Indicators suggest there is some risk of downturn (Box 2), with several potentially destabilising events possible (Table 2). Threats to stability from overheating in terms of output or inflation has lessened in recent years (Figure 12, Panel A). However, macrofinancial indicators underline the threat from the housing market, with house prices and related indicators (house indebtedness, bank size, Figure 12, Panel B) pointing to continued vulnerability. Any impact will most likely be through aggregate demand than financial instability. Although there are a number of factors likely to mitigate the systemic impact of these vulnerabilities, including large aggregate mortgage prepayment buffers and recently tightened macro-prudential measures, a fall in house prices and or demand could have significant macroeconomic implications. Specifically, the market may not ease gently but develop into a rout on prices and demand with significant macroeconomic implications. Externally, Australia, as always, is exposed to the vagaries of global commodity markets and this might include a renewed plunge in prices (or, positively, a strong resurgence). Australia’s iron ore production is among the lowest cost in the world and therefore comparatively insulated from such developments, however its coal sector is relatively more exposed as its production is distributed across the cost curve. Interaction of downside scenarios is likely to exacerbate the negative macroeconomic outcomes. For instance, a negative external shock could lift unemployment sharply which would result in significant fall in consumption and rising mortgage stress and falling house prices.

The economy is well positioned to handle shocks such as those described in Table 2. The speed and strength of the rebalancing processes in response to the end of the commodity boom auger well for the economy’s shock-absorbing capacity. In addition, Australia has more reserve capacity for monetary and fiscal stimulus than many other OECD economies (see discussion below).

Monetary and financial-market policy: coping with low interest rates

As in many other economies, monetary policy has been the principal tool for supporting aggregate demand in recent years. This partly reflects that fiscal policy has focused on curbing deficits following the large fiscal expansion during the global financial crisis and consequent rise in public debt (Figure 14). Monetary stimulus has been consistent with the RBA’s medium-term inflation target band of 2% to 3% (Figure 7), as inflation has been low, and interest rates are higher in Australia than in the United States or the euro area (Figure 14). Unless downside risks materialise, the current supportive stance of monetary policy remains appropriate at present, particularly in the absence of inflationary pressures. However, a side effect is a risk that accommodative policy may be increasingly distorting financial markets and, especially, house prices (which have risen to very high levels). Eventually, rates will need to be normalised, but the timing and pace will depend on developments in growth, employment, inflation, and the housing market.

Macro-prudential measures are helping contain housing-loan growth

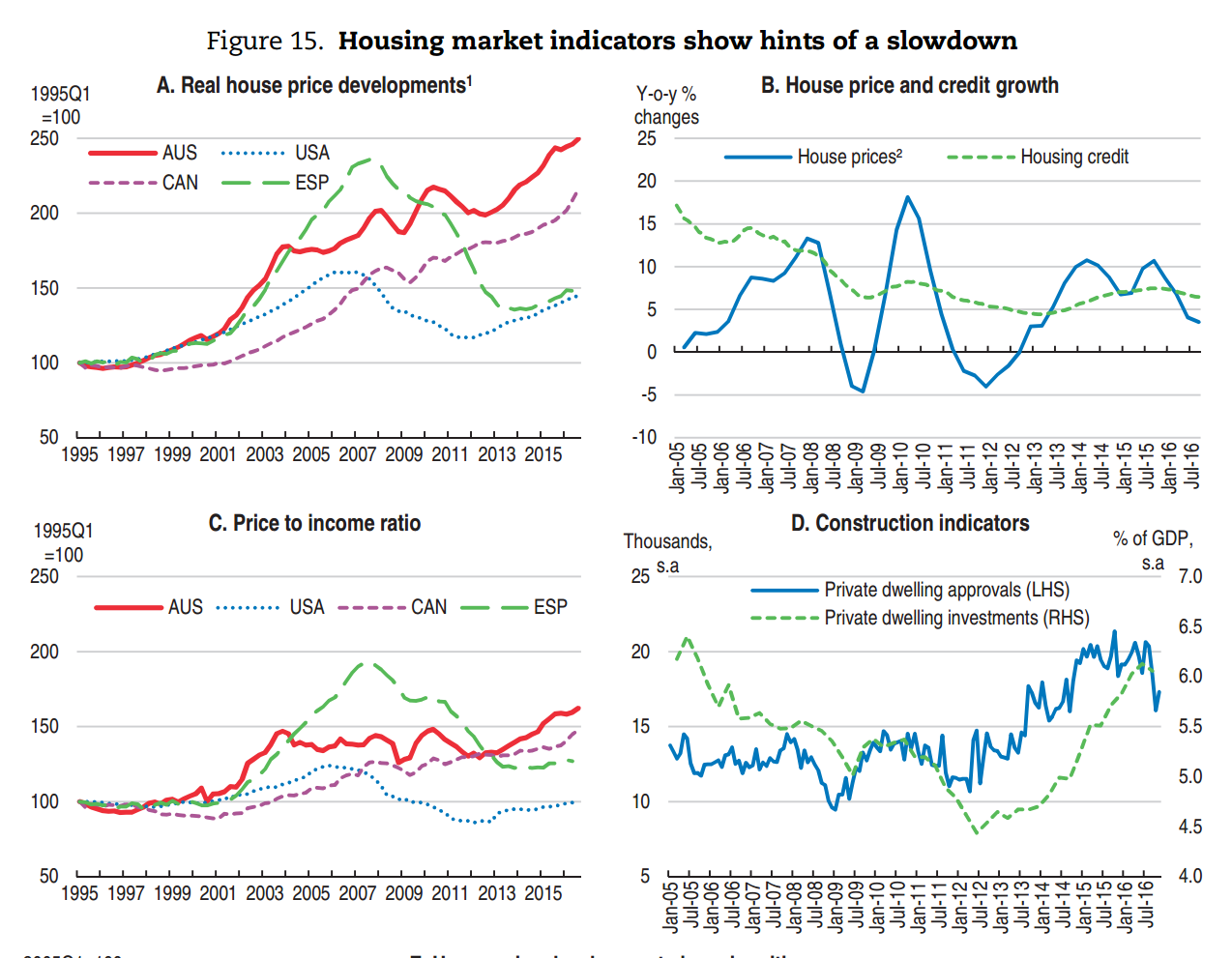

House prices and household debt have reached unprecedented highs (Figure 15), in part because policy-rate cuts have lowered debt servicing costs (most housing loans are set at variable interest rates). In real terms, house prices have increased by 250% since the mid-1990s. Furthermore, the ratio of house prices to incomes has undergone further increase in recent years, straining affordability, especially for first-time buyers in Sydney. Foreign demand for housing, while a contributing factor, does not appear to have had a substantial impact on price growth. There are signs that the housing market is cooling. Recent data indicate price growth has eased in most urban centres, reflecting in part a substantial supply response – dwelling approvals and investments have increased substantially in recent years (Figure 15). However, the significant increase in Australia’s house prices and price to income ratios remains. A continued rise of the market, fuelled by both investor and owner-occupier demand, may end in a significant downward correction that spreads to the rest of the economy.

All a bit silly. “Rebalancing” is only strong because of the housing bubble so if it pops there’ll be no economic resilience! Note Australian affordability is much worse than RBA propaganda says it is.

With the world’s leading credit rating agency warning this week that it will potentially downgrade all Australian banks — and the nation’s sovereign rating — unless the housing market’s crazy momentum cools fast, it’s beyond time for the Reserve Bank of Australia to reverse its 2016 mistakes.

If governor Philip Lowe ran money at a hedge fund, he would be forced to cut his losses and accept that the logic the RBA used to rationalise its May and August rate reductions was wrong (as we warned ad nauseam).

The two main reasons the RBA felt it could further debase borrowing costs were: first, because it thought the housing market was already cooling (erroneously claiming house prices fell in July); and, second, that its rate cuts would not reignite the boom that it launched in 2013. Both assumptions proved faulty.

Between January 1 and April 31, 2016, Australian capital city home values appreciated at a frisky 8.1 per cent annual pace (after removing the April jump in CoreLogic’s index when it upgraded its sales sample, which is the largest of any index provider). In the 10 months since April 2016 (or following the RBA’s May cut), price growth has accelerated to 10.4 per cent a year. Strike one.

Just as the Australian Prudential Regulation Authority’s 2015 constraints on credit creation were starting to mitigate the irrational exuberance, the RBA injected borrowers with another double dose of adrenalin.

And yet in September 2016, Lowe advised parliament that “the two interest rate cuts we have had this year do not seem to have stimulated a new round of house price increases”.

I mulled writing a similar piece yesterday. With the Fed now on the march, it might be done without too much damage via the currency. However, there are a bunch of reasons why more macroprudential would be better:

the domestic economy is very weak and although the next few quarters look a bit better that will get worse by year end as the dwelling construction boom begins its long fall;

a dollar spike would be damaging to suffering mining states;

the 2003 experience of targeting eastern house prices suggests a rerun of two hikes would result in serious price falls in Sydney and Melbourne. Back then we had the mining boom tailwind to bail it out, today recession would be a very high risk.

A better approach for the bubble managers is to drop the macroprudential speed limit to 5%. That would crush price growth and prevent a resurgence of it while low rates would prevent a rout.

That said, APRA still appears to be asleep at the wheel and if it is not going to tighten then Chris is right that the RBA should.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.