US-China trade relations haven’t yet appeared at the top of President Trump’s agenda, but it is likely to be a matter of time before this happens. One of the most consistent themes in Donald Trump’s comments on public policy over the past thirty years has been his opposition to persistent US trade deficits which, in his view, somehow impoverish the United States and enrich its trading partners.

The most important overall question in thinking about the Trump administration’s approach to the US-China trade relationship is whether it will be ‘soft’ or ‘hard’. We define a ‘soft’ approach as one governed by WTO rules and which aims to achieve a renegotiation of the trading relationship in a more or less cooperative environment; and a ‘hard’ approach as one that doesn’t hesitate to seek a rebalancing of US-China trade outside a WTO framework.

We believe there is certainly a risk that the Trump administration’s approach will be ‘hard’, since Trump officials think China’s membership of the WTO weakens the US’ ability to take action against Beijing’s unfair trade practices because the WTO lacks a proper framework to deal with the subsidies that are provided by China’s SOEs.

The central question in thinking about China’s response to a more hostile US approach to trade is whether Beijing will respond ‘symmetrically’ or ‘asymmetrically’. A ‘symmetrical’ response in our view is one in which a trade-policy measure is countered by a trade-policy measure: a kind of tit-for-tat. An ‘asymmetrical’ response is one where China’s reaction to a US trade policy initiative might range across the whole spectrum of the US-China bilateral relationship, including both economic and non-economic measures.

A trade-specific or ‘symmetrical’ set of measures by Beijing might be the first line of response. China could retaliate by bringing cases to the WTO on its own, impose countervailing measures, let its SOEs and other government controlled entities snub American goods and services or remove perks granted to US multinationals in China. But China might also choose to retaliate asymmetrically. Such measures could be of economic nature, e.g. threatening to sell off US treasuries and responding via the exchange rate, but could also extend to non-economic issues.

A US-China trade dispute would be least disruptive to global ‘animal spirits’ if the conflict is characterized by a ‘soft’ Trump and a ‘symmetric’ China response, but it is easy to imagine that neither of these conditions might hold. For that reason, it is worth being cautious about the effects that such a conflict might have on risk appetite, and on expectations about growth in the largest and second largest economies and beyond. We don’t believe that the market is currently pricing any risk of a ‘hard’ vs ‘asymmetrical’ conflict.

Also Macquarie:

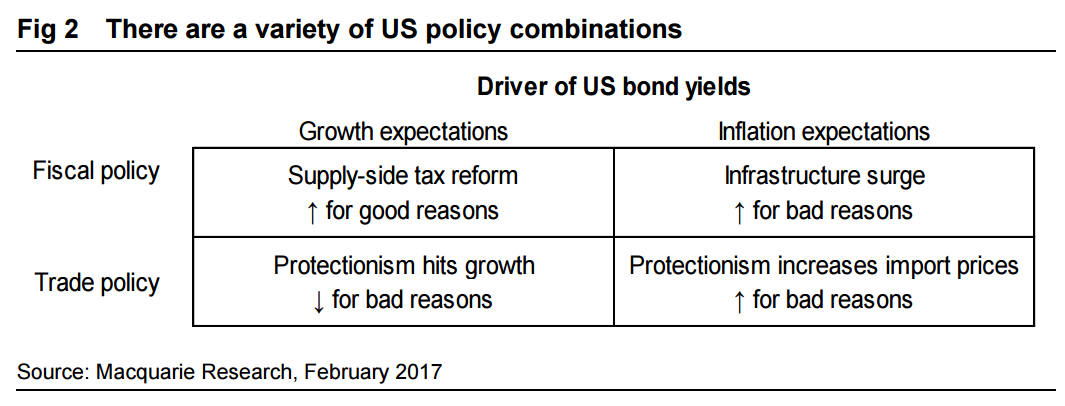

1) We believe the US bond market has started to price in protectionism: lower growth & higher inflation Fig.2 covers some of the possible policy shifts in the US. Please note that we believe protectionism would be bad for growth, but increase inflationary expectations.

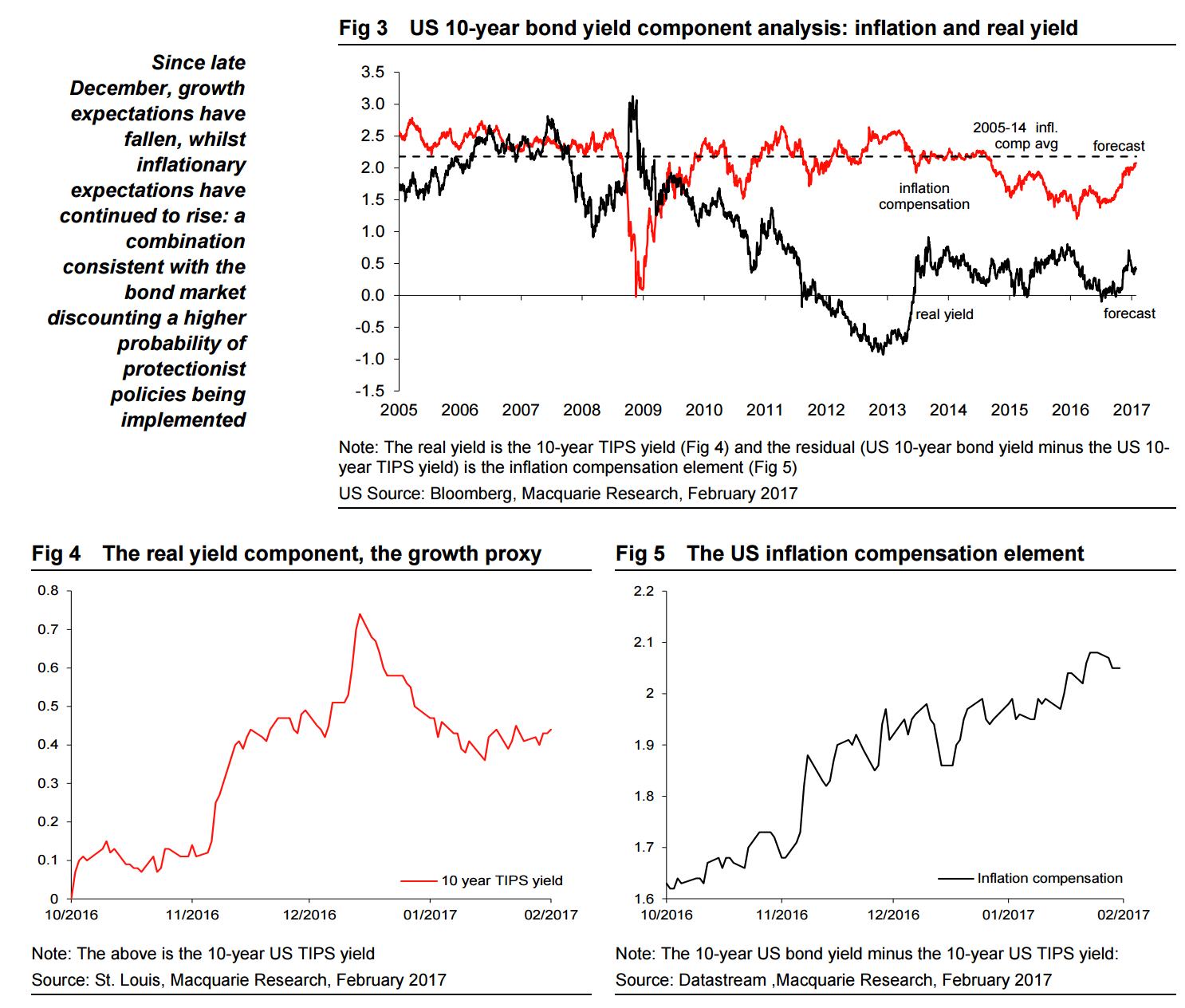

Fig 3, Fig 4 & Fig 5 break out nominal US 10-year bond yields into a real yield component, the growth proxy, and the US inflation compensation element. The 2016 global industrial production recovery, and the cyclical recovery in advanced economies drove up both elements from September 2016, Fig 3.

Following the US election on 8 November 2016, financial markets embraced the “Reflation trade” and as shown in Fig 4 and Fig 5, both the real yield, the growth proxy, and the inflation compensation element continued rising until late December. However since late December, growth expectations have fallen, whilst inflationary expectations have continued to rise: a combination consistent with the bond market discounting a higher probability of protectionist policies being implemented.

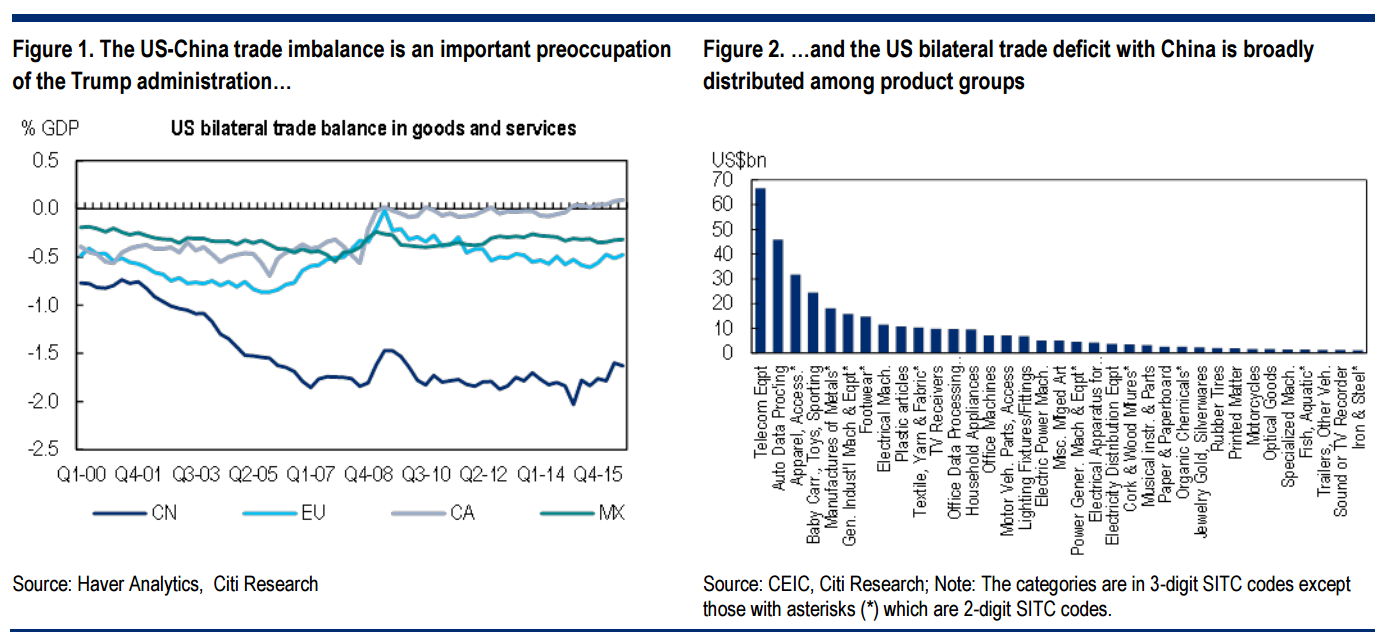

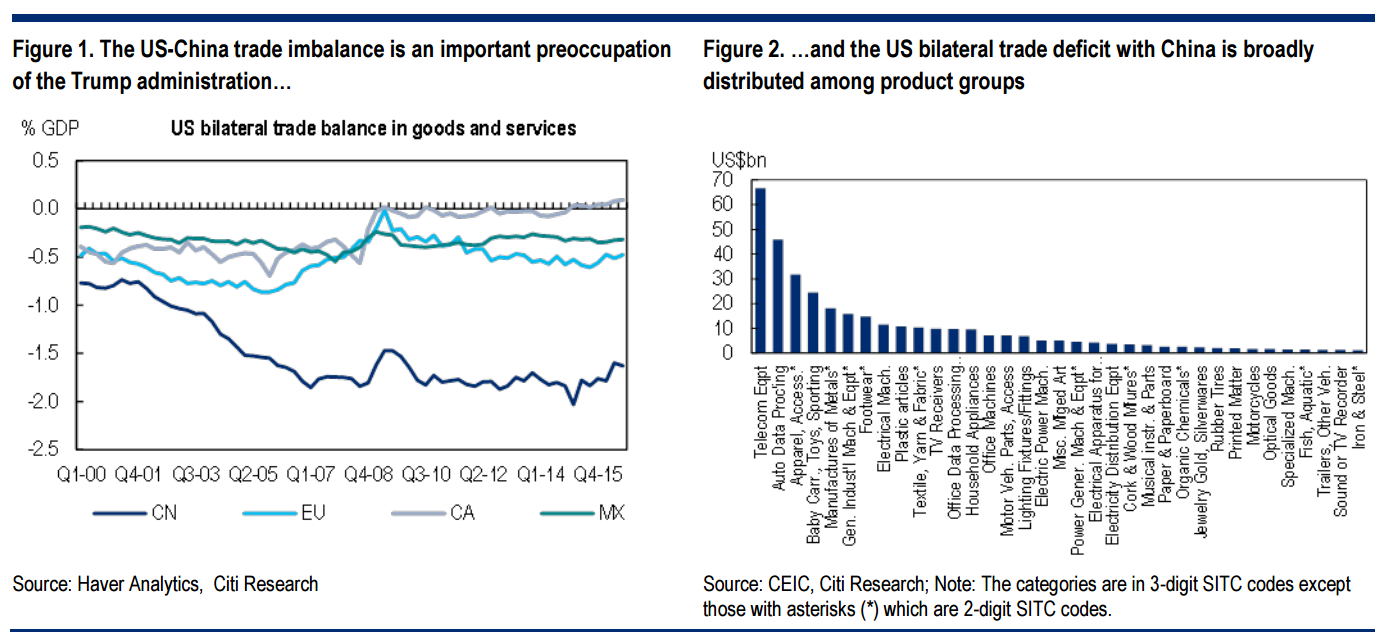

This is the context to the possible 45% tariff on Chinese imports and 35% tariff on Mexican imports. MNCs deployed successfully the ICT revolution over especially the 20 years up until 2008, and the Global Financial Crisis, resulting in a shift in global income shares to capital as explained in the 20 May 2016 Macq-ro insights: from labour to capital. There was a demand pull element into EM economies (as they embraced trade liberalisation) as well a MNC supply-push seeking lower labour costs. The following four charts perhaps suggest where President Trump’s attention will be. Economic vulnerability is one measure of negotiating weakness, Fig 6 and Fig 7. Mexico and China are highlighted in blue.

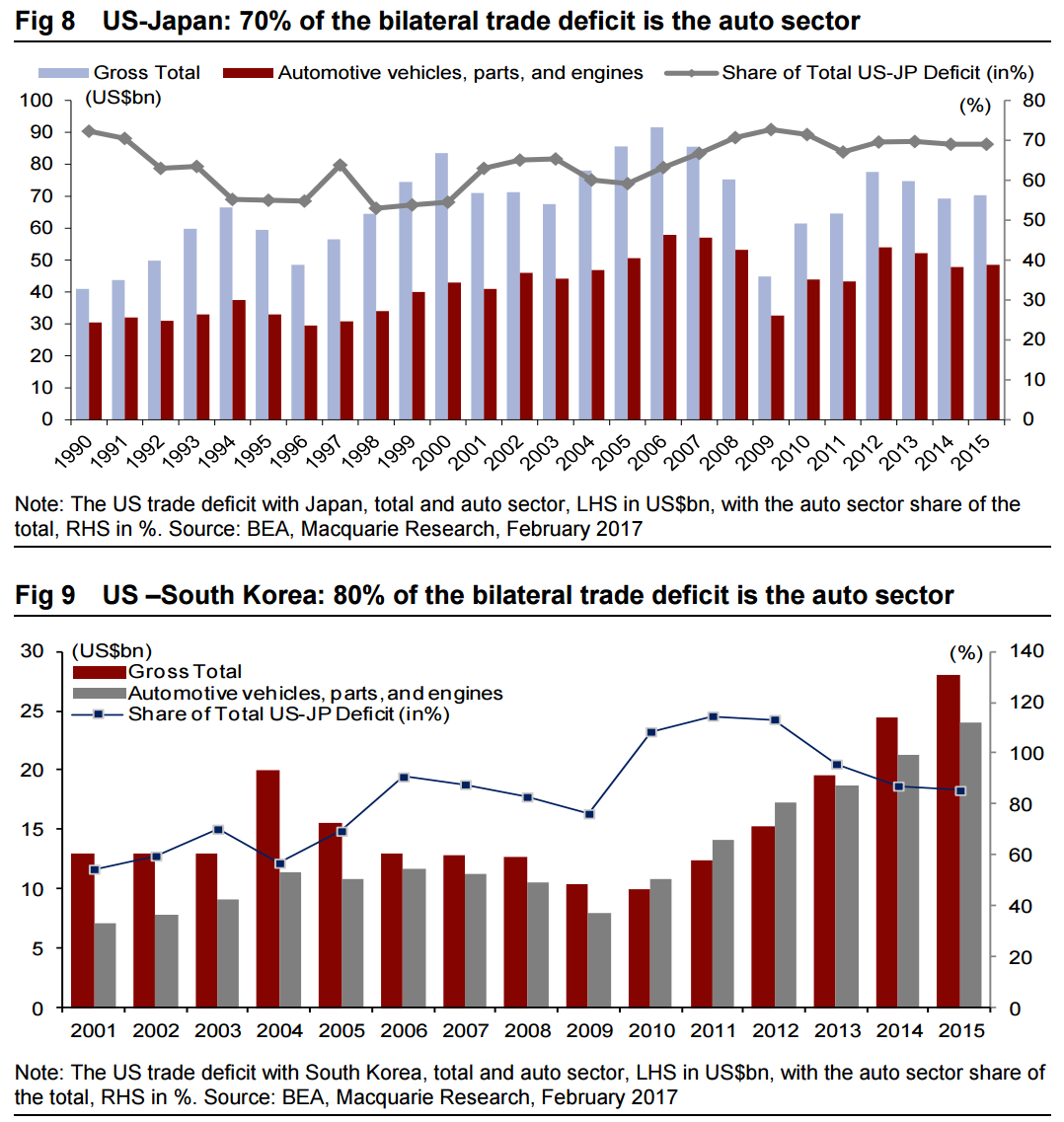

President Trump is probably aware of the ongoing US-Japan auto sector bilateral trade deficit, Fig 8. Ominously for Japan, the chart look very similar for South Korea (Fig.9) and the US-South Korea Free Trade agreement (KORUS, 2012) was under heavy attack from Candidate Trump and his advisors.

For what it is worth, my own mail from within the diplomatic corp is that Trump’s China hawk, Peter Navarro, has already been sidelined. Niall Ferguson has the right idea, I think:

Advertisement

The relationship between China and Donald Trump could deliver mutually beneficial trade outcomes experts say, defying fears that the billionaire US President’s “America first” platform will erupt in a protectionist spat and set back growth.

Niall Ferguson, the British historian, and Charles Dallara, an adviser to previous Republican presidents and the Trump transition team, both painted a more optimistic picture for US-China relations.

“His definition of winning is not getting the whole pie,” Dr Dallara, who is also vice-chairman of private equity firm Partners Group, said of President Trump.

“[China is] very, very attuned to the reality that perhaps they don’t need to respond to the first punch that President Trump may throw on the trade front.

“That if they are considered and if they are restrained and if they are patient, that solutions to the US-China trade problem can be found as they were found between the US and Japan during the 1980s,” he said, recalling that “both sides were able to walk away declaring victory”.

I agree that most of the renegotiation will be deals not dust-ups. Trump has already signaled “America First”. For those with brains, the obvious response is to come bearing great flattery and gifts. If so, you will be embraced by the Great Narcissist. Japan has shown the way here and, although it’s early, I suspect will walk away relatively unscathed in trade terms in return for greater defense spending and a commitment to invest in the US.

Advertisement

That’s what Trump wants more than anything, to save his people via growth and income and be adored, trade imbalances won’t matter if he gets it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.