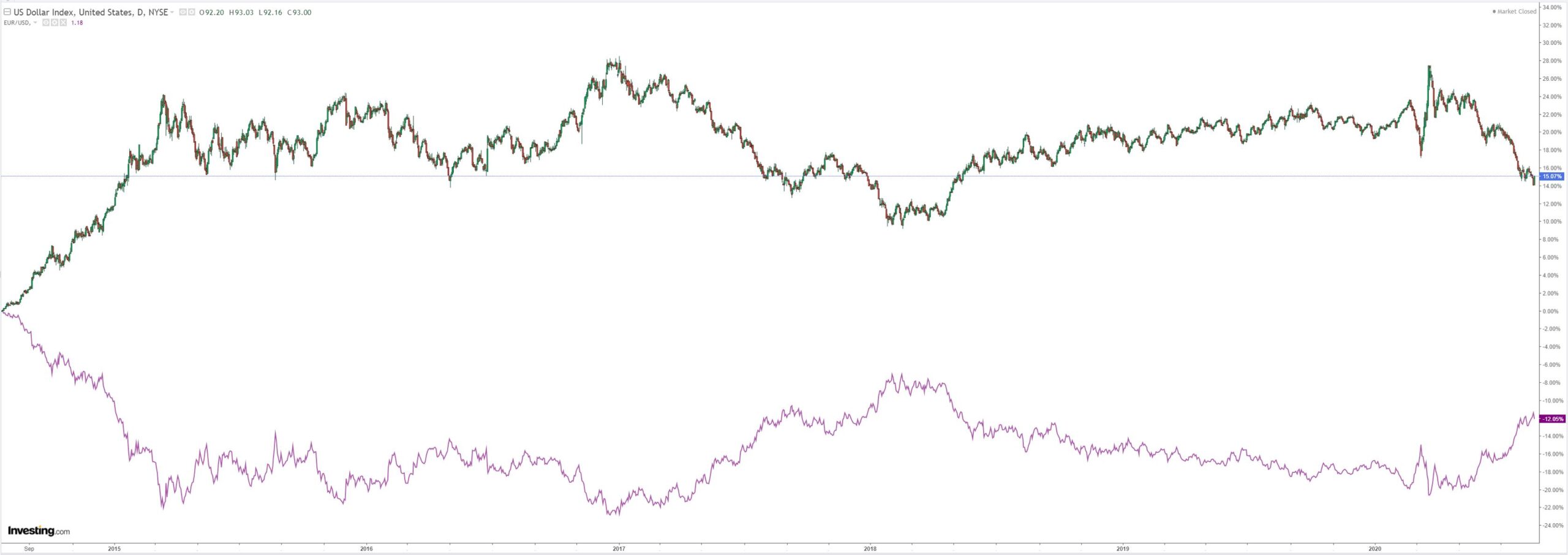

DXY roared back last night:

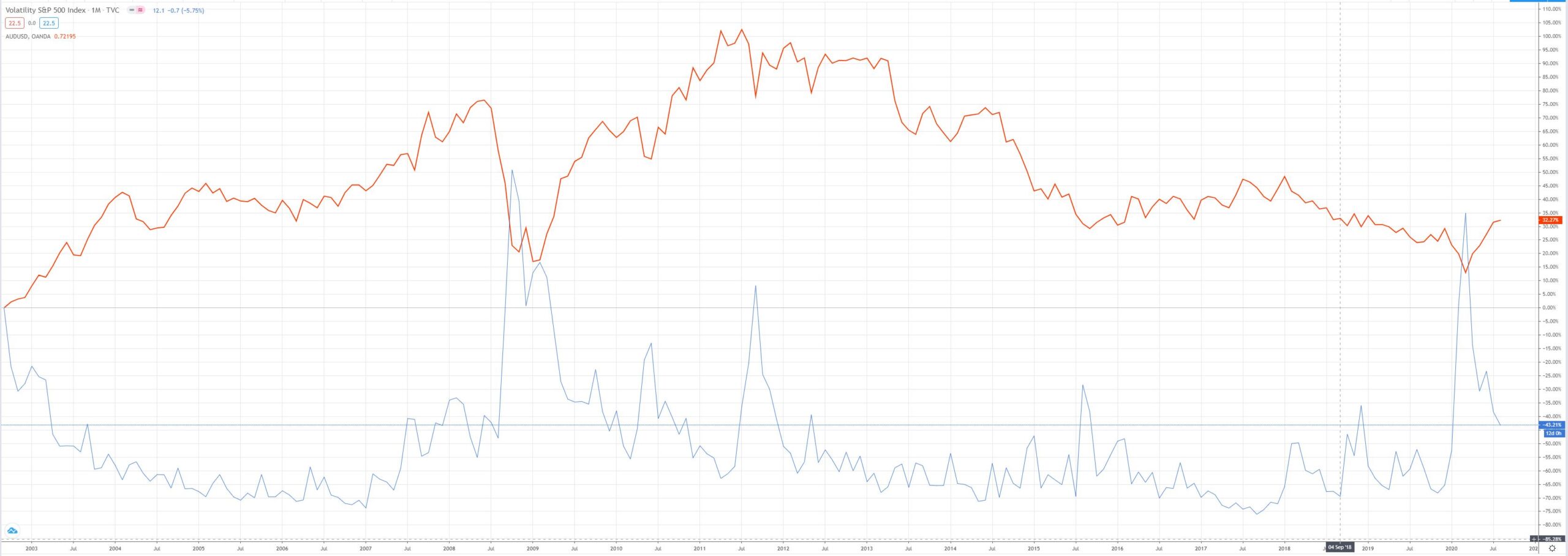

The Australian dollar was bashed:

Gold was creamed:

WTI is bid by a robot:

Metals did OK:

Miners not:

Nor EM stocks:

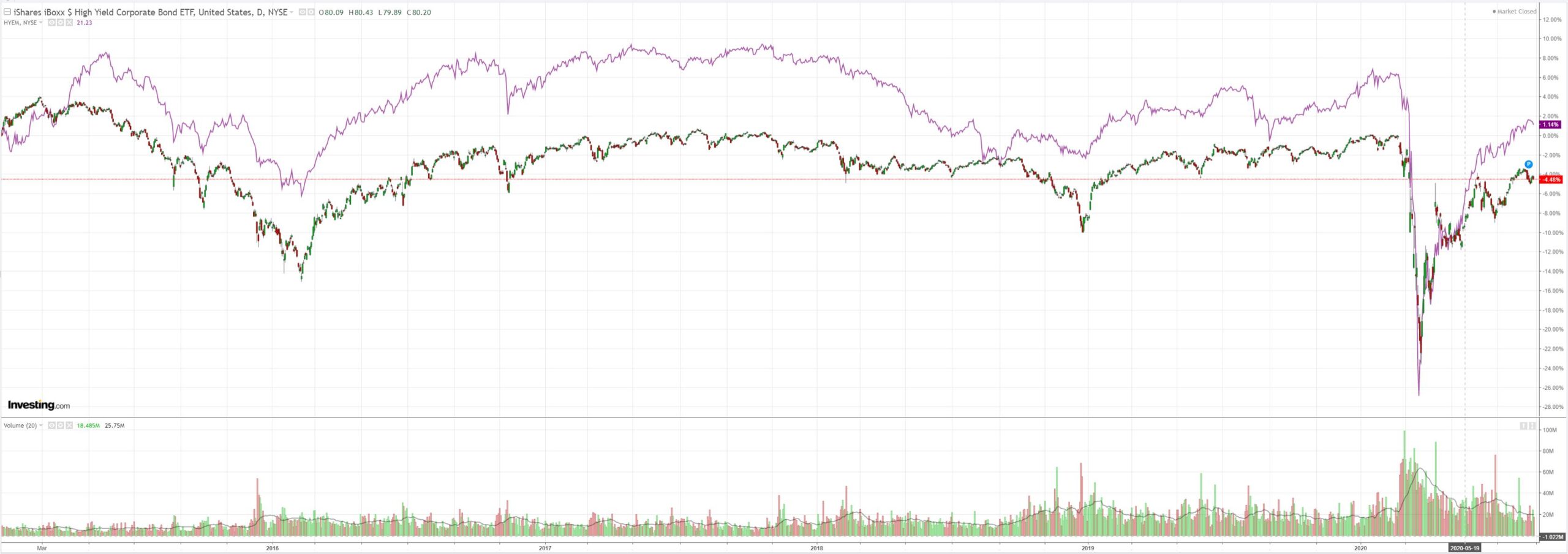

Or junk:

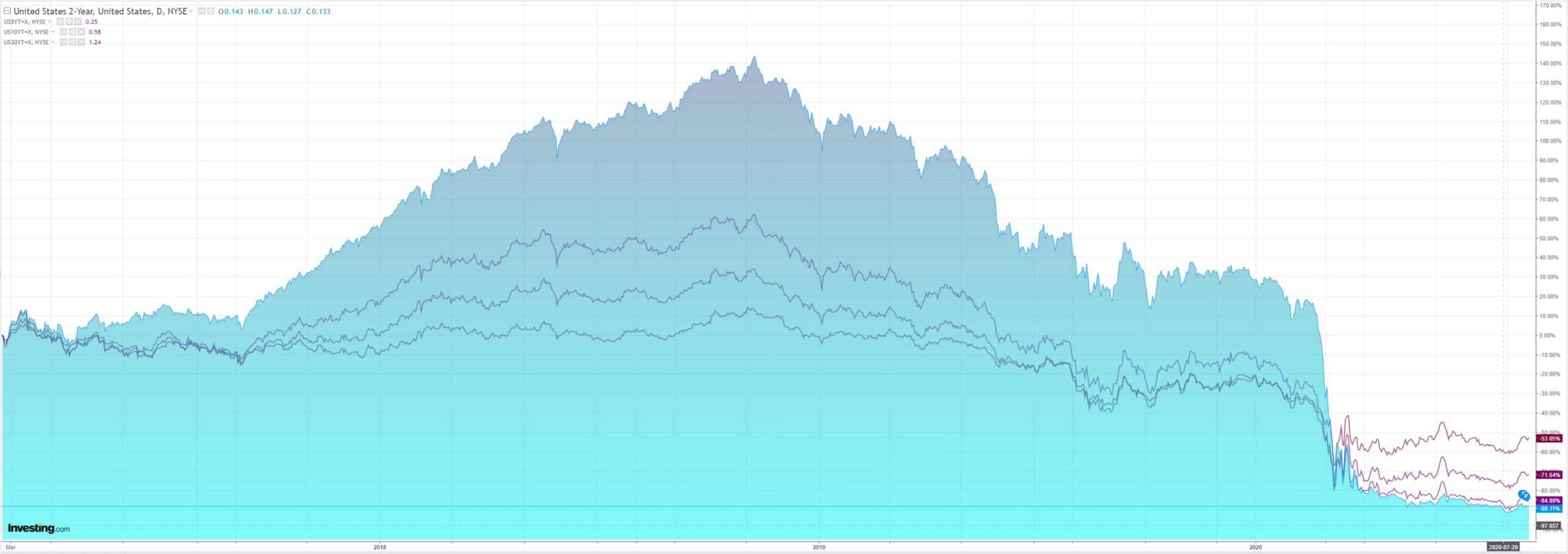

Yields lifted:

And stocks fell:

The culprit was Fed minutes which simply weren’t dovish enough:

Participants observed that uncertainty surrounding the economic outlook remained very elevated, with the path of the economy highly dependent on the course of the virus and the public sector’s response to it. Several risks to the outlook were noted, including the possibility that additional waves of virus outbreaks could result in extended economic disruptions and a protracted period of reduced economic activity. In such scenarios, banks and other lenders could tighten conditions in credit markets appreciably and restrain the availability of credit to households and businesses. Other risks cited included the possibility that fiscal support for households, businesses, and state and local governments might not provide sufficient relief of financial strains in these sectors and that some foreign economies could come under greater pressure than anticipated as a result of the spread of the pandemic abroad. Several participants noted potential longer-run effects of the pandemic associated with possible restructuring in some sectors of the economy that could slow the growth of the economy’s productive capacity for some time.

A number of participants commented on various potential risks to financial stability. Banks and other financial institutions could come under significant stress, particularly if one of the more adverse scenarios regarding the spread of the virus and its effects on economic activity was realized. Nonfinancial corporations had carried high levels of indebtedness into the pandemic, increasing their risk of insolvency. There were also concerns that the anticipated increase in Treasury debt over the next few years could have implications for market functioning. There was general agreement that these institutions, activities, and markets should be monitored closely, and a few participants noted that improved data would be helpful for doing so. Several participants observed that the Federal Reserve had recently taken steps to help ensure that banks remain resilient through the pandemic, including by conducting additional sensitivity analysis in conjunction with the most recent bank stress tests and imposing temporary restrictions on shareholder payouts to preserve banks’ capital. A couple of participants noted that they believed that restrictions on shareholder payouts should be extended, while another judged that such a step would be premature.

No mention of yield curve control or negative interest rates or pushing out the bond curve when all of them are already priced into everything.

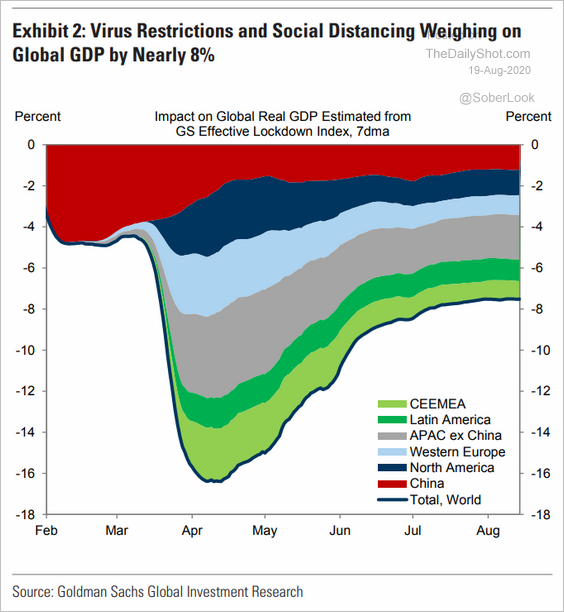

And why wouldn’t they be? The global depression is immense and absolutely entrenched despite already unprecedented stimulus:

V-shaped recovery my butt.

It looks like the Fed will need some reminding of who is boss with a little bit of volatility. If so, stand by for more AUD clubbings: