From Domain:

Philip Lowe has some high-powered backing if he leaves interest rates on hold Tuesday as widely expected.

Days after the Reserve Bank of Australia governor signalled that rate cuts weren’t in the national interest amid record household debt, the securities regulator said it was looking at mortgage lending standards across the banking sector. The Organisation for Economic Co-operation & Development last week highlighted risks posed by Australian property and private debt.

Sydney house prices have soared 73 per cent in the past five years, ranking it second only to Hong Kong as the world’s least affordable housing market, while Melbourne prices shot up 52 per cent in response to the RBA’s multi-year easing cycle. The central bank had sought to steer economic growth away from mining investment and toward Australia’s traditional services industries led by exports of tourism and education.

…In Sydney and Melbourne, a housing construction boom teamed with state infrastructure investment and population gains have led to a lopsided national economy. Consultancy SGS Economics & Planning estimates the two cities account for more than two-thirds of the nation’s economic growth. Meanwhile, in the mining hub of Western Australia, the economy is moribund.

That means the RBA is currently setting one policy for a range of disparate economies. If the central bank could vary its rate by region, SGS reckons Sydney would be on 3.75 per cent, Melbourne on 2.25 per cent and Western Australia capital Perth on 0.5 per cent.

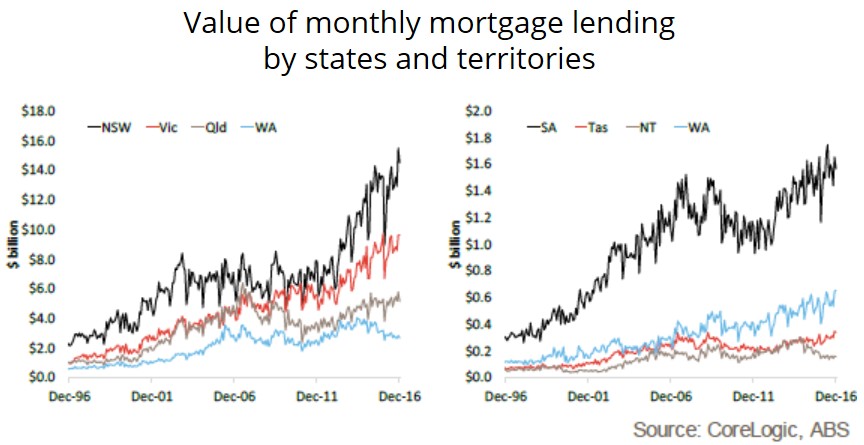

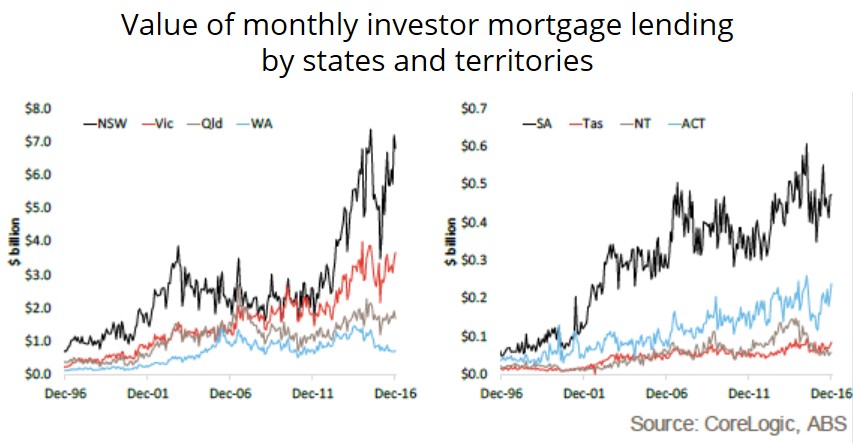

This is easily done. Here’s how. Sydney and Melbourne are soaking way more than their proportional share of investor mortgage credit, charts from CoreLogic:

APRA simply pulls back its macroprudential investor mortgage speed limit to 5% system growth. Year on year growth is only at 4.2% but a number of large institutions are running at 10% over the past six months. All will have to hike investors mortgage rates and, because the lending is so concentrated in Sydney and Melbourne, it will implicitly be geographically targeted.

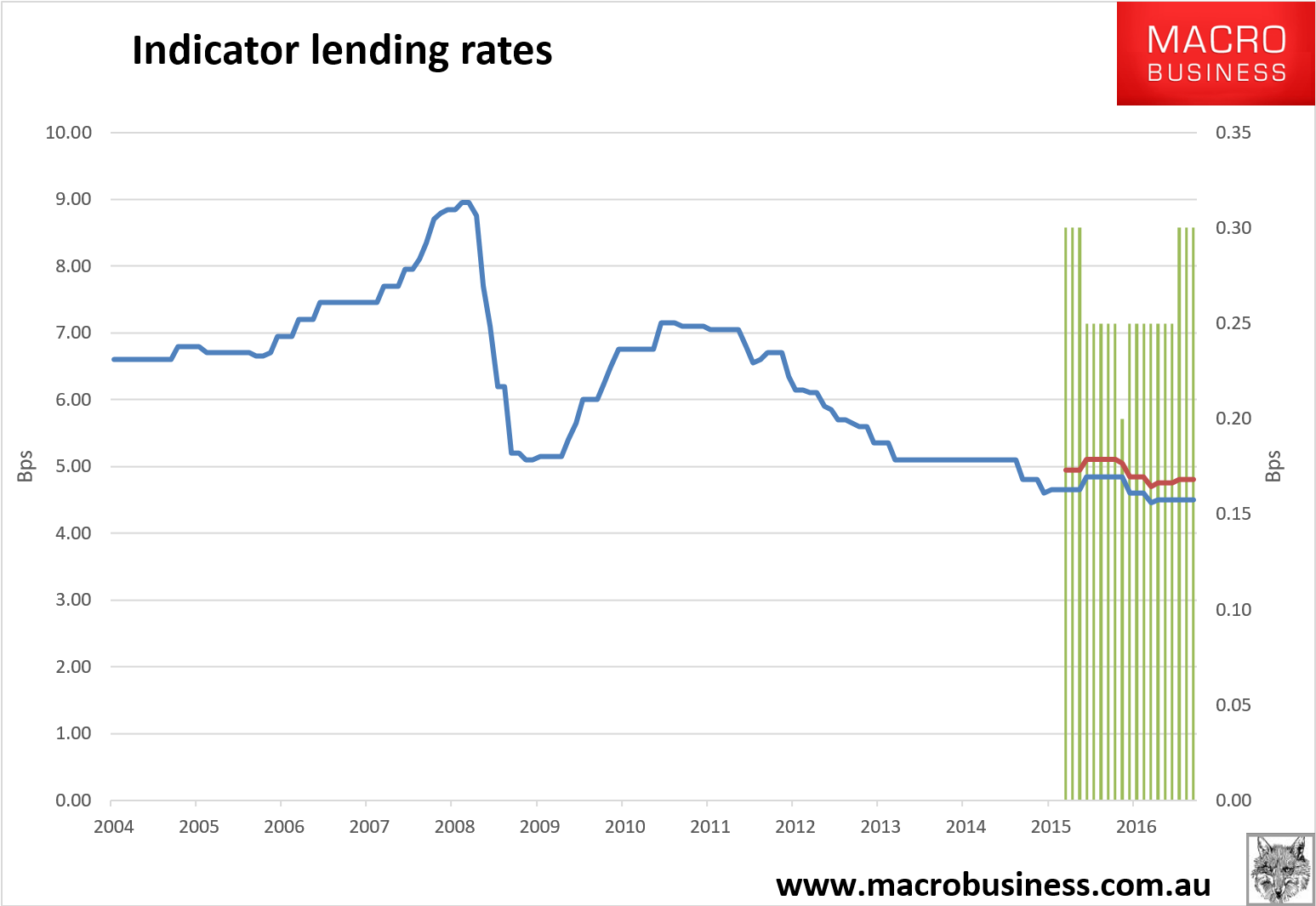

This has already lifted investor mortgage rates by 50bps and increased the spread to owner occupiers by 10bps:

Further macroprudential tightening will widen the spread much further. You just keep tightening until you reach the level you want.

Yes, there’ll be some dodgy loan switching but that can be resolved with better reporting and the experience of the first round of tightening suggests strongly that there’ll still be a big reaction anyway.

Then you cut the cash rate and mortgage rates fall everywhere else.

The only thing preventing it is APRA uber-caution and the diffused responsibility between it and the RBA owing to a broken twin peaks regulatory structure.

Just get on the phone to one another or, if that tech is too scary, meet under the mushroom in Martin Place. You’re both based there!