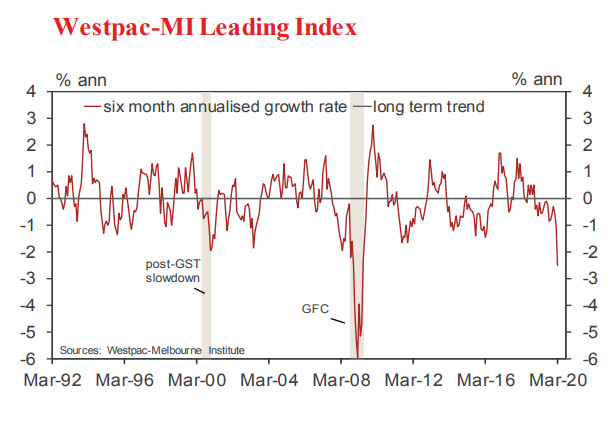

The sharply weaker signal is consistent with a deepening economic impact from the Coronavirus pandemic. The Leading Index growth rate in March is the most negative seen since the Global Financial Crisis.

Moreover, while it may still be well above the deep lows recorded in 2008-09 and in recession periods historically, two of the components in the latest update have dominated the impact of the Coronavirus disruptions. These components – US industrial production and the ASX 200 – capture the direct impacts of the virus on the global economy and financial markets. The impact domestically via sectors such as housing activity and employment will be captured more fully in coming months.

On March 31 Westpac forecast that the Australian economy would contract by 8.5% in the June quarter of 2020 and, following a strong rebound in the December quarter, would contract by 5% over the full course of 2020. Yesterday, the Governor of the Reserve Bank forecast a similar profile with a contraction in 2020 of 6%.

The Leading Index growth rate has now deteriorated 1.7ppts over the last six months, from -0.76% in October to –2.47% in March. Just two components account for all of the decline: US industrial production (–1ppt) and the ASX200 (–1ppt). Both components weakened sharply in the March month: US industrial production falling 5.4%, the biggest monthly decline since World War 2; and the ASX slumping 21%, the worst monthly fall since the share market crash in 1987.

Other components have been more mixed with a significant drag from sentiment-based indicators such as the Westpac-MI Consumer Expectations Index (–0.15ppts) the Westpac-MI Unemployment Expectations Index (–0.13ppts) but little change in the contribution from actual hours worked and more positive support from dwelling approvals (+0.31ppts), the yield spread (+0.18ppts) and commodity prices measured in AUD terms (+0.13ppts).

The Reserve Bank Board next meets on May 5 while the Bank is also due to release the full set of economic forecasts in its May Statement on Monetary Policy on May 8.

In the Governor’s speech yesterday and in the Board Minutes for the April meeting, which were also released yesterday, the Bank confirmed its commitment to do whatever is necessary to hold the three year bond yield at 0.25%. The commitment that the target cash rate of 0.25% would not be increased before the bond yield target was relaxed was also confirmed.

Recall that in October 2009 the RBA increased the cash rate target only six months after the final GFC-related cut in April 2009. At that time there was a clear commitment from the Bank to move away from emergency policy settings.

The situation is different this time. The Governor has indicated that he expects current targets will be in place for a number of years.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.