Westpac with the note:

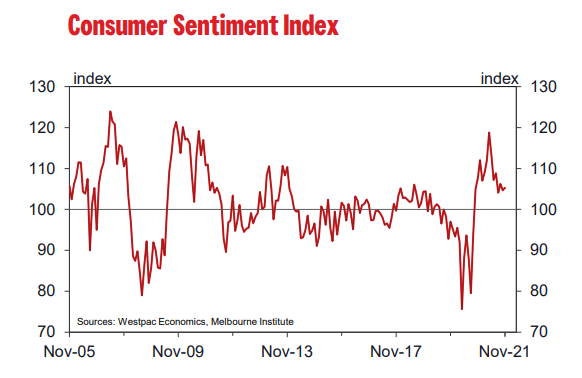

While the movement in the Index is hardly noteworthy there are a number of intriguing aspects of the survey that provide us with useful evidence of how the economy is evolving as we emerge out of COVID.

These include insights into spending patterns; the labour market; the impact of a changing interest rate scene; industry developments; and housing.

Firstly, the level of the Index is almost identical to the level just over a year ago in October 2020 (105.0) and has remained steady over the last two months despite both Sydney and Melbourne having moved out of their hard ‘delta’ lockdowns since September.

In contrast, the Index had surged 32% over the two months to October 2020 as the nation heaved a sigh of relief that Victoria’s ‘second wave’ COVID outbreak was finally coming under control and that other states had successfully avoided a return bout. That was a time when respondents were still very uncertain about the outlook and the risks associated with COVID.

In recent months the success of vaccination rollouts has underpinned a confident consumer despite being in lockdown. This is best demonstrated by the confidence level of the 7.8% of respondents who do not plan to get vaccinated with their confidence level at a disturbing 73.8 compared to confidence amongst the fully vaccinated at 106.5.

Confidence levels around the states are largely unchanged from the October survey with only NSW, up 4.4% to 107.9, showing a clear positive response to reopening news.

The November sentiment print is particularly important given the lead-in to the Christmas shopping season. Expanding on this, our November survey includes an additional question about Christmas spending intentions, asking consumers whether they plan to spend less, the same or more on gifts than last year.

We have been asking this question since 2009 and compared with previous surveys the results are generally encouraging. The proportion of respondents who are planning to spend less is 26% – the lowest proportion on record. That said, only about one in ten consumers actively plan to spend more this year, a relatively low proportion, with just over 60% expecting to spend the same.

Overall, the net proportion of ‘spend more minus spend less’ is the second best since the survey began. It seems that consumers are determined not to allow their spending to slip back further while at the same time being cautious about over-extending.

In recent weeks there has been considerable volatility in financial markets which have moved to price in the prospect of multiple increases in the Reserve Bank’s cash rate in 2022. Markets were partly soothed by the RBA Governor’s commentary following the recent Board meeting although the decision by the Board to no longer provide explicit guidance that interest rates will likely remain on hold until 2024 may have still unnerved some.

Certainly, sentiment amongst mortgagors points to some concern about a potential rise in rates. Overall confidence of respondents with a mortgage fell by 5.2%, with their expectations for finances over the next 12 months plunging by 7.5%.

This shift in tone around interest rates also looks to have weighed more generally on the finance-related components of the Index: the ‘finances compared to a year ago’ sub-index was down 4.5%; and the ‘finances, next 12 months’ sub-index fell 0.7% (the latter highlighting the significance of the 7.5% fall amongst mortgagors).

Against this, the reopening of the major cities looks to have shored up confidence in the economic outlook: the ‘economy, next 12 months’ sub-index lifted by 3.3% and the ‘economy, next five years’ sub-index was up 2.6%.

There was also a modest improvement in attitudes towards major purchases, the ‘time to by a major household item’ sub-index up 1.8%. This component is still down 7.7% on November 2020 but some of this softness likely reflects the high starting point for durables spending which has surged 15% during the COVID pandemic. The combination of some ‘saturation’ in durables spend and easing restrictions in Sydney and Melbourne, and on travel, suggests we are likely to see a significant rebalancing in spending from goods back towards services and experiences – a view that also looks to be supported by the responses to our question on Christmas spending plans.

However, by far and away the most stunning development was around labour market expectations. The Westpac Melbourne Institute Unemployment Expectations Index fell 11% from 107.1 to 95.3. Recall that the Index measures expectations for unemployment over the next 12 months – a lower reading indicating more consumers expect unemployment to fall than rise, a positive signal for confidence in the jobs market.

Indeed, this is the lowest level for the Index since the mid-1990s, when resurgent growth was finally starting to see sustained declines in unemployment from the very high levels of the early 1990s recession. Confidence is at historic highs for both males and females although the confidence amongst females is particularly buoyant – near all-time record levels going back to 1975.

Employees in the following industries are the most confident about the job situation: real estate; accommodation and food; media and telecommunications; health care; and retail. This may be an indication of where labour shortages are likely to emerge in coming months.

Home-buyer sentiment improved in the month but remains sharply lower compared to a year ago. For much of the year, we have been highlighting significant falls in the ‘time to buy a dwelling’ index. As at last month the index had declined 37% from its peak in November 2020 – a clear sign that rising prices and deteriorating affordability were weighing on buyer sentiment, particularly amongst owner occupiers and prospective first home buyers. The Index bounced back by 9.4% this month to 91.1.

It remains at a weak level overall, still down 31% compared to a year ago but may be signalling some very early signs that some potential buyers are anticipating better prospects for affordability. NSW recorded a large 24% gain but was coming off a very weak October read (72.4, down 23%) while Victoria (up 2.4%); Western Australia (up 9.9%); and South Australia (up 27%) all lifted. Only Queensland (down 3.4%) showed a further fall.

The changing interest rate environment may also be starting to impact the outlook for house prices. The Westpac Melbourne Institute House Price Expectations Index fell by 2.3% in November but remains at a very high level of 169.4. The national result masked bigger falls in all the major states, except NSW.

Expectations fell 4.5% in Victoria, 11.8% in Queensland and 5.9% in Western Australia. These were partly offset by a 4.3% increase in NSW although this was again coming off a sharper 9.3% drop in October.

The Reserve Bank Board next meets on December 7. The Board indicated that its next policy decision will relate to its bond buying program which is scheduled to be reviewed at the meeting on February 1.

Westpac expects that the current weekly program of purchasing $4bn in AGS and semi and local government bonds will be reduced to $2–3bn with the next review most likely in May.

This decision will be based on the Board’s assessment of the pace of progress in achieving its objectives. If this is assessed as being satisfactory and the Board decides to reduce the program to $2bn in February it could cancel the purchase program altogether by May