Fed Chair Powell guides negatively. In an ad hoc speech, Fed Chair Powell said that the economy faces unprecedented risks from COVID-19 if fiscal and monetary policy makers do not step up to the challenge. He suggested that the recovery could take time to gather momentum, and that the present liquidity crisis could morph into a solvency crisis. Interestingly, when the speech was scheduled late last week following money market pricing of negative rates for the first time in history, investors thought that Powell would directly address the issue of negative rates in prepared comments, or perhaps deliver an upbeat economic outlook. But he did neither. In response to Powell’s warnings, equities sold off, bonds were little changed, the USD strengthened and gold rallied. Within equities, value factors badly underperformed, while momentum and quality factors outperformed. All in all, a class risk off response.

No to negative rates ... for now. Although Powell did not directly address negative rates in prepared comments, he did respond to a question about them afterwards. Powell said that the Fed’s view on negative rates had not changed. While conceding that some people have argued their merits, Fed officials have observed mixed results in the international experience with them. They have not been considering them as a real option recently, and indeed, have maintained a strong preference for other tools that have been used so far. Interestingly, since Powell and other Fed officials have spoken about negative rates, money markets have priced them out of the curve – but only just.

Never say never. Presumably, Powell was referring to the use of quantitative easing (QE) in the past to achieve the same easing as negative rates, without the perverse deflationary side effects from taxing the banks and savers. However, because of circumstances that have burdened the Fed with setting global, rather than local monetary policy – the so-called Triffin dilemma – it might be possible for negative US rates to support other economies that have imported US monetary policy to a degree. Perhaps this is why the USD rallied in response to Powell’s comments ruling out negative rates. Also, we note that Wu-Xia estimates of the shadow Fed funds rate, with have tacked on the effects of QE suppression of bond yields to achieve hypothetically negative policy rates, did not quickly reach the depths prescribed by our “Taylor” rule in the previous crisis. Negative rates might not be currently under consideration because of the hope that fiscal policy makers might do more leg work. However, the temptations for the Fed to “go there”, not wanting to put all hope in other arms of policy, seem very real, especially if officials have started to consider scenarios where a solvency crisis follows a liquidity crisis.

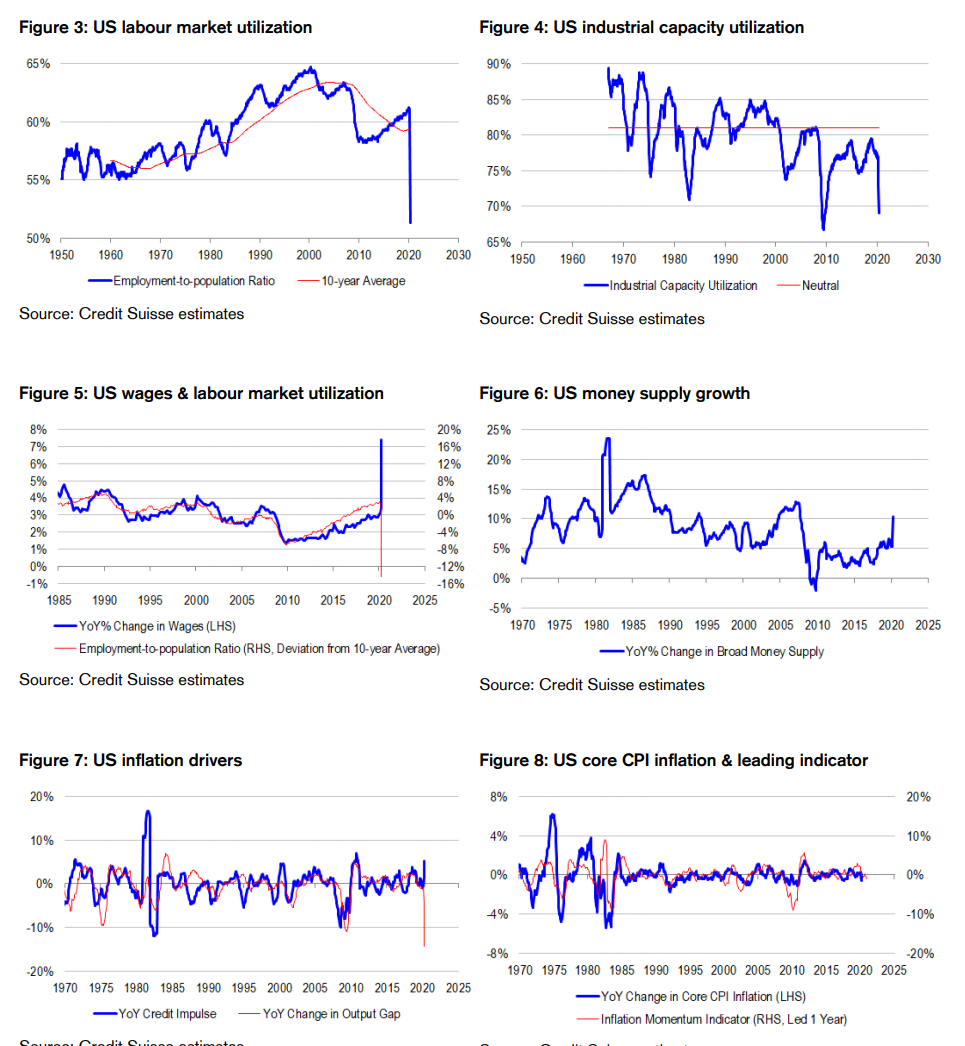

Positioning for uncertainty, not outcomes. The jury is still out on whether negative rates will actually be put into effect or not. But for us, the risks are more worthwhile positioning for than the outcome itself. We note that the different drivers of inflation are significantly diverging at present, with credit and money supply growth accelerating, but slack increasing. Forecasting inflation carries with it more risk than before. Indeed, actual wage inflation outcomes are deviating from bleak labour market outcomes. The dispersion of inflation leading indicators necessarily flows into policy. As it stands our “Taylor” rule prescriptions for Australian and US rates are deviating quite far from policy rates at the zero bound. In the first instance, the higher tracking error that monetary policy makers are running means that interest rate volatility should rise. Interestingly, our measures of (rolling) Fed tracking error and dispersion of inflation leading indicators are highly correlated with measures of market pricing of rates volatility such as the MOVE index. Therefore, the rises in tracking error and dispersion should drive market pricing higher as well. Further, the rise in rates volatility should support higher bond yields, even as discussion about QE and negative rates pulls pricing in the opposite direction. But if monetary policy makers choose to suppress rates volatility as well through forward guidance and QE, something else has to give. And that something is currency valuation against gold. Historically, when the market price of interest rate volatility is low relative to our estimate of the Fed’s tracking error, gold prices tend to rise. Gold prices rise for other reasons too of course – but the linkage with rates volatility suppression is very hard to ignore. Indeed, rates volatility suppression is a powerful leading indicator of the gold price. Right now, actual Fed tracking error is high and rising, while priced rates volatility is very low. The Fed is trying to have its cake and eat it too – but gold investors are pouncing on the crumbs that fall from the table. Many view gold as an asset to buy when one is positioning against the system, and our analysis arguably supports this claim. Interestingly, from a factor investing perspective, our dynamic factor weights are giving us very similar signals. We are positioning against conventional quantitative processes by both shorting momentum and value, while going long on quality. And interestingly, this factor combination favours resources stocks over bond proxies, consistent with our thesis about the costs of artificially suppressing rates volatility in such a fluid macro environment.

Too many variables to solve for, not enough equations. We think that the Fed is too burdened with too many policy objectives. It needs to set rates appropriately for the US economy. It needs to set rates for the world. It needs to keep bond yields low to support asset pricing. It needs to suppress volatility to prevent passive and risk parity investors from rushing to the exits. And now, it needs to keep a lid on gold prices, because rising gold prices either signal longer-term inflation risk or longer-term systemic risk. Perhaps this context explains why Powell is addressing the evolving nature of the crisis from liquidity to solvency. Clearly, the Fed needs to compromise between the different objectives it has to the extent that they compete. But investors are clearly worried that the compromise might not be favourable nor predictable. If only COVID-19 would go away quickly to make all of the constraints go away! But this is clearly not happening, and indeed, needed to happen yesterday given the extensive damage already caused by the disease and the response to it.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.