So far results have been tilted to the positive with the average revision to FY17 consensus EPS c+1%. A clear trend has been upbeat/positive guidance for many companies. Share price reactions to the results have been marginally negative, despite a flurry of positive reactions early on.

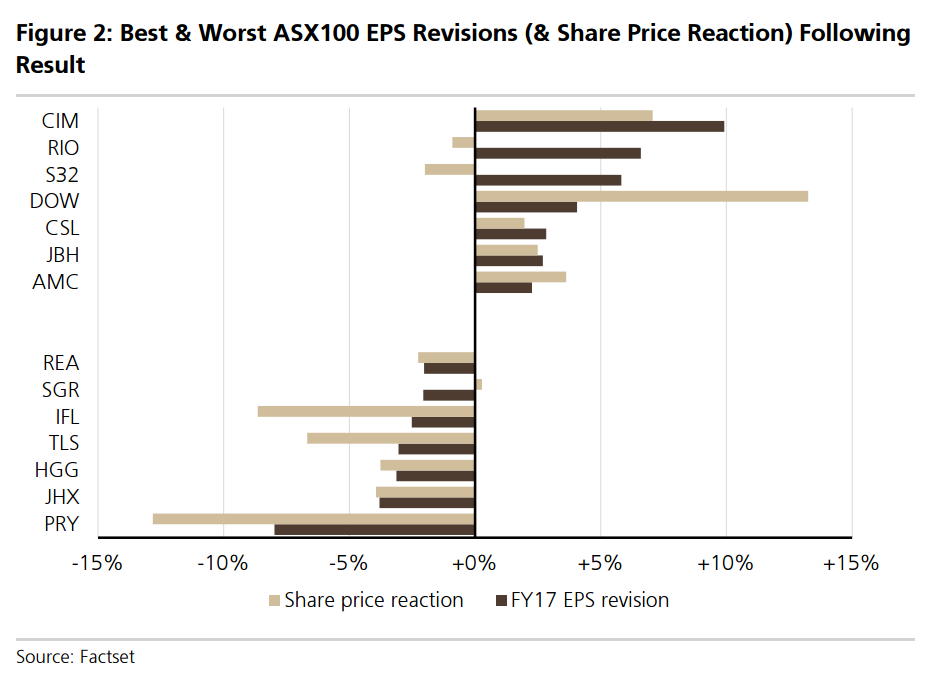

Positive & Negative Surprises

Stocks we judge to have surprised positively so far are AGL Energy, Amcor, Boral, CIMIC Group, Computershare, Downer EDI, JB Hi-Fi, Resmed and Transurban Group. In contrast we estimate there have been 7 noteworthy disappointments relative to consensus: Bendigo Bank, Domino’s Pizza Enterprises, Henderson Group, IOOF Holdings, James Hardie Industries, REA Group and Tabcorp Holdings.

Key Themes – More Stock Specific Than Macro

So far reporting season trends appear to be mostly stock-specific than thematic, apart from the obvious improvement in resource stock earnings. We have so far seen good and bad results in both globally/US orientated and as well as domestically focussed companies. Our portfolio is tilted somewhat to US/offshore earners but the domestic economy still clearly has pockets of strength.

Market Conclusions – No Profit Bonanza But Better Earnings Foundations

Headline market earnings growth is accelerating rapidly in FY17E to c19% (from -9% in FY16) having been upgraded substantially over the last few months, although this lift is very much mining-driven. The ex-resources EPS growth pick-up forecasts is much more modest but improving nonetheless.

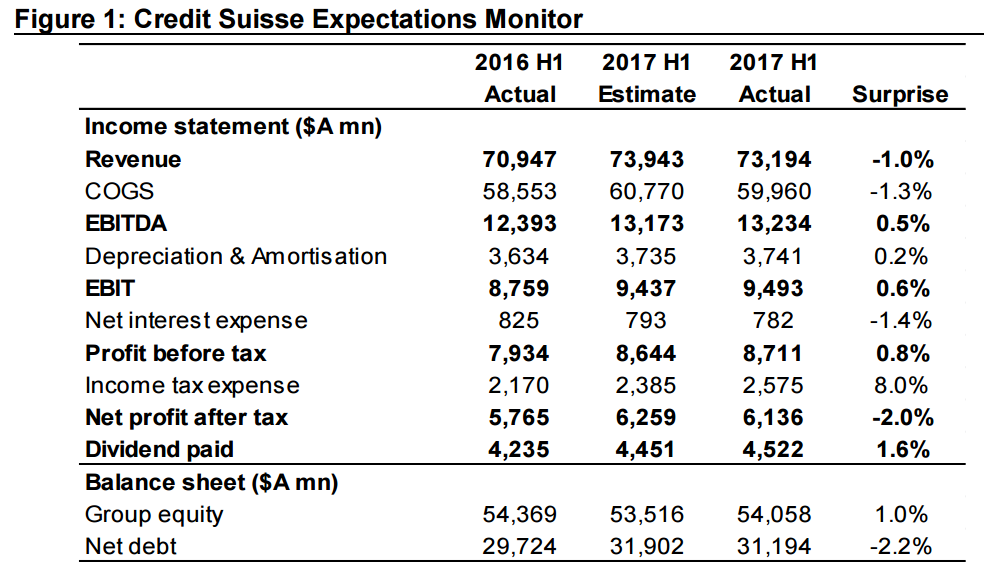

Credit Suisse also uses expectations but finds the opposite:

Revenue: As readers are all aware, the general economic environment has been challenging for a number of halves in a row now, and if anything it has modestly deteriorated further more recently, making organic revenue growth very hard to come by. Consistent with this, the companies that have reported so far have only delivered fairly modest +3.2% revenue growth, which has slightly disappointed relative to the prior Credit Suisse expectations of +4.2% for the same set of companies. This is directionally consistent with the general environment being tougher than expected, which has set the tone for the reminder of the aggregate P&L statement.

COGS: Over the past few years, our Credit Suisse Expectations Monitor has shown that as revenue growth has increasingly become harder to come by, companies have squeezed their costs to produce satisfactory profit growth, but that this source of profit growth has also now somewhat dried up. Consistent with cost-out having largely dried up, Credit Suisse was forecasting +3.8% COGS growth for the companies that have reported to date, i.e. very modestly less than the forecast revenue growth of +4.2%, indicating an expectation for slight aggregate margin expansion. Interestingly, as mentioned above, revenues have not grown as much as expected, nor have costs, but to date, costs have grown even less relative to revenue than expected, which has been the major source of bottom line profit growth during this reporting period. As recent past half years of limited cost out evidence have illustrated we question the sustainability of such cost out as a continued source of revenue growth going forward.

EBITDA and margins: Accordingly, operational earnings to date have grown more than revenue growth, i.e. by +6.8%, and have in fact positively surprised by +0.5% compared to prior Credit Suisse expectations. As a result, EBITDA margins have expanded by 27bp more than expectations on the pcp.

Net interest expense: In an environment of declining/low rates, it is not surprising that analysts were expecting a further -3.8% decline in net interest expense in FY17. However, to date, net interest expense has come in even further down at -5.2% on the pcp. As such lower-than-expected net interest expense has provided low-quality support for bottom-line earnings.

Income tax expense: Coming off an FY16 1H effective tax rate base of 27.3% (for the sample that have reported so far), Credit Suisse was forecasting little change in the effective tax rate to only 27.6% in FY17 1H. However, to date, the actual effective tax rate has come in well above expectations at 29.6% or broadly in line with the corporate tax rate of 30%.

Net profit after tax: The higher-than-expected tax paid has broadly offset the low quality bottom-line benefits of the (forecast) low D&A growth and the lower-thanexpected net interest expense, leaving NPAT growth of +6.4% marginally below operating earnings growth of +6.8%. As a result, NPAT has missed Credit Suisse expectations by around -2% reporting period to date, highlighting that in aggregate the reporting period has been modestly disappointing versus expectations.

Dividends: Despite Credit Suisse expectations for NPAT growth of +8.6% prior to reporting period (for the sample that have reported so far), we were not forecasting a commensurate increase in dividend paid growth, indicating we expected some aggregate dividend payout contraction from historically high payout levels. However, given softer than expected profit growth and modestly higher than expected dividend growth the expected contraction in dividend payouts has not materialised, accordingly, payouts remain historically elevated. Interestingly, post Trump winning the US electoral race in early November last year the dividend yield investment style has returned to relative favour (possibly as a result of Australian dividend yield still offering relative appeal (versus lower yields in other countries) compared to rising global bond yields), so companies delivering higher-than-expected dividends may be relatively more rewarded in the near-term.

Net debt and gearing: During the half, there has been some evidence of net equity retirement and modest debt raising, which has led to a slight increase in aggregate gearing. Given a persistent sub-trend macroeconomic environment over the past six months, we are not expecting there to be a significant change to the major themes identified in this report over the remainder of the reporting period.

You be the judge! I do not expect much. This year will see an ongoing economic plod with profit growth totally dominated by bulk commodity producers. Then next year the tail end of the bulk boomlet holds in earnings even as underlying profit conditions deteriorate with the economy.

There’s nothing here to alter my view that the developed market rebound is going bypass Australia.

Advertisement

That said, capital values do have upside risks. Miners can clearly rally further if spot prices hold up and that, in turn, will steepen the yield curve globally triggering buying banks, so in aggregate stocks could rise anyway.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.