Three data releases today. First, Business Indicators:

| Dec Qtr 22 to Mar Qtr 23 (%) | Mar Qtr 22 to Mar Qtr 23 (%) | |||

|---|---|---|---|---|

| Sales of goods and services (Chain volume measures) | ||||

| Manufacturing | ||||

| Trend | na | na | ||

| Seasonally Adjusted | 3.6 | 1.9 | ||

| Wholesale trade | ||||

| Trend | na | na | ||

| Seasonally Adjusted | 2.3 | 0.7 | ||

| Inventories (Chain volume measures) | ||||

| Trend | na | na | ||

| Seasonally Adjusted | 1.2 | 4.1 | ||

| Company gross operating profits | ||||

| Trend | na | na | ||

| Seasonally Adjusted | 0.5 | 7.1 | ||

| Wages and salaries | ||||

| Seasonally Adjusted | 1.8 | 11.4 | ||

Inventories are much higher than expected and will add to 0.3 or so to GDP.

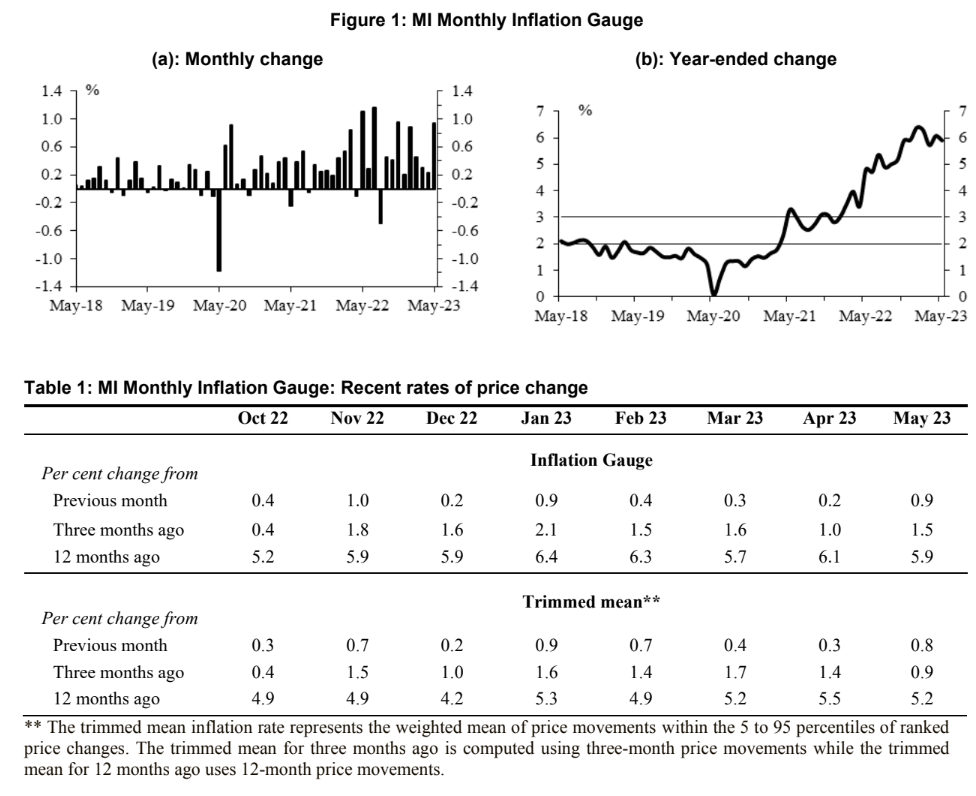

Second, Melbourne Institute’s monthly inflation exploded in May. The gauge was up 0.9% and 5.9% over the year.

Trimmed mean was up 0.8% and 5.2% over the year:

Third, ANZ job ads rose in May:

ANZ-Indeed Australian Job Ads bucked its recent downward trend and rose by 0.1% m/m in May. The series is currently 51.9% higher than pre-pandemic levels. @MadelineDunk @CallamPickering @MBansi @Felicity_Emmett #ausecon pic.twitter.com/1wozz4fPW7

— ANZ_Research (@ANZ_Research) June 5, 2023

All three of these are marginal indicators but they are all pointing one way. The economy is stabilising before inflation is beaten.

Two words for ya: house prices. The RBA needs them to fall further not rise.

My bet is a hike tomorrow.