It is my view that the US entering a goodly recession. Perhaps less understood is that Europe is not far behind. This has been disguised by the China reopening.

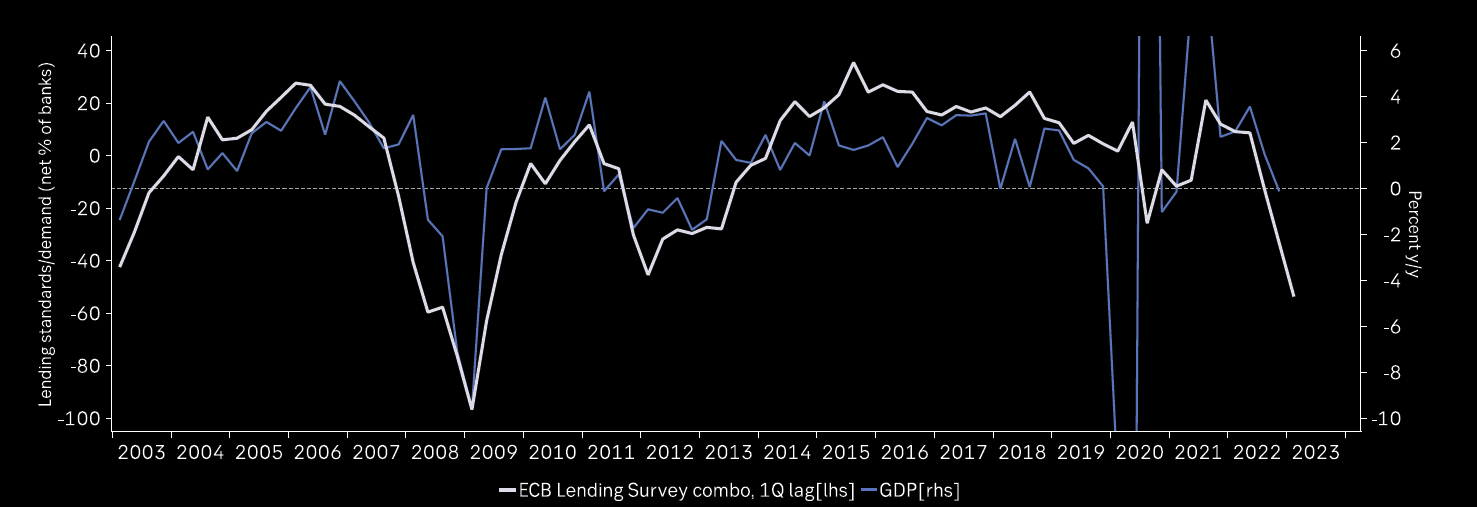

Bank credit negative ouch:

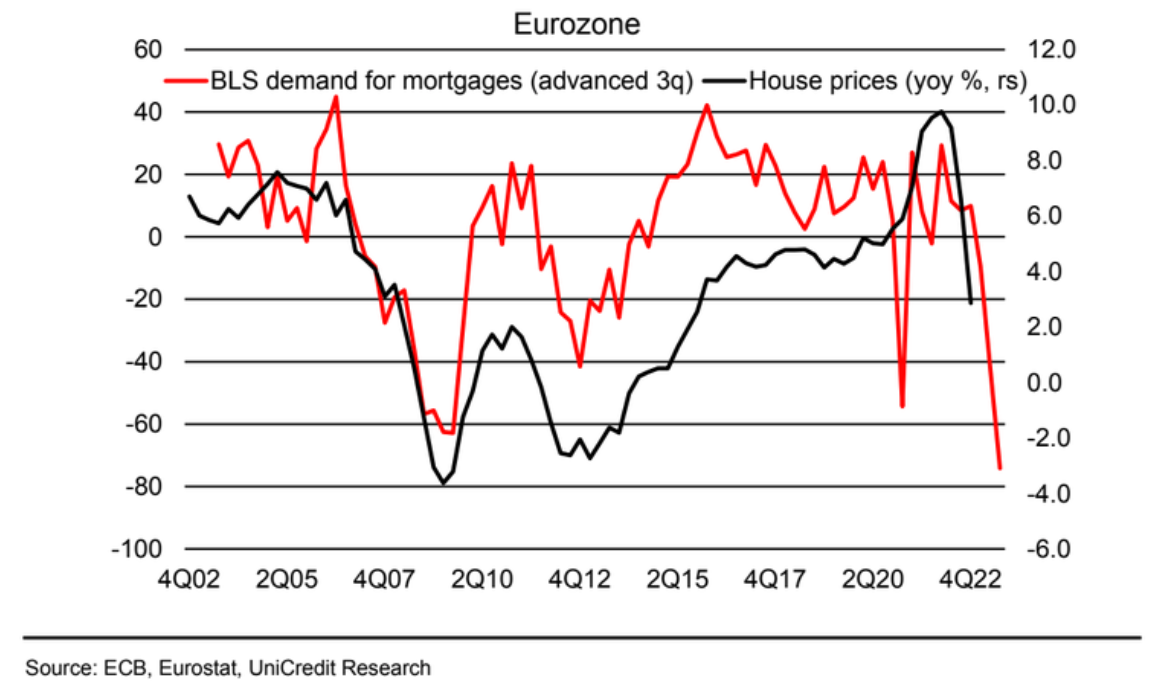

European property markets are breaking down as well. Unicredit with the detail.

This morning, Eurostat published data for residential real estate prices in the eurozone for 4Q22. The message is clear: the price correction in the real estate sector has started. We think that further weakness is in the pipeline, as the Bank Lending Survey (BLS)points to a quick deterioration in mortgage demand in response to aggressive rate hikes by the ECB.

■At the eurozone level, house prices dropped by 1.7% qoq, the first quarterly decline since early 2015 and the largest since the start of the Eurostat time series in 2005. The drop was especially pronounced in Germany (-5% qoq), Finland (-3.4%) and the Netherlands (-2.6%). In yearly terms, price increases in the eurozone decelerated markedly to 2.9%, from around 10% at the beginning of 2022. While most of this adjustment reflects weaker demand amid higher interest rates, it is possible that some supply effects might also be at play as the price of new homes starts to reflect the easing of shortages of construction materials and equipment.

■Overall, the correction in the housing market does not come as a surprise, although the latest data show that weakness has been more intense and has materialized earlier than we had expected. Such correction has implications for the economic outlook, primarily through reduced residential investment, but also via direct consumption effects (especially for housing-related durable goods), wealth effects and collateral effects.

■However, the impact on financial stability is likely to remain contained. At the household level, tight labor markets, sound balance sheets and limited exposure to floating-rate mortgages should prevent the emergence of distress and fire-sales of houses, while the price correction will reduce some of the overvaluation triggered by the pandemic. At the banking-sector level, comfortable capital buffers and prudent provisioning substantially reduce the risk of a credit crunch.

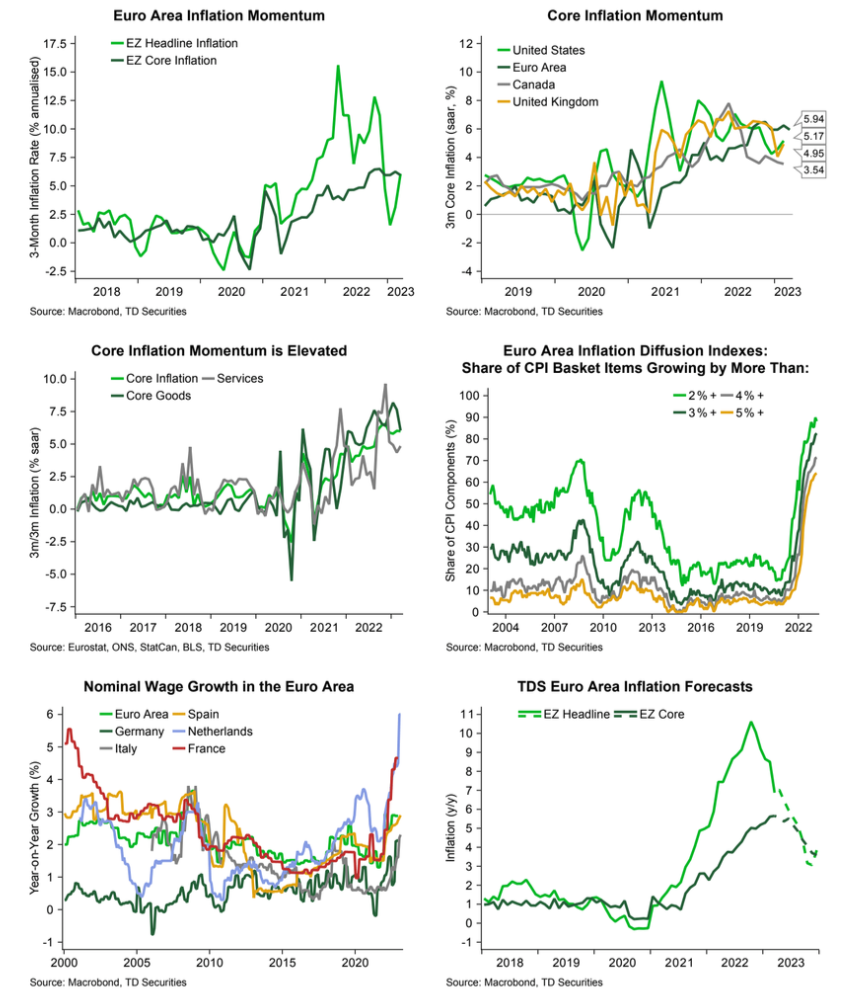

And the ECB is trapped. TD Securities has more.

The widely-accepted pre-COVID view was that euro area (core) inflation was sticky below 2%. This characterisation might not have changed much, even if the backdrop has: core inflation has been incredibly sticky at elevated levels too. The 3-month annualised rate of core EZ inflation has been in the 5.8%-6.5% band since September 2022, with few signs of deceleration. This is high on an international basis.

•The surprising feature of this is how strong core goods inflation has been. It too has been range-bound since June 2022 between 6.0%-8.2% on a 3-month annualised basis.

•Inflation remains broad-based in the euro area as well, with the diffusion index showing 64% of CPI basket items growing by more than 5% y/y, second only to the UK in the G4, and still rising.

•The backdrop is not encouraging: though the data is lagged, nominal wage growth continues to accelerate across the region, reaching new highs. We expect both headline and core inflation to be between 3.5-4.0% y/y by end-2023.

•While recent banking stresses will likely dampen demand a touch in the region, absent any renewed stresses, we expect the ECB to continue hiking at its May&June meetings, reaching a terminal rate of 3.50%. If the ECB needs to go higher, the risks skew to further 25bps hikes from July rather than a 50bps hike in May.

Maybe. Then again, if the US recession comes on quickly, a rising likelihood given the credit crunch there, then Europe will suffer the combined effects of rising bank funding costs and a trade shock.

Either way, Europe is going into recession this year as well.

This is one major reason why I do not trust the rally in EUR or the selloff in DXY.