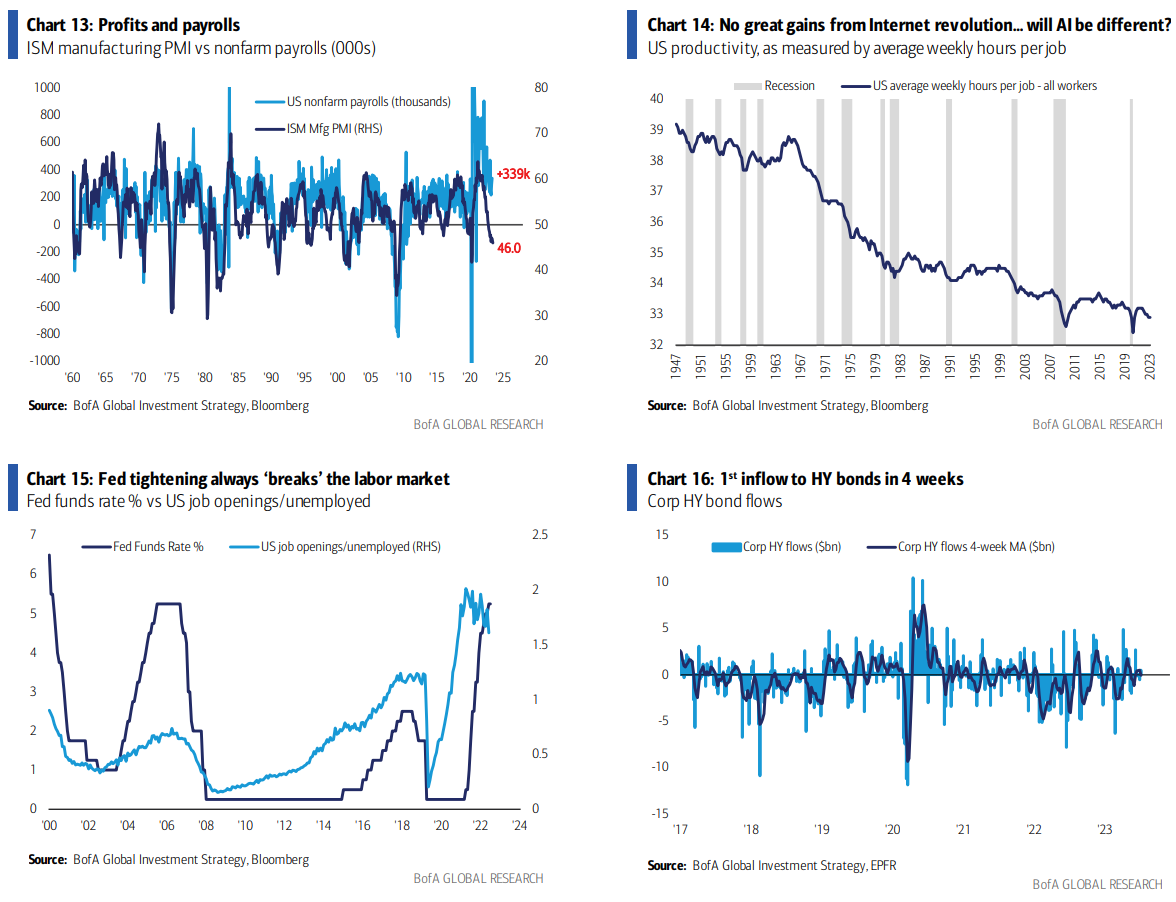

x Credit: largest inflow to IG bonds in 5 months ($9.0bn), plus 1st inflow to HY bonds in 4 weeks ($0.5bn – Chart 16), to-date no fears re corporate bonds;

x Stocks: 1st time since Nov’22 inflows to Developed Markets ($31bn past 8 weeks) trending higher than into Emerging Markets ($14bn – Chart 17)

x US & Japan: inflows to Japanese stocks past 5 weeks ($8.9bn); largest inflow to US large cap funds in almost 8 months ($12.9bn – Chart 18).

BofA Private Clients: $3.2tn AUM…60.4% stocks, 21.1% bonds, 11.7% cash; private clients happy in high-yielding fixed income & cash, and a subtle seller of stocks into strength…biggest stock outflows in 6 weeks & note GWIM total equity AUM up 11% YTD vs 14% gain in SPX; ETFs past 4 weeks show clients buying Japan, HY bonds, selling TIPS, utilities.

BofA Bull & Bear Indicator: no change at 3.2…Bull & Bear Indicator stays more bearish than bullish due to still-high cash levels (5.1% in June Global FMS), weak flows to risky HY & EM debt funds, which offset bullish shift from hedge funds, better stock market breadth and credit technicals.

Hotter than July: 7th US payrolls, 11th CPI, 11-12th NATO summit, 14th JPM EPS, 19th Tesla, 25th ECB, 26th FOMC, 27th BoJ, 26-28th likely Apple/Microsoft/Google, late-July also China Politburo…no wonder vols off the floor.

Rates Shocking Again: into central bank meetings, driven by inflation, deficits (wars are very expensive), and strong labor market data, financial conditions tightening again in early-Q3, keeps the “higher-for-longer/hard landing” view entrenched (that’s ours – we say Q3 tightening of financial conditions great opp to position for hard landing)…

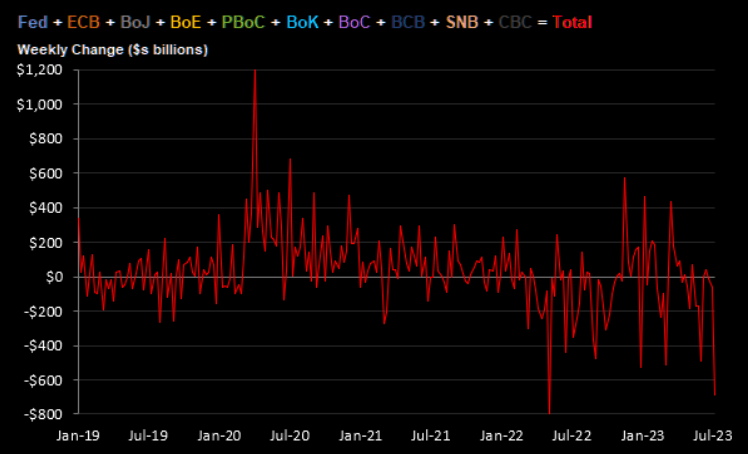

x liquidity, e.g. central banks have drained $170bn liquidity past 2 weeks (even with BoJ YCC – Chart 4), another $1tn drain expected next few months;

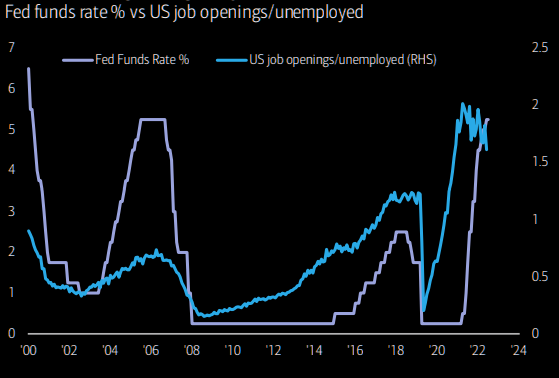

x Fed: 200bps cuts were expected ‘23/’24 after SVB…now just 100bps cuts priced in;

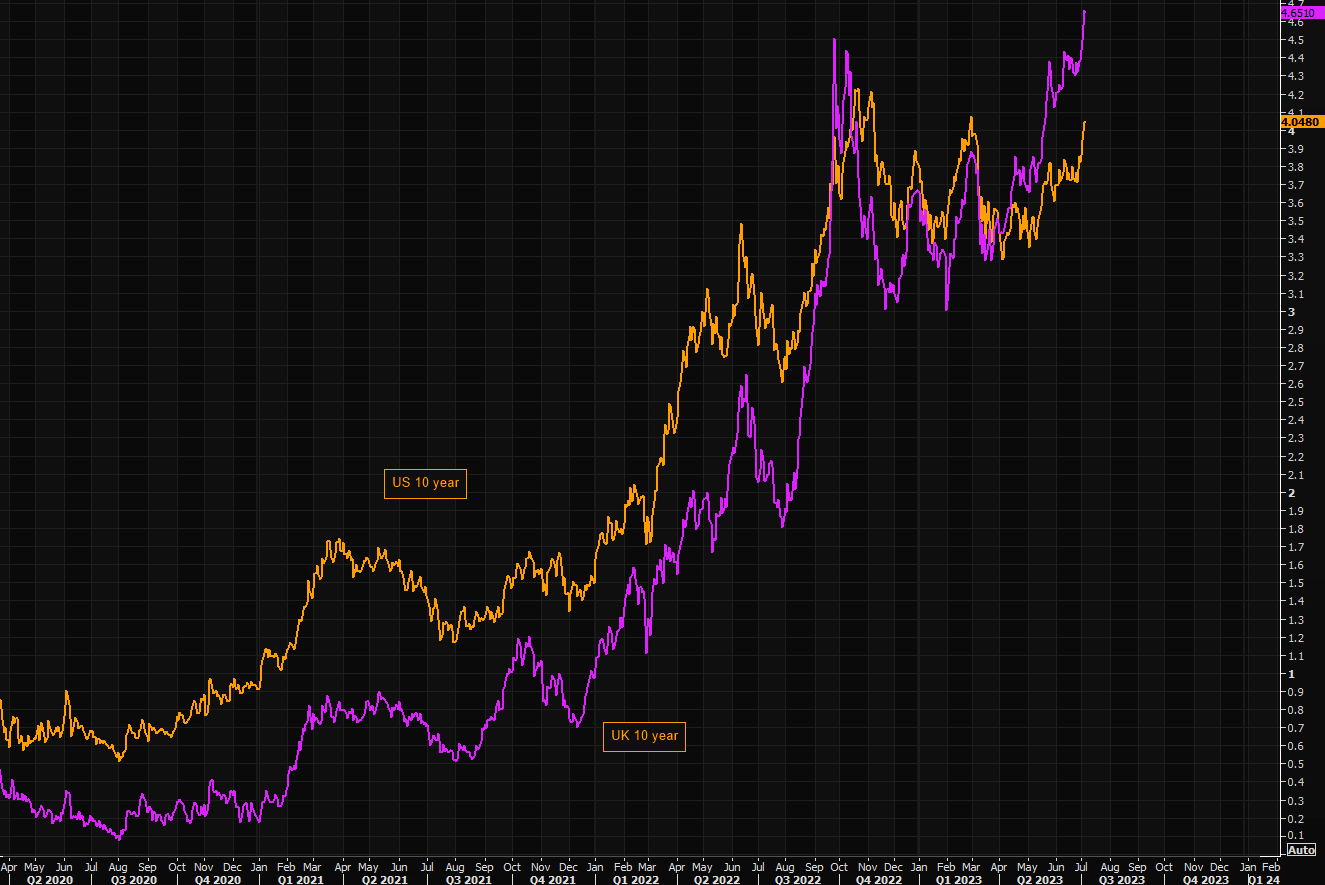

x yields, e.g. 2-year yields highest in UK & France since 2007;

x real rates, e.g. highest 5-year US real rates since 2008;

x banks, e.g. higher yields, lower banks (see UK – Chart 3) never good;

x yield curve, e.g. “double-low” in 2s10s inversion around 110bps – steeper is recession signal;

x HY, e.g. Asia HY credit ETF price near YTD low and down 8% since Jan’23 high (Chart 6);

x FX, e.g. big FX reversals (rolling 12-month change of average value of Japan yen & China renminbi down 25% in past year – Chart 5) often coincide with deleveraging.

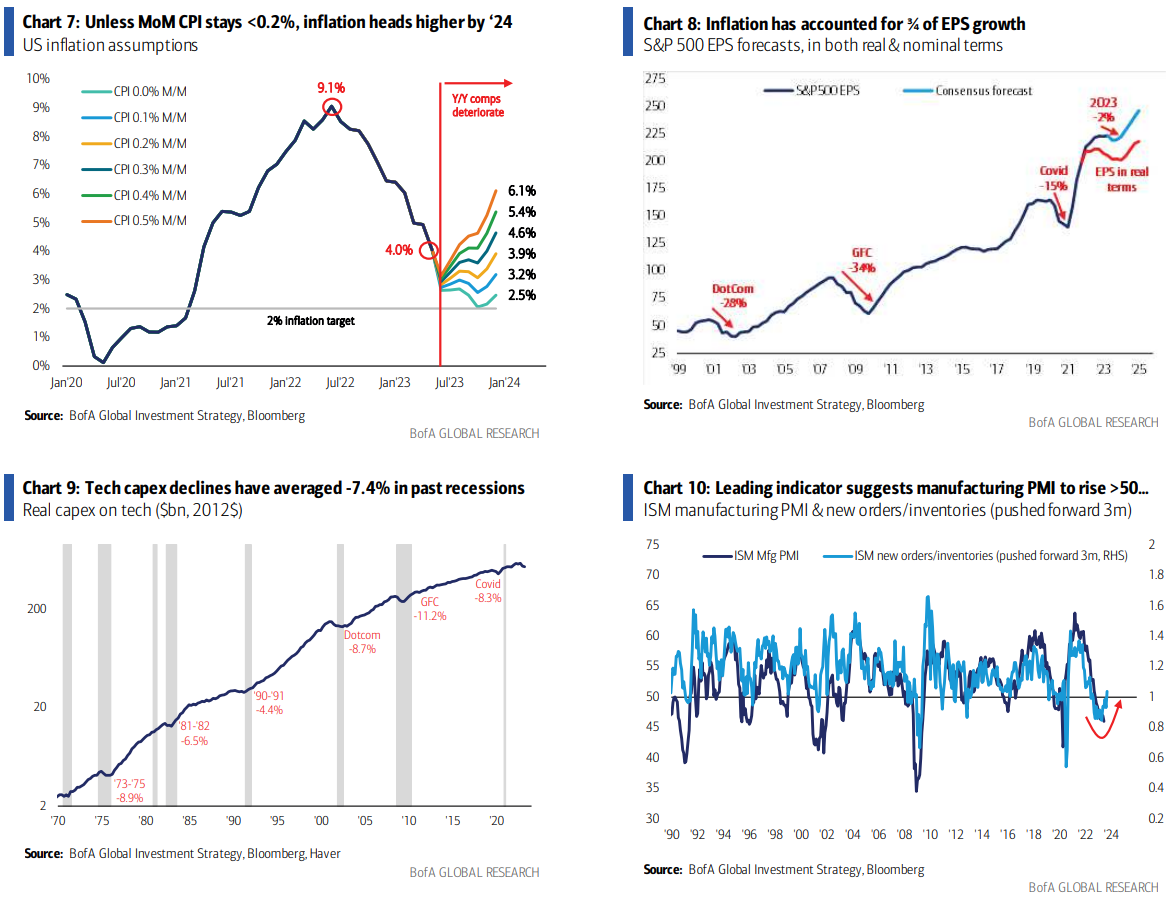

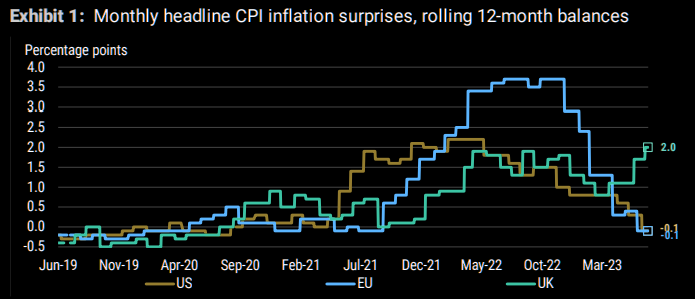

Trough Inflation: bull factor for markets has been drop in headline inflation from 9% to (next week) 3%…but on current monthly CPI trends the June print will be trough for 2023 and H2 sees rise back to 4% (unless monthly prints gap lower to <0.2% v soon – Chart 7); important side note…inflation has been positive for EPS – why the Q1 EPS recession call was so off…past 18 months US core CPI up 9%, S&P 500 EPS up 12.5% thus real EPS growth +3-4% since Jan’22 (Chart 8).

Trough Profits: profits v correlated with ISM (Chart 13) and ISM led by ratio of new orders to inventories…latter strongly suggests manufacturing ISM to rise >50 next 3-4 months (Chart 10); this is good news although transportation, semis, industrials, homebuilders have discounted the outcome and thus v vulnerable if headfake (was case in 2001/02 & in 2023 more important service sector trends are far less impressive – Chart 11)…and China/Europe economic data pretty atrocious right now (Chart 12).

AI vs Rates: AI remains a narrative based on speculative numbers; but the numbers are big (ChatGPT web traffic down 10% in June, 1st ever drop, but still 1.8bn to 1.6bn visits ain’t bad); internet in late ‘90s spawned “new paradigm” productivity thesis that was not borne out in data (Chart 14) & IT real spend is anything but recession-proof (IT spend has fallen on average 7-8% in recessions since 1970 – Chart 9) – we say “sell the last hike” will hit tech hardest…but if AI & Magnificent 7 can shrug off new rates-shock then “baby bubble” set to mature into something bigger in H2.

The Market Ear picks up the AI bubble theme.

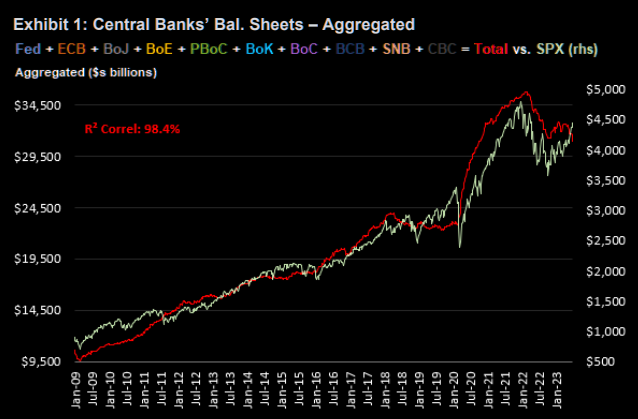

The one chart to rule them all

Liquidity matters, and given that the GLJ liquidity measure has a 98.4% R² correlation to the S&P 500 dating back to January 2009, you should pay close attention. Rougher times ahead?

GLJ

CB delta

Not looking overly supportive…

GLJ

The cross

US 10 year saw the 50 day cross the 100 day moving average as yields surged this week. Previous crosses have led to yields moving much higher. Maybe this time is different, but MS reminds us: “…yields eclipsed 4% this past week for the second time this year and the third time since 2008”.

Refinitiv

Bondmania

There are big differences between the drivers of US and UK rates, but the motion in UK rates really makes you wonder…

Refinitiv

Battered bonds

MS sees a comeback for bonds going forward: “The possibility that central bank hikes to date may weigh on economic activity into year-end, and that any remaining hikes may not come until mid-2024, increases the attractiveness of government bonds, in our view. Hence, while they’ve been battered and bruised, government bonds look primed for a comeback in 2023.”

MS

Will they break it again?

Fed always breaks something…

BofA

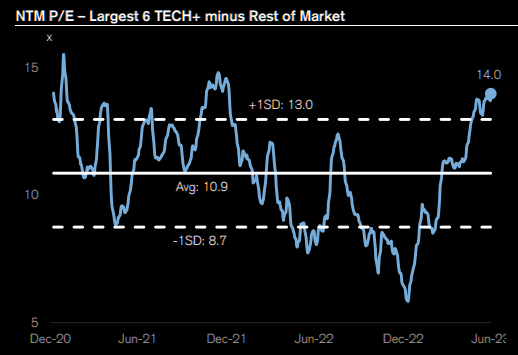

Big tech not cheap

The easy AI trade is over. Things up here are much more tricky.

CS

NASDAQ – now vs 1999

It would be almost too perfect, but why not a painful pullback here, and then a crazy autumn bull…

Refinitiv

Short sales

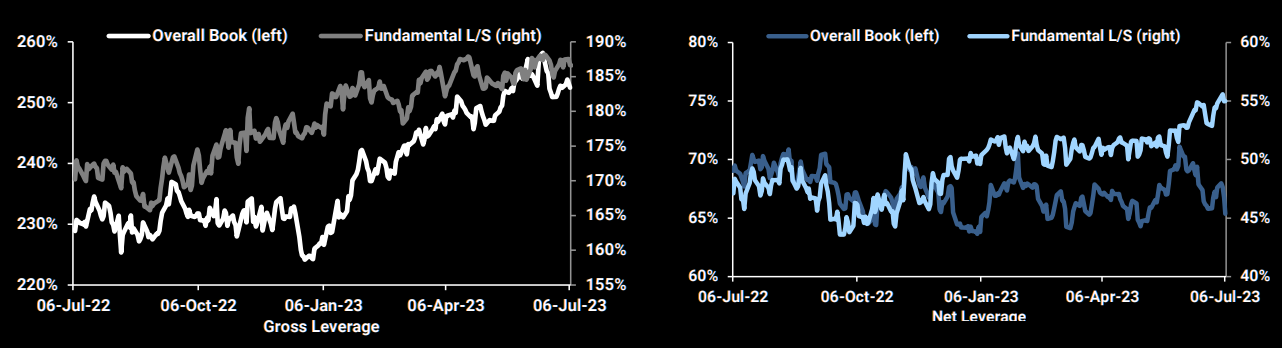

Latest flows via Goldman’s prime book: “Overall Prime book was net sold as gross trading activity increased for the second straight week, driven almost entirely by short sales. Macro Products were heavily net sold driven by short sales and to a much lesser extent long sales – this week’s short sales in Macro Products was the largest since Sep ’22.” Noteworthy is the big MOC sell order on Friday.

GS

…but before you get too bearish

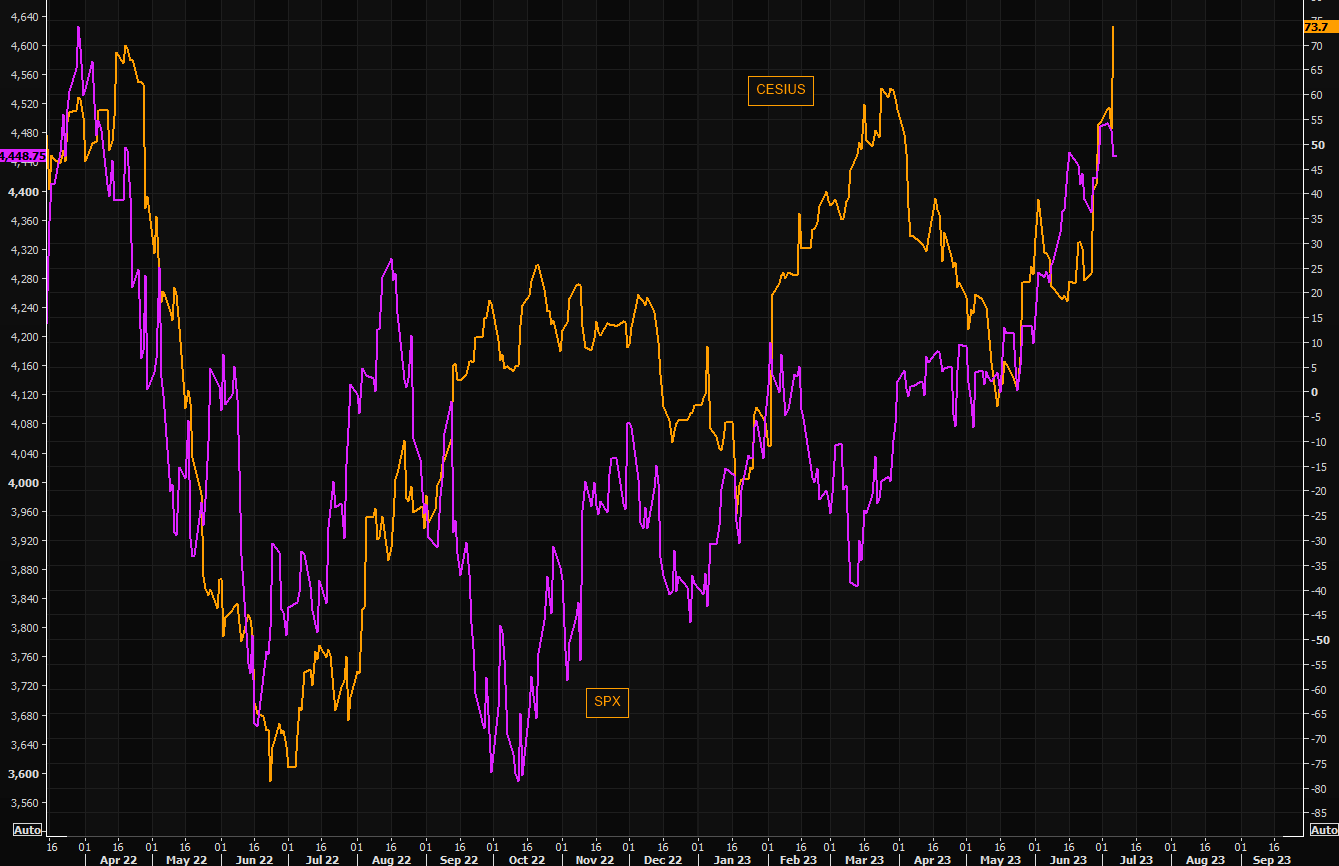

Citi US economic surprises index is “breaking up”. CESIUS ad SPX have moved in tandem.

Refinitiv

Such stretched readings on economic surprises are usually contrary signals, in this case, bearish.

The AI bubble has dragged the economy up via positive impacts upon consumption, as expected. But, now it is backing up rates as well.

Inflation is not beaten so the Fed must keep chasing the bubble.

Sooner or a little less than sooner, this thing will come apart and leave the financialised real economy naked and alone before the searing glare of very high-interest rates.