While most signs point to Trump and a Republican-led Congress wanting to replace Yellen as chair, she does offer some advantages to the new administration. Yellen runs the Fed smoothly, is well known to and understood by markets, and is inclined to be cautious about raising rates until inflation becomes a significant risk. Nonetheless, at this point it appears likely that she will not be reappointed as chair.

The Chair’s role in FOMC decision making

The group dynamics that determine how the Fed makes policy decisions, and by extension how much influence the Fed chair has over policy, have shifted over time. Fed chairs have to strive for a strong consensus, but past chairs have pursued consensus in different ways. Greenspan was perceived as being more of a top-down leader. Even so, it took him a number of years to earn that power, and when he had, he used it relatively sparingly—reserving it for times when strong policy action was more necessary. Bernanke is viewed as having moved to a more bottom-up approach, as he promoted open discussion and deliberation of policy decisions by a wider array of individuals. Greater Fed transparency and more frequent Fed communication were also key aspects of this evolution. Yet when the chips were down and strong leadership was needed during the financial crisis, Bernanke clearly stepped up. He also championed moving the Fed into uncharted waters with a variety of special liquidity facilities and financial rescue packages, as well as balance sheet policy, the adoption of an inflation target, and strong forward guidance.

Yellen appears to have largely maintained the more deliberative structure that Bernanke endorsed, though at times she too has shown signs of adopting a more Greenspanian approach. Whomever the new Fed chair is, assuming Yellen is not reappointed, it will take some time for him or her to achieve the stature and respect that Bernanke and Yellen enjoyed (and continue to enjoy) in their committee leadership. The time Yellen had spent as Governor, President of the San Francisco Fed, and Vice Chair afforded her an opportunity to hit the ground running when she became the Chair, with an unusual degree of goodwill already established with her fellow FOMC members. Prior to his being named chairman, Bernanke earned significant respect during his tenure as governor especially via his speeches and the force of his arguments and persuasion at FOMC meetings.

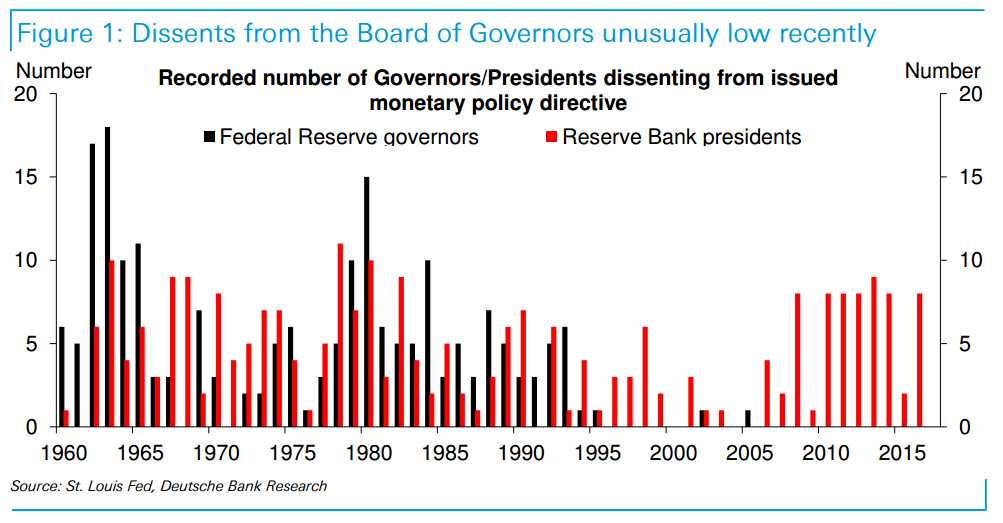

The consensus-based decision making process at the Fed should not be taken for granted, however. Indeed, there may be room for more contention on the Committee going forward. The FOMC has become less hawkish and more centrist in recent years. To be sure, the number of dissenting votes, especially among Fed governors, has been unusually low for the past decade (Figure 1). These numbers were much higher during the 1970s and 80s, when Fed leadership appointed by one Administration faced dissenting votes by new governors appointed under the next Administration. Paul Volcker, a centrist Democrat appointed by Carter, encountered dissents from a succession of supply-side Republicans appointed by Reagan. Looking ahead, less consensus and more dissents would seem likely if there is a shift away from the center at the top of the Fed leadership, especially if some of the centrists now in office remain until their terms run out (in most cases not until well into the 2020s).

Near-term market reaction

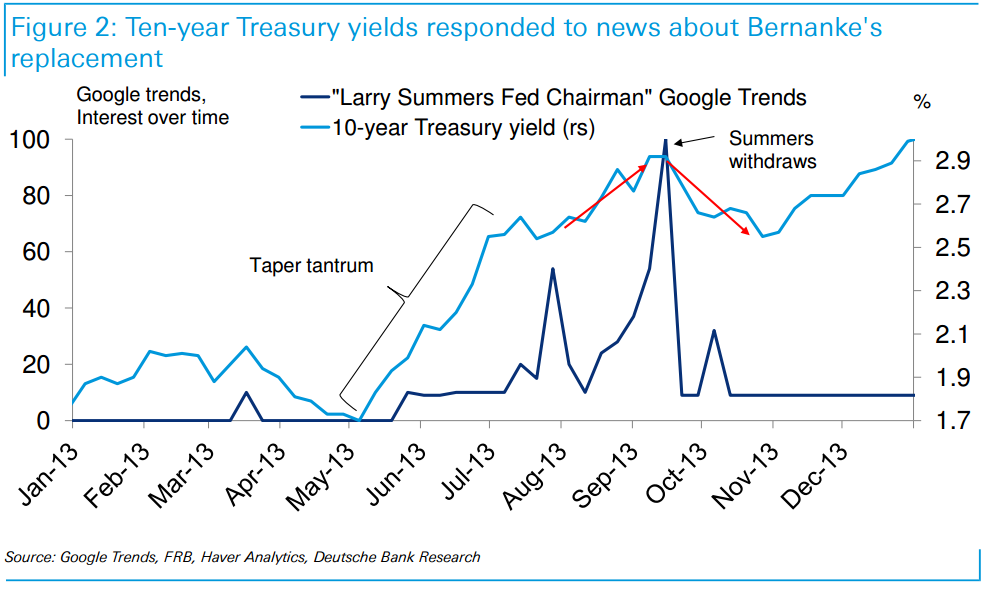

The importance of the Fed Chair goes well beyond the FOMC’s group dynamics. For example, markets will begin to reflect the potential for disparate monetary policy paths under different candidates. The market response to the decision about Bernanke’s replacement is a recent example of this. In 2013, Janet Yellen and Larry Summers were believed to be top candidates to replace Bernanke when his term expired in 2014. Although Yellen and Summers were similar candidates in many ways — both were well-known PhD economists with strong academic and policy backgrounds and orthodox views about monetary policy and the economy – Summers was perceived as being the more hawkish candidate. This perception was motivated at least in part by Summers’ more cautious views about the Fed’s unconventional balance sheet policies.

As the market believed that Summers’ odds of becoming Fed chair were on the rise, Treasury yields rose. The market narrative at the time was that a “Summers premium” was being built into Treasury yields to account for the risk of a more hawkish chair. This premium was then unwound when Summers’ odds diminished and he eventually withdrew his name from consideration in midSeptember (Figure 2). With the range of potential Yellen replacements seemingly wider than that for Bernanke, market pricing could be expected to shift more dramatically in response to news about her potential replacement, if it signals a sharp departure from current policy expectations.

A critical juncture for Fed credibility and independence

Beyond a near-term repricing of markets to prospects for a new Fed chair, Yellen’s replacement could have considerable long-term implications for the performance of the economy and markets. The next Fed chair will preside over an economy that is near full employment and that could be given a large dose of fiscal stimulus. This combination raises the risk that the Fed could fall behind the curve if it is not willing to sufficiently tighten policy. If the next Fed chair is more dovish, and the Fed does not sufficiently tighten policy to prevent the economy from overheating, inflation could rise and longterm inflation expectations could be at risk of becoming unanchored to the upside. In the extreme, the Fed’s hard-won credibility to target a low and stable inflation rate could be questioned. The risk to the Fed’s credibility and independence is potentially greater in the current environment where legislation is being considered that would put monetary policy decisions under greater review by Congress (i.e., audit the Fed). On the other hand, there are also prospects for a considerably more hawkish chair than Yellen, who could lead the Fed to follow a more “rules-based” policy. Because traditional monetary policy rules generally prescribe a fed funds rate well above current levels, such a chair would be more likely to act pre-emptively to ensure that the economy does not overheat. Short-term interest rates would be higher, the dollar stronger, and risks of higher inflation would diminish. As a result, the Fed’s inflation targeting credibility would be reinforced.

Who might replace Yellen?

At this point there is substantial uncertainty about who will replace Yellen. There has been little indication from the Trump administration about possible candidates, and the range of outcomes seems wider than in the past, given that Trump’s economic team has been filled by candidates that were previously relatively unknown in economic policy circles and who have not been associated with past administrations. It is also not straightforward to infer what type of candidate Trump may prefer from his past comments on the topic. While he has previously suggested that monetary policy is too loose, a more hawkish Fed chair would not seem to fit with his pro-growth priorities. Based on Trump’s past comments, the makeup of his economic advisors and appointments, and the political leanings of Congressional Republicans, it would seem that he may prefer a candidate that: (1) has significant experience in markets and/or business (i.e., a market practitioner rather than an academic economist), (2) does not have strong hawkish leanings that would work against Trump’s growth agenda, and (3) does not forcefully reject greater Congressional oversight of the Fed.

Given this uncertainty, we discuss three categories of candidates that Yellen’s replacement could be chosen from: known non-academics / market practitioners, known academics / PhD-trained economists, and relatively unknown candidates.

Known non-academics / market practitioners

The first group of potential candidates is known non-academics and market practitioners. Several recent Fed chairs, including Greenspan and Volcker, fall into this category.

For markets, the relevant points about a candidate in this category are the following. First, it is possible that his or her monetary policy views are not well-known and therefore the future path of monetary policy could be more uncertain. Markets should build in some risk premium to reflect this uncertainty. Second, given a background in financial markets, a Fed chair in this category could place greater focus on signals from financial market variables, the credit cycle, and spillovers from monetary policy across regions. Third, financial market practitioners may better understand how market participants will interpret and react to Fed communication and signals about the future path of monetary policy.

One potential candidate matching this description that has received some attention recently is Kevin Warsh. Warsh is an experienced private financial market practitioner with strong Republican credentials. He also served as a member of the Board of Governors during 2006-2011, a period when he gained useful experience assisting then Chairman Bernanke with financial crisis management, especially via his ties to the markets. Warsh has recently been openly critical of the decision making process at the Fed, saying that they lack a well-defined strategy, overreact to recent data points, and should focus more on the financial or credit cycle. His comments about whether the current policy stance is appropriate have been more cautious. In a recent panel at the Hoover Institution, Warsh noted that he does not see the difference between recent readings of 1.7% core PCE inflation and the Fed’s target of 2% – a seemingly hawkish comment that the current inflation shortfall does not justify keeping monetary policy loose. 2 He was also critical about the Fed’s balance sheet policies, because, in his view, the Fed’s strategy changed over time and that it risks entering into fiscal policy, not necessarily because of financial stability concerns or that the large balance sheet was providing an inappropriate amount of accommodation. These comments are slightly hawkish, but they leave room for interpretation about the implications for how monetary policy is set.

Another potential candidate in this category is current Fed Governor Jerome Powell. He is viewed as having conventional/centrist views about the economy and markets with slightly hawkish leanings. He has emphasized that the diversity of views within the Fed is important and supports the increase in the Fed’s transparency and communication that has occurred. 3 But he also supported some revisions to how the Fed communicates. In a speech last November he stated, “…communications should do more to emphasize the uncertainty that surrounds all economic forecasts, should downplay short-term tactical questions such as the timing of the next rate increase, and should focus the public’s attention instead on the considerations that go into making policy across the range of plausible paths for the economy.”

Both Warsh and Powell have recent experience in senior roles at the Fed. As such, they understand well the Committee’s decision making dynamics. Other former Fed governors with Republican or conservative leanings include Randall Kroszner and Lawrence Lindsey. If one expands the list to include recently former Reserve bank presidents, a name like Richard Fisher could be added.

Known academics / PhD-trained economists

Consistent with the past two Fed chairs, Yellen’s replacement could be a well-known PhD-trained economist. Such a candidate would likely bring well established views about the economy and monetary policy’s role. For markets, while such a candidate could move policy in a dramatically different direction, these characteristics should also reduce uncertainty about the future path of monetary policy.

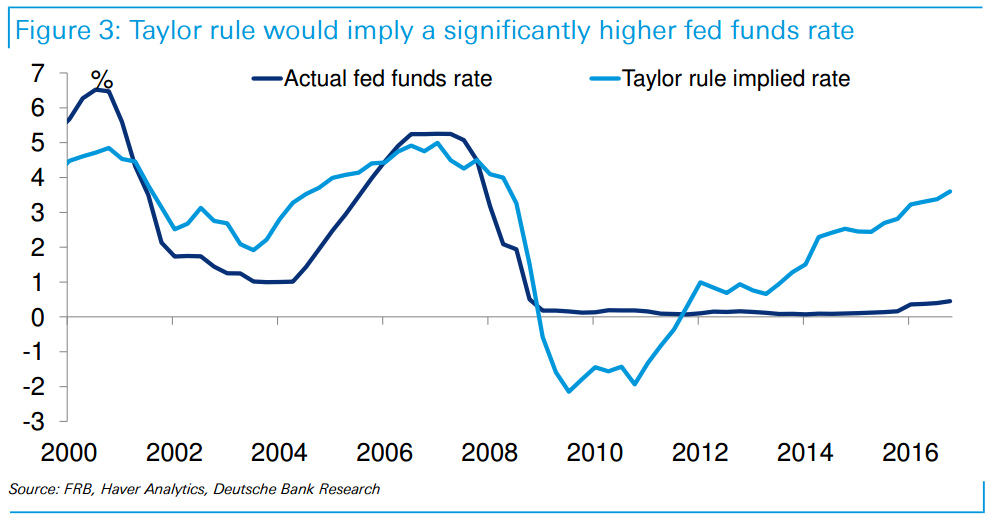

A candidate frequently named in this category is John Taylor. Out of the possible candidates, Taylor’s views about monetary policy are likely to be the best understood. He has argued consistently in recent years that Fed policy is too dovish relative to his Taylor rule. If Taylor was perceived as being a likely candidate the market would price a more hawkish Fed outlook, especially in terms of interest rate hikes. Indeed, the original version of his rule would prescribe a fed funds rate currently above 3% (Figure 3). Politically, Taylor would fit with Republican views for a more rules-based Fed, but his policy leanings — more aggressive rate increases and the stronger dollar that would result — would work against Trump’s pro-growth agenda the Republican side of the political spectrum. However, their ties to past “establishment” administrations may hurt their chances in the current discussion. John Cochrane, a professor from the University of Chicago with conservative leanings, could be another potential candidate. He has written extensively about financial economics and asset pricing, as well as about monetary policy. Some of his recent research has delved into more unorthodox topics, such as whether Fed policy rates and inflation could be positively related, i.e., that low policy rates may lead to low inflation and vice versa. These are just several examples of potential candidates that come from well-known academic backgrounds. Our list is hardly exhaustive; other candidates are certainly possible.

Relatively unknown candidates

The final potential candidate is someone that is relatively unknown. This would not be unprecedented. In 1978, G William Miller, who had been serving as CEO of Textron Corporation, as well as on the Boston Fed’s Board of Directors, was a relative unknown to markets when he was appointed as Fed Chairman. In his short tenure, Miller presided over a surging inflation rate in the late 1970s, and it soon became evident that he was in over his head when it came to guiding monetary policy. Miller agreed to move over to become Secretary of Treasury, and Volcker was then named to lead the Fed and tasked with taming inflation.

The next chair will not face the same sort of crisis situation that Miller did when he took office, at least not right off the bat. The economy is essentially at full employment and inflation is showing signs of nearing its desired level. The Fed enjoys substantial credibility and inflation expectations are reasonably well anchored.

That said, a widely “unknown” candidate will face challenges. Such a candidate’s views about monetary policy will not be well understood initially, and markets will have to build in a risk premium reflecting this uncertainty. Markets will be sensitive to the possibility that a candidate meeting this description would be in tune with the Trump Administration’s pro-growth agenda. It is possible that such an orientation will be appropriate if animal spirits succeed in boosting the supply side of the economy via a surge in business investment and labor productivity growth. However, it is also possible that strong growth in aggregate demand will kindle a significant overshoot of inflation, putting the Fed well behind the curve and greatly enhancing the potential for discord on the FOMC.

In conclusion, it is safe to say that the likely change in Fed leadership ahead will make for a significant increase in uncertainty about the course of monetary policy and fascinating times ahead for Fed-watchers and investors alike.

Historical experience under different Fed chairs

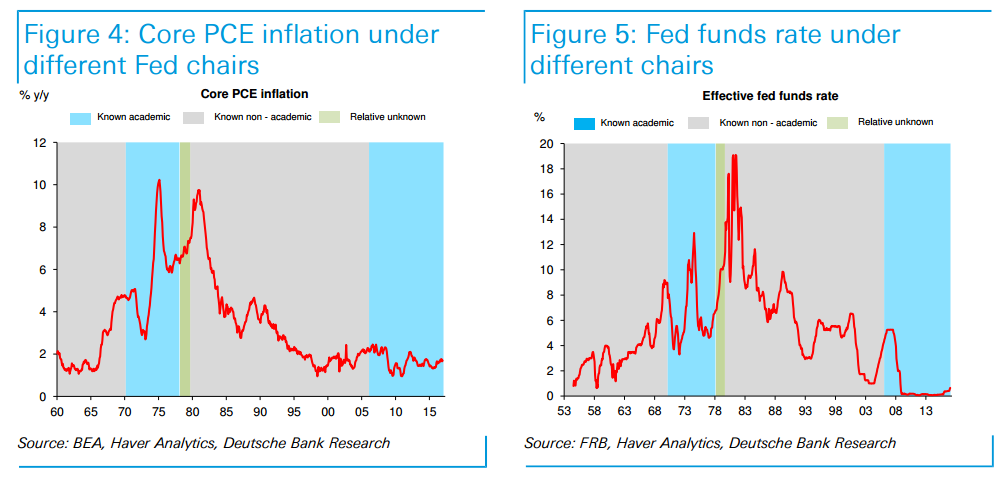

How have the different Fed chair types influenced economic performance in the past? It is difficult to reach any firm conclusions given that the number of Fed chairs is limited, and the economy’s performance has often been driven by events and trends outside of the Fed’s direct control, such as demographics.

However, there is an interesting observation to note about a variable more directly influenced by the Fed: inflation. The large pickup in inflation in the 1970s occurred under a chairman that was a known academic but without significant Fed experience – Arthur Burns. The rise in inflation continued under a previously unknown chair G. William Miller. It then took Volcker and Greenspan – two well-known but non-academic economists – to bring inflation under control and help usher in the two decade-long period of low macroeconomic volatility and solid economic performance that was the Great Moderation. This experience would conflict with a view that a more academically-oriented Fed chair would be more likely to tame inflation, while a more market-oriented chair would be more reluctant to tighten monetary policy aggressively.

Current vice chair, Stanley Fischer, is surely the outstanding favourite. He is more intuitively hawkish than Yellen (he was the first central banker to hike rates post-GFC in Israel) but is not dogmatic so would perhaps re-orient the Fed a little more towards tightening but not so much that it disrupted markets. Continuity recommends itself strongly in a recovering economy. .

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.