From Morgan Stanley on the US market but a handy primer:

Key takeaways from our analysis of the energy storage market:

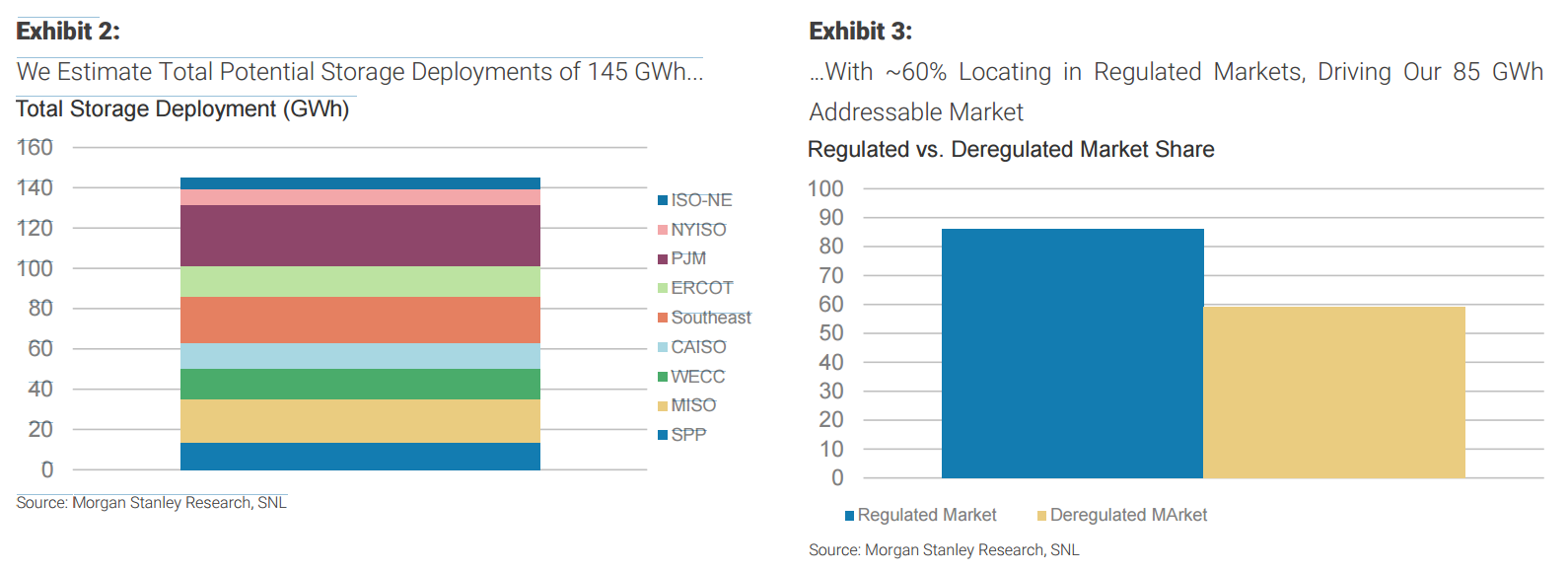

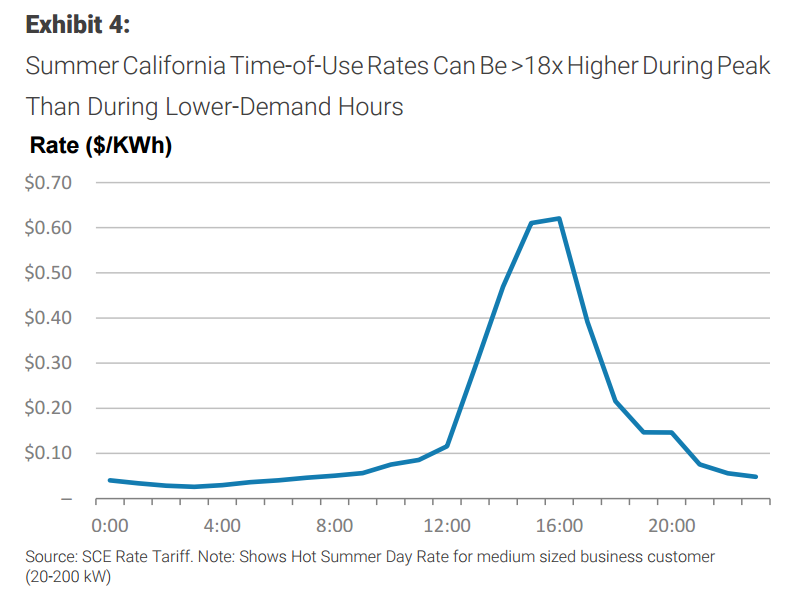

1. Demand for energy storage from the utility sector will grow more than the market anticipates by 2019-20, driven by the fallM ing cost of storage, greater renewable energy penetration, and greater utility focus on the many customer benefits of energy storage. Specifically, we project that demand for energy storage in the US will grow from <$300m per year currently to $2-4b per year by 2020, with a total addressable market of ~85 GWh, or $30b.

2. There is little understanding of the approach utilities will take to determine whether storage is in their customers’ best interests; looking across the US, we found that the collective benefits of energy storage are greater than appreciated. There are many state/regional studies of the benefits of energy storage, but one stood out to us for the depth of analysis into the numerous benefits: the Brattle Group assessment of energy storage in the ERCOT (Texas) market (the report is available here). We analyzed the benefits of energy storage in Texas, and applied this analysis to the rest of the US; this work became the basis for our analysis of the energy storage market.

3. Energy storage potential in the rooftop solar market is a small fraction of the demand we see coming from utilities, primarily because of solar net metering rules but also because distributed storage costs are in our view substantially higher than the costs of large-scale, utility-driven storage deployment. While we see limited storage deployments at rooftop solar installations in Hawaii and California, our analysis shows relatively poor storage economics in other states. If solar net metering rules change (such that excess solar power sold back to the grid receives a relatively low price) and storage costs drop significantly, there is potential for this market to grow, but we remain unconvinced that net metering rules will be changing broadly, other than in a few isolated instances such as in Arizona. For clients interested in better understanding the economics of storage in the rooftop solar market, please ask us for our financial model, which can be easily modified to fit specific dynamics in each US state.

The Brattle Group’s Analysis of Storage in the ERCOT (Texas) Market The Brattle Group, a market consulting firm, published (on behalf of its client Oncor, a large Texas utility) a comprehensive report on the economics of energy storage in the ERCOT market, which encompasses most of Texas. We believe FERC will not permit regulated utilities to deploy energy storage in the ERCOT market because it is a deregulated power market (see our ” The Key Regulatory Driver: Storage in Deregulated Markets ” section for a description of the issue and our view). However, we believe the Brattle Group’s approach to assessing the benefits to customers from the deployment of energy storage is helpful because we view it as a natural “lens” through which utilities across the US will determine whether, and to what extent, to deploy energy storage. The Brattle Group concluded that, at an all-in deployed capital cost per kWh of energy storage of $350, up to 15 gigawatt-hours (GWh) of storage could be deployed in ERCOT with a net beneficial impact to customers.

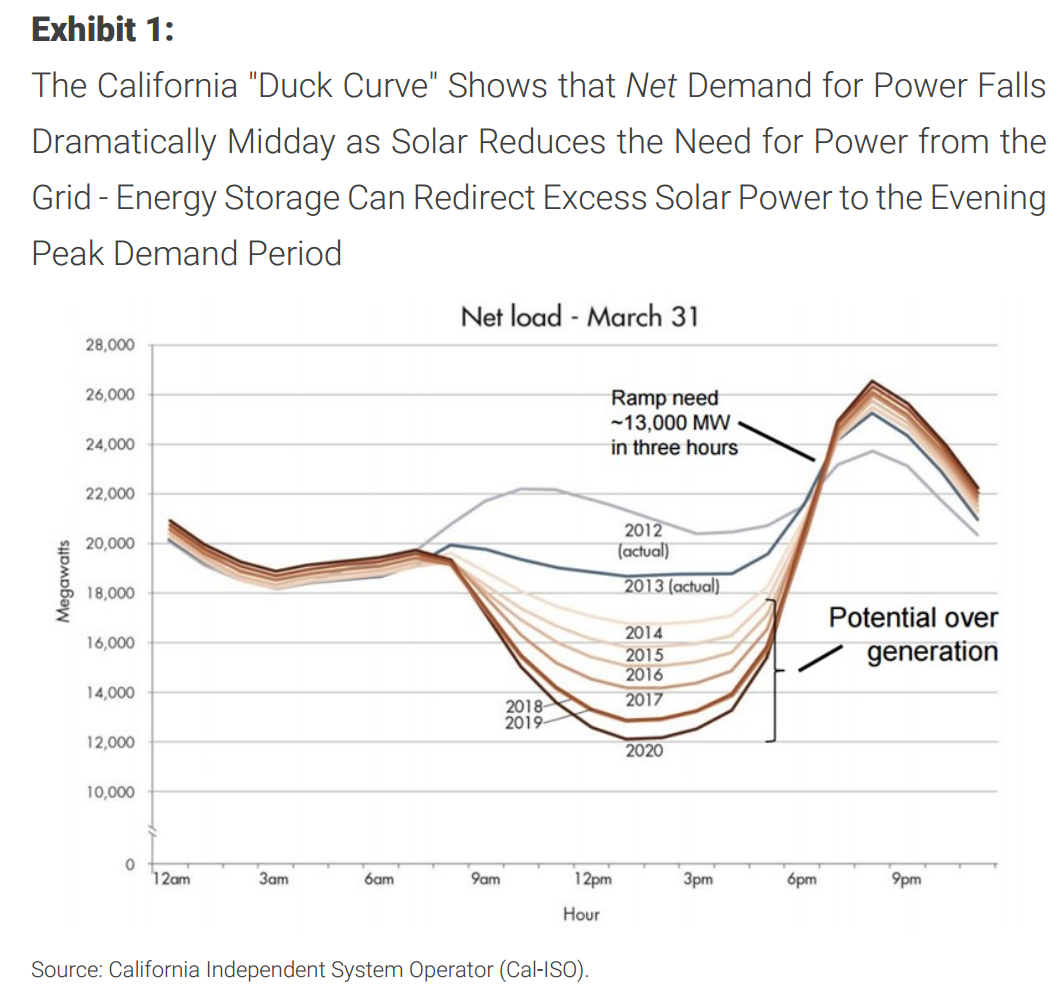

What is so important about the utility “lens” in analyzing energy storage? We think the benefits of storage are broader than appreciated. This perspective becomes especially important to understand as renewable energy penetration increases. As wind and solar energy become an increasingly important part of the US power generation mix (driven primarily by favorable economics, state-level clean energy goals, and federal tax credits passed by a Republican majority Congress), storage helps address a couple of key issues: the mismatch between when renewable energy is produced and when consumers want the power, and the inherent intermittency of renewable energy. The California “duck curve” is a useful starting point to understand the role of storage. This curve, shown below, highlights that net power demand from consumers (net of the large amount of solar power produced in the middle of the day) will fluctuate more widely throughout the course of the day/evening. Energy storage can help by storing excess power produced by solar midday/early afternoon (and wind at night) and releasing the stored electricity in the early evening and morning.

In the Brattle report, benefits of energy storage are classified in the following broad categories: 1. Margins that the energy storage system itself can realize by arbitraging the difference between on-peak and off-peak power, prices as well as providing market-driven grid stability services typically known as “ancillary services.” The Brattle Group found that the margin from this category of benefits was generally insufficient on its own to justify widespread energy storage deployment.

2. Collective grid benefits for all customers (not just the owner of the energy storage system), including lower grid outages, lower systemwide power prices and lower required grid expenditures through avoided power plant investment and greater utilization of grid infrastructure such as transmission lines. Based on these benefits, Brattle Group estimated that up to 15 GWh of energy storage could be deployed with net incremental benefits to customers (net of the cost of storage) for each GWh deployed.

Our methodology begins with the analytical framework developed by the Brattle Group that addresses the market potential for storage in ERCOT (Texas), and adapts this approach to important differences in regional power market dynamics. We define the addressable market as the deployment level at which there is no incremental net benefit to customers from deploying additional storage (i.e., the point at which incremental costs exceed incremental benefits). The Brattle Group found that the optimal battery deployment size in ERCOT was 5,000 MW, assuming 85% round-trip efficiency and 3-hour discharge, with a merchant benefit of approximately $430m/year. This merchant benefit, however, does not capture the total system-wide benefits of storage, which include power savings, reliability, and transmission & distribution functions. Brattle estimated that these non-merchant benefits represent 30-40% of total benefits. For our calculations, we quantify non-merchant benefits in ERCOT using 40% and equaling ~$286m/year.

1) Merchant benefits include only the profit that a battery storage operator would receive from dispatching into the wholesale market. To calculate the merchant benefit of storage, we chose representative regions from ISO-NE, NYISO, PJM, MISO, SPP, ERCOT, SOUTHEAST, CAISO, and WECC and analyzed daily real-time hourly power prices from the last five years. For each day we found the delta between the maximum and minimum daily power prices and averaged these daily values over five years. We then scaled these values by market size as well as the average price volatiltiy relative to our representative market, to arrive at an approximate merchant value benefit for each Independent System Operator (ISO). In most markets, merchant value was equal to ~56-64% of the total customer benefits. Importantly, the merchant value alone is not high enough in any US market to support deployment of storage, even under aggressive cost decline assumptions.

2) Power price reduction benefits: We quantified these benefits by scaling the average delta power prices and peak load of each ISO in relation to ERCOT. This accounts for differences in power prices as well as peak load sizes between the various ISOs. In the Brattle report, power price savings accounted for about $100m, or 14% of total storage benefit. We found a range of ~13-15% in other markets.

3) Other non-merchant benefits. We calculated these benefits by scaling the non-merchant benefit in ERCOT by the peak load of each ISO. Other non-merchant totaled about $186m, or 26% of total storage benefits in the Brattle report. We found a range of ~21-31% in other markets.

To find the optimal battery storage deployment, we took the total benefits (merchant +power savings+ non-merchant) for each ISO as a proportion of the total benefits calculated by Brattle in ERCOT and multiplied them by the total MW of battery deployment (5,000 MW) to obtain the MW volume of battery storage for each ISO. The higher the calculated total benefit, the higher the storage deployment value. Total deployment across all ISO’s equaled approximately 48 GW, or 145 GWh.

When considering the impacts to the power sector from energy storage, the most common response we hear is the ability of storage to replace the utility grid (i.e., for customers to go “off grid”). While in some geographies at some point in the future this may be a tangible risk/opportunity (depending on your perspective), for many years we believe other business models will prevail, not all of which displace the utility grid but instead enable the utility grid to continue to support the increased growth of renewables. In our view, the two most prevalent approaches will be: (1) a utility-driven approach in which utilities deploy storage (and earn a regulated return on capital deployed) as a way to enable the growth of renewables and/or defer transmission/distribution projects, and (2) a customer-driven approach in which solar customers reduce their peak power usage, resulting in many cases in significant utility bill savings. We discuss each potential business model below. In addition to these two business models, there is a third approach we think will be economically feasible but lead to smaller volumes of deployed storage: merchant developers deploying storage in deregulated markets to provide grid reliability services (known as “ancillary services”). Merchant deployment of storage solely for power price arbitrage between high and low price hours is not economically feasible even under very aggressive cost decline assumptions.

1) The utility-driven approach. We are sensing a significant degree of interest in energy storage among a number of US utilities, and we expect many utilities will begin to explore the deployment of significant amounts of energy storage, especially in light of the price levels disclosed by leading energy storage providers such as Tesla and LG Chem. There are numerous customer benefits that a utility can factor into its decision to invest in storage, and this “scope of benefits” is, we think, much broader than the scope of any other business model, as we highlighted in the previous section.

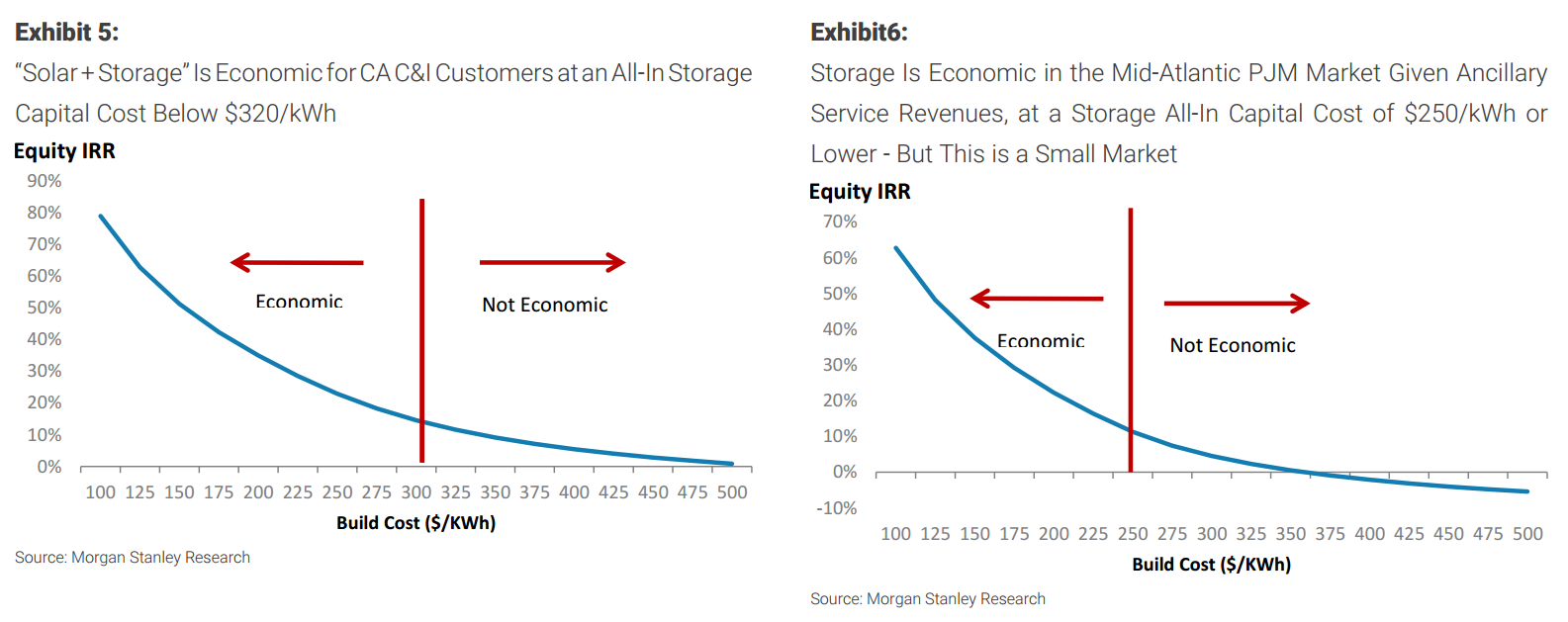

2) Batteries as demand response. Another business model that will, in our view, generate demand for energy storage is centered on customers using time-of-use rates could will use batteries as a form of demand response. In many power markets, such as California, there are very large differences between peak and off-peak power customer rates (much larger than that seen in wholesale power prices). Furthermore, demand charges, which are applied to customers based on peak usage levels, can be costly. The following are two approaches that can be taken, in which storage serves to “shave the peak”:

Solar + storage. Under this approach, solar customers would use storage as a means of reducing demand for power from the grid during peak demand (and pricing) periods. Because solar power output does not perfectly coincide with peak periods of demand for power, and because power prices during peak periods are often many multiples of the average price, storage can be a powerful tool to reduce solar customers’ power bills. A solar customer would store a portion of the power produced by the solar panels during lower priced daytime hours, and release this power during the highest priced peak periods rather than purchase incremental power from the utility at very high rates. This approach not only reduces costly energy purchases, but can also reduce a customer’s demand charge. Demand charges are designed to recover transmission and distribution grid costs, and are based on a customer’s peak usage. For a medium-sized commercial customer (20-200kW) in California, for example, demand charges can be $400-500/MW-day, and thus represent a meaningful portion of the electric bill. We conducted a preliminary analysis of the economics of this business model in California using Tesla’s storage pricing and performance characteristics, and we conclude that this approach would likely be economic with installed storage costs below $320/kWh.

Pure demand response. Storage could be used independently of solar power to reduce power bills, as per the solar + storage example above, and in some markets (such as the deregulated mid-Atlantic PJM power market), this service can be eligible for Demand Response revenues. For example, to the extent that using storage would reduce a customer’s maximum peak energy usage from the grid, storage can help customers reduce their total “demand charges,” which are often set based on the level of peak energy usage. We would note the joint venture between EnerNOC (a leading Demand Response provider) and Tesla as an example of this approach.

3) Merchant applications of battery storage. The third business model involves merchant developers deploying storage in deregulated markets to provide grid reliability and power price arbitrage services. While we estimate that the economics of grid reliability services are feasible using Tesla’s battery technology in some US power markets, we do not see power price arbitrage alone as viable given current on-peak / off-peak price spreads. Furthermore, while grid reliability service applications for batteries do have compelling economics in some instances, the demand for this service is very limited, keeping the addressable market small. In PJM, for example, the largest deregulated power market in the US, total demand for the grid support service most relevant for batteries is only ~725 MW. Storage penetration above this level does not provide additional benefit to the grid.

Merchant model 1: Grid Reliability Services. Deregulated power markets have grid reliability products, known as ancillary services. Any qualifying power generation or storage asset located within the market can sell capacity as an ancillary service provider via a daily or hourly auction process. Prices are set in a similar manner to energy in deregulated markets: The market operator procures enough capacity to meet a required demand level, beginning with the lowest price offer. The marginal (highest price) offer needed to meet demand sets prices for all resources selected. The most common form of ancillary service for battery storage is known as “frequency regulation,” whereby a capacity resource will respond to very short term (as little as every few seconds) changes in demand, supporting reliable operation of the bulk power system. Participation in frequency regulation typically requires only short duration discharges or reductions of power, making it an attractive product for batteries. One of the most supportive competitive markets for battery storage is PJM (Pennsylvania-Jersey-Maryland Interconnection), which is the largest deregulated US power market, covering much of the mid-Atlantic. PJM offers a premium regulation product for fast responding resources such as batteries, known as Dynamic Regulation (RegD). We estimate that a well-operated battery participating in regulation markets can operate at high (nearly 100%) utilization rates throughout the year. Furthermore, pricing for regulation is fairly attractive, averaging ~$44/MW for all resource types in 2014. That said, regulation needs are limited, keeping the addressable market fairly small. For example, PJM requires only 725 MW of regulation on-peak, and 525 MW off-peak, and currently has ~300 MW of battery storage operating, all of which was constructed in the last several years. Due to the small market size, additional development of battery storage M will likely put downward pressure on regulation prices, in our view. We factor that into our analysis of ancillary service storage economics, and estimate such projects are currently economic at installed costs of ~$250/kWh or lower, excluding any available subsidies or incentives.

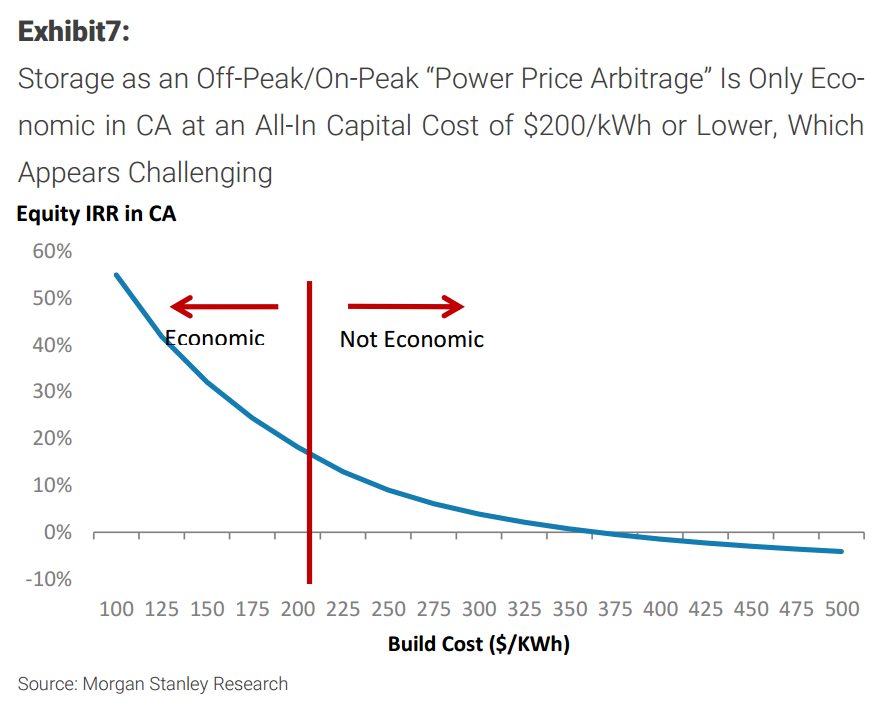

Merchant model 2: Price Arbitrage. Wholesale power prices are typi- Source: Morgan Stanley Research cally higher during peak demand daytime hours than during low demand hours, which typically occur at night. A second potential merchant business model would be to deploy a battery to arbitrage this price spread: buy low-cost power at night, and sell it during high priced periods during the day, effectively acting as a peaking power plant. In order to participate in a capacity resource that can sell energy, most power markets require at least 4-6 hours minimum duration — a much higher requirement than for ancillary services. Our analysis shows that average annual price spreads in US markets are well below levels needed to support price arbitrage battery economics. For example, in California the average price spread between the highest priced and lowest priced 4 hours averaged $20-25/MWh over the last several years. In addition to low spreads, most grid-scale batteries have an ~85% round-trip efficiency, meaning that ~15% of the energy purchased at night is lost and never sold back to the grid. Furthermore, while a price arbitrage battery can still participate in ancillary service markets as noted above, much of the capacity would not be available for sale during hours which the battery was either selling energy or recharging. We estimate that installed battery system costs would need to fall to below $200/kWh for a battery “peaker” to become economic in California. In PJM, we see limited application of such batteries even as prices fall due to stringent operating requirements under the proposed Capacity Performance rule, which can require long-duration energy production during extreme weather events.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.