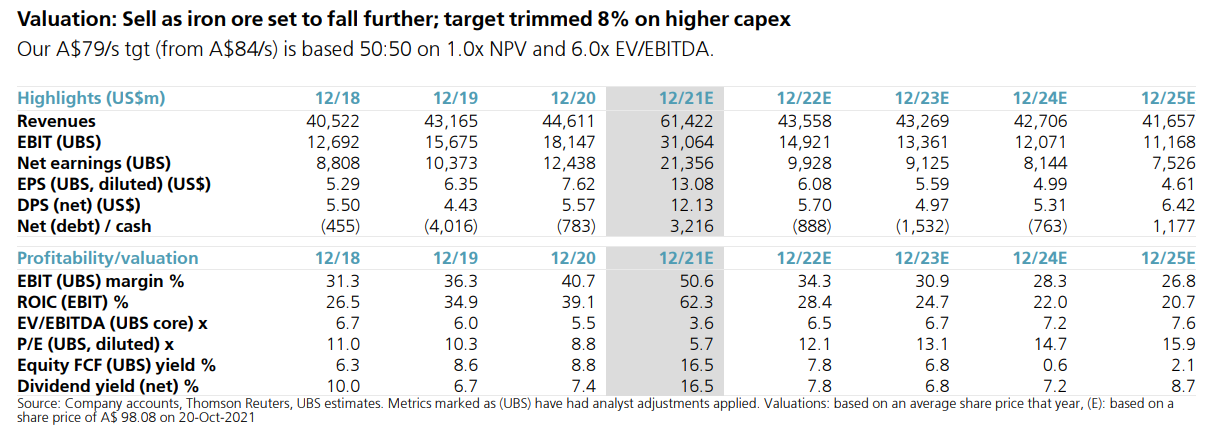

RIO’s new mgmt team set out its strategy to focus on operational performance,

ESG credentials & growth, while rebuilding trust after Juukan Gorge. It aims to cut its Scope 1&2 emissions faster (-50% by 2030) at a cost of ~$7.5b. RIO pivots the business more towards growth in energy transition commodities, lifting 2023/24 capex to $9-10b (from ~$8.5b). RIO now looks beyond ‘Tier 1’ assets & low-risk jurisdictions and considers M&A; in our opinion, Simandou & Saguenay Al growth are more likely. We trim forecasts for higher capex/opex & cut NPV ~10%; this results in our tgt falling ~8%.

1) Decarbonisation: high capex to future proof the portfolio, returns uncertain

(1) Decarbonisation: RIO lifts its 2030 Scope 1&2 CO2 target reduction to -50% vs 2018 base (from -15%); in 2020 S1&2 emissions totalled 32Mt. The ~16Mt CO2 reduction will come from: Pilbara renewables (~1Mt from deploying ~1GW of renewables to replace gas-based power for fixed plants; these emit ~33% of total Pilbara emissions); repowering PacAl (~5Mt reduction at Tomago & Boyne Island; this requires 5+GW of renewables (RIO share) costing $5-7.5bn); various abatement projects (~4Mt of which ~50% are NPV positive); and other energy efficiencies, ELYSIS (new Al inert anode technology) & carbon offsets. RIO expects to spend $7.5bn on decarbonisation by 2030, with $0.5b pa in 2022-24 (mostly Pilbara renewables) and $5b in 2025-30. ELYSIS is on track for commercial scale technology in 2024. RIO expects decarbonisation to ‘future-proof’ the portfolio, but the benefits to shareholders are hard to value. With Scope 3 (519Mt CO2 in 2020), RIO looks to provide targets in Feb-22.

2) Pivoting to growth; 3) M&A opportunistically; 4) Pilbara volumes to lift

(2) Growth: RIO looks to double growth capex to $3b pa from 2023, growing in copper, battery raw materials (eg Jadar) & high-grade iron ore (eg IOC, Simandou); it will look beyond “Tier 1” assets & low-risk jurisdictions. RIO still discusses infrastructure sharing at Simandou with SMB-Winning; it will not compromise on ESG. RIO expects to double copper production to 1.2Mtpa from OT (+400kt), Resolution, Winu etc; the discussions on licences/ power etc continue with the Mongolian govt. (3) M&A: RIO looks to opportunistically grow inorganically; it aims to maintain “Single A” credit metrics but would allow this to fall temporarily for the right acquisition. The capital allocation process is unchanged. (4) Pilbara: RIO expects to lift production to 345-360Mt (from 320-325Mt in 2021) as its new replacement mines (+90Mt) & Gudai-Darri (+43Mt) ramp up. RIO flags more replacement mines are needed in 2023-24; opex is challenged by a higher work index though Gudai-Darri will improve mix & strip ratio.

This is based on an iron ore price of $80+ in 2022. Too bullish for me!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.