From Bubble-o-Phil today:

To this:

This year’s growth has been shredded but worry not, the RBA always has a future boom at hand and despite a poor H1 this year, H2 is going to rocket to deliver an unchanged result of 3%. How?

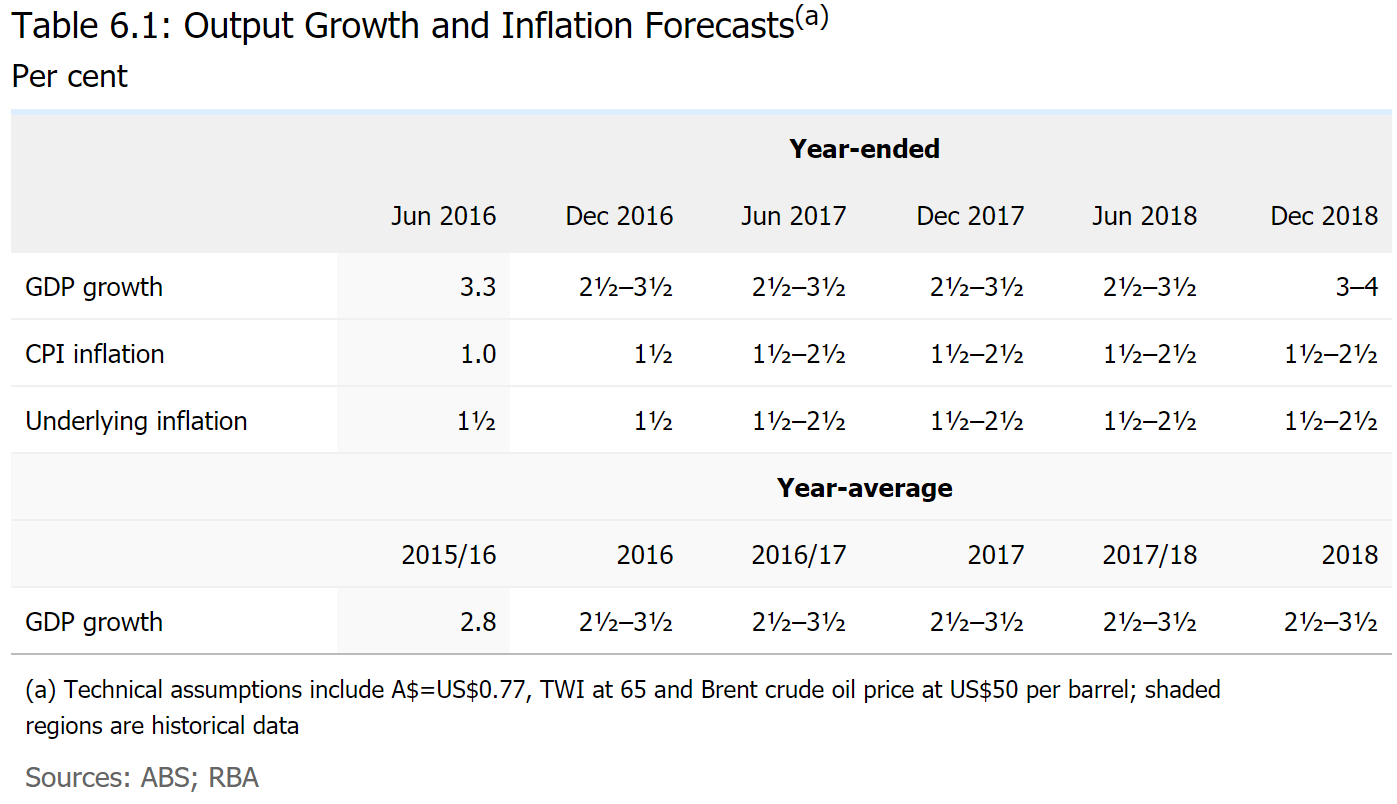

Overall, the forecasts for year-ended GDP growth are lower over the next three quarters than those presented in the November Statement, almost entirely due to the base effect of the weak September quarter (Table 6.1). The profile for consumption growth has been revised a little lower over the forecast period reflecting a view that consumption growth is unlikely to run materially ahead of household income growth over this period. This implies that the saving ratio will be relatively stable, rather than continuing to decline, as previously assumed. The effect of the adjustment of the consumption growth profile on aggregate GDP growth is partly mitigated by an offsetting, and related, downward adjustment to the forecasts for import growth.

Overall, year-ended GDP growth is forecast to pick up as the drag from mining investment and effects from the earlier fall in the terms of trade dissipate. GDP growth is forecast to increase to 2½–3½ per cent in late 2017, and to be above potential for most of the forecast period.

Some of the factors that led to the slowing of non-mining activity over the year to September were temporary. For instance, the fall in residential construction activity in the September quarter reflected bad weather. The large pipeline of work yet to be done, particularly in apartment building, is still expected to support further growth in dwelling investment over 2017. Public demand also declined in the September quarter, but this series is volatile. Public demand is expected to grow solidly over the forecast period, consistent with state and federal government budgets, which together imply ongoing growth in public investment.

Household consumption growth lost some momentum in mid 2016. This slowdown brings year-ended growth more into line with the subdued growth in household disposable income and suggests that households have become less willing to reduce their rate of saving to support consumption, despite low RBA interest rates and increases in household wealth. Given the stronger tone of more recent indicators, consumption growth is expected to be a little stronger than in mid 2016 over the forecast period.

Non-mining business investment has been weak for some time, despite the support provided by low interest rates and the earlier depreciation of the exchange rate. The outlook for non-mining business investment is relatively subdued in the near term, consistent with the Australian Bureau of Statistics (ABS) capital expenditure survey of firms’ investment intentions and the recent downturn in non-residential building work yet to be done. Non-mining business investment is still expected to pick up later in the forecast period and there are a number of positive indicators that support this projection. Non-residential building approvals increased over 2016 and non-mining business investment has been growing in New South Wales and Victoria, which have been less affected by the end of the mining investment boom. Moreover, survey measures of capacity utilisation have been increasing over the past couple of years and are currently above their long-term averages.

Much of the weakness in mining activity in the September quarter was the result of temporary factors and mining activity is expected to contribute to growth over the forecast period. The fall in resource exports in the September quarter was partly the result of temporary disruptions to coking coal production. In the medium term, the assessment of the production capacity of the resource sector is little changed and therefore the forecasts for the volume of exports are also little changed. Liquefied natural gas (LNG) exports are expected to continue growing strongly for some time. More broadly, exports of Australian goods and services in aggregate are forecast to continue growing at a solid pace.

Recent high prices for bulk commodities are not expected to lead to a material increase in production capacity, partly because prices are expected to decline over the forecast period. Mining investment is still expected to fall further over the forecast period, as large resource-related projects are completed and few new projects are expected to commence. However, the largest subtraction of mining investment (net of imports) from GDP growth has already occurred.

Lower GDP growth in mid 2016 is consistent with the loss in momentum in the labour market outcomes observed over 2016. Leading indicators such as job advertisements and job vacancies point to some pick-up in employment growth over the first half of 2017. Employment growth is then expected to remain broadly steady over the next couple of years, which is slightly lower than forecast at the time of the November Statement. This forecast takes into account the expectation that LNG production, which is less labour intensive than the investment phase of the mining boom, will make a contribution of around ½ percentage point to year-ended GDP growth over each of the next few years. The unemployment rate is expected to edge lower over the forecast period, suggesting only a modest reduction in the degree of spare capacity in the labour market from current levels. The participation rate, which is influenced by both structural and cyclical factors, is assumed to remain around its current level.

There has been a small downward revision to the forecasts for various measures of wage and household income growth over the next few quarters following the slightly weaker-thanexpected outcomes for wage growth in the September quarter. As a result, the pick-up in wage growth has been pushed out a little and is consistent with information from liaison that firms expect little change in wage growth over the next year. The forecast gradual recovery in wage growth from late 2017 assumes that some of the factors that have been weighing on wages will gradually dissipate. For example, the significant decline in wage growth in resource-rich states and mining-related industries is expected to fade as the economy rebalances towards other activities. Firms’ and employees’ near-term inflation expectations are not expected to fall any further. However, ongoing spare capacity in the labour market is expected to limit the recovery in wage growth.

Got to keep up those spirits.