The Australian interim reporting period has been the strongest since 2010. Analysts have raised their ASX 200 June 17 EPS forecast by more than 1%. This time last year, analysts cut their forecast by more than 2%. Expectations are now for ASX 200 growth of 18% for June 2017. Dividend forecasts have also increased and Aussie companies are set to achieve a new high watermark in dividend payments this year of more than A$72bn.

While it is still too early to conclude, there may be early signs that the Aussie earnings expansion is broadening out from commodities. There have been small upgrades for some of the classic cyclicals like the contractors, retailers and even Nine Entertainment! Meanwhile, outside the big misses for AMP and Suncorp, there were upgrades amongst the Financials. We anticipate a further broadening of the profits recovery from here.

Encouragingly, Aussie companies are resisting the temptation to spend. Although they have guided for stronger sales, they have also guided to weaker capex. This has not happened in over ten years. Further evidence of an earnings expansion and conservative capital allocation keeps us positive on Aussie stocks. We stick to our year-end target of 6000 for the ASX 200.

EPS upgrades

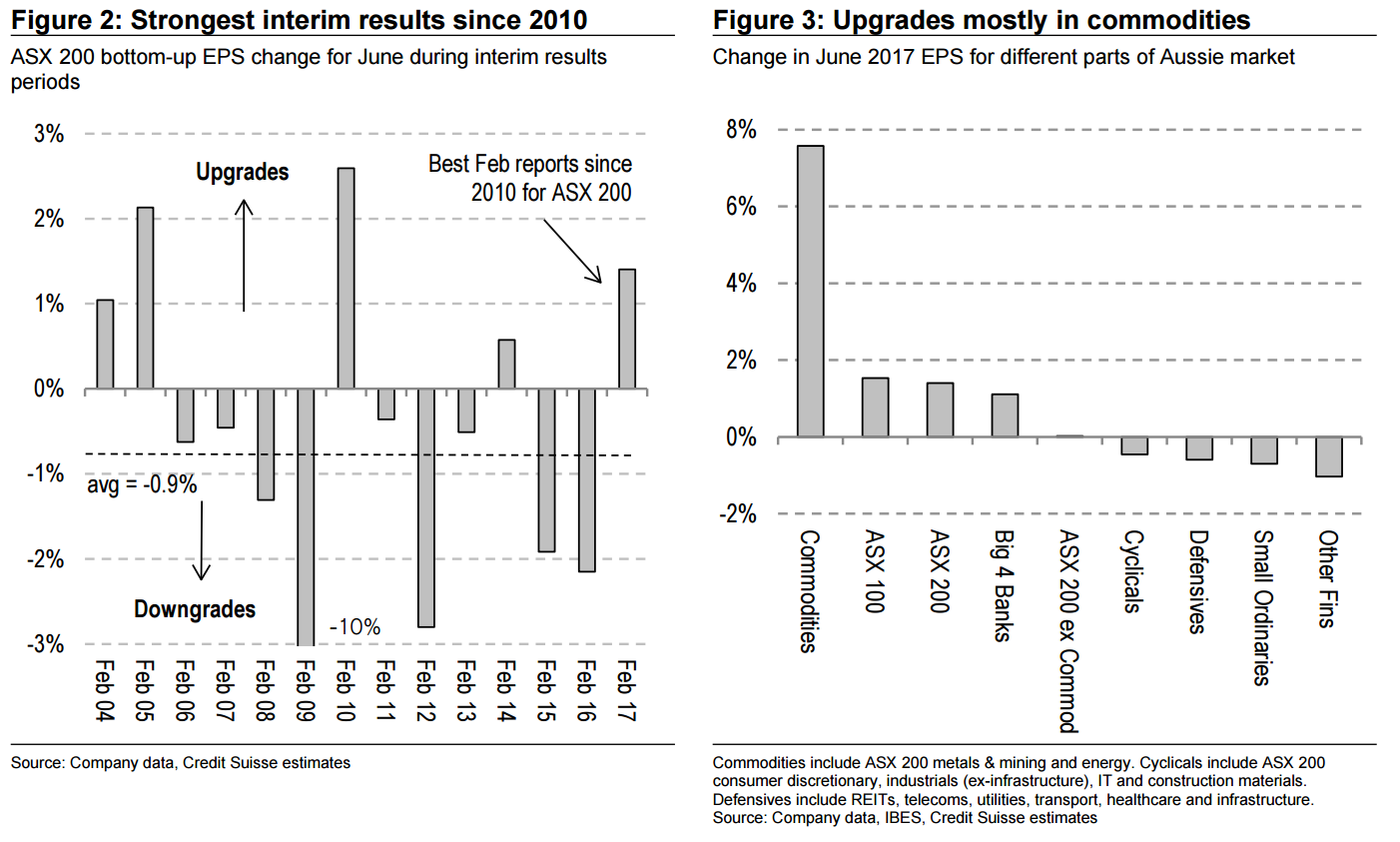

Australia is enjoying the strongest interim reporting period since 2010. Company results have led analysts to raise their EPS forecast for the ASX 200 by 1.4%. This time last year analysts had cut their forecast by 2.1%. On average analysts have downgraded by 0.9% during the February reporting period.

The upgrades have been focused in commodities. Here analysts have raised the equivalent of June year-end forecasts by more than 7%. There have also been upgrades in the big 4 banks (+1%). Of course this is important for our market as these four stocks make up 30% of the profits base. While it is not compelling as yet, we think there could be early signs of the earnings expansion broadening into other parts of the equity market.

Cyclical stocks (which include companies like Qantas, Amcor, Brambles, CIMIC and Aurizion) and Other Financials (non-banks, non-REITs) continue to suffer downgrades. However, even in these areas there is some good news. There were strong results from CIMIC, Downer, JB Hi-Fi and GUD. But these were more than offset by the weaker results from James Hardies, Dominos and Flight Centre, amongst others. Meanwhile, the 1% downgrade to “Other Financials” EPS would be a 0.6% upgrade if we exclude the big disappointers of AMP and Suncorp. So while it is too early to conclusively say the Aussie earnings expansion has broadened out from commodity companies, there could be very early signs of this happening. We expect further evidence of this during the full-year results in August.

Analysts remain skeptical beyond FY17

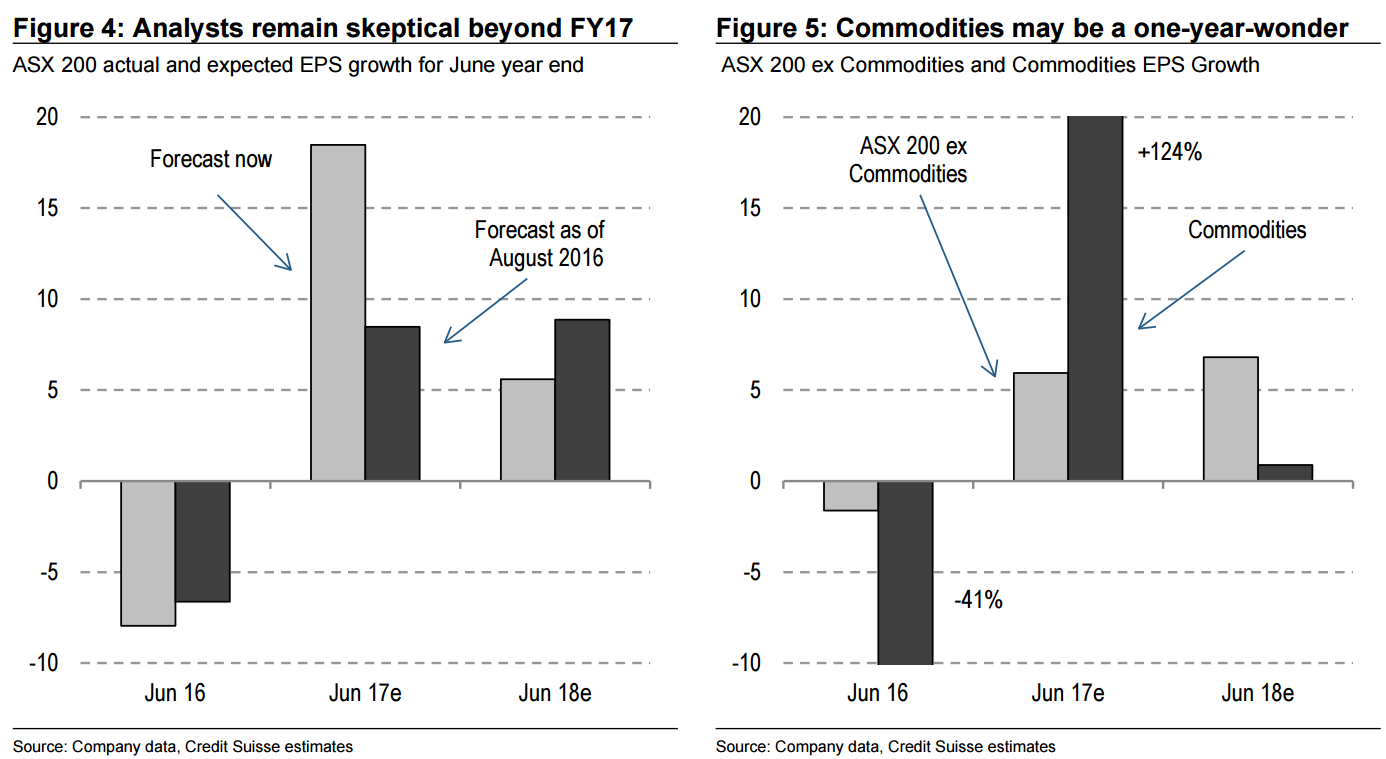

Upgrades to June 2017 EPS takes the ASX 200 earnings growth forecast up to 18%. Analysts were forecasting just 8% growth back in August. A double-digit increase in market EPS is consistent with the start of previous earnings expansions in Australia. But analysts remain skeptical that the strong EPS growth will carry into 2018. They are forecasting EPS growth to fall by two/thirds by June 2018. If we were to follow the path of previous earnings expansions then we should expect upgrades to the June 2018 forecasts as well.

Within the market the big driver of the EPS expansion has come from the commodity stocks. Analysts are forecasting metals & mining and energy company profits to double during the 12 months to June 2017, and then stall over the following 12 months to June 2018. Meanwhile, outside of commodities, analysts are anticipating a moderate acceleration in profits growth.

A new high watermark in dividends

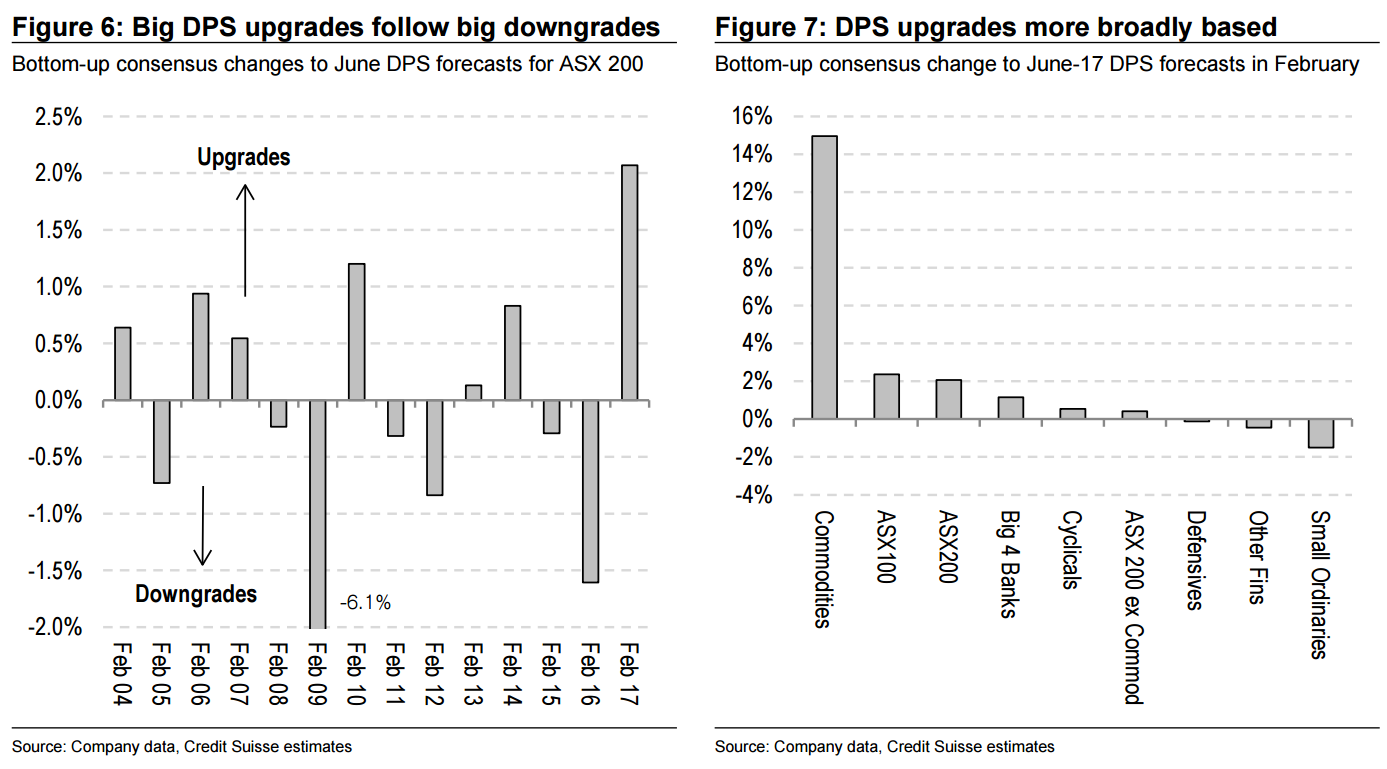

While analysts upgraded ASX 200 EPS by 1.4% during the February reporting period they raised their DPS forecasts by 2.1%. It was the best interim results period for dividends in more than 15 years. Of the course the big dividend surprise comes after the big miss this time last year. Remember that was when BHP made it clear its full-year dividend would be cut by an extraordinary A$6bn.

While there were clear DPS upgrades for the more cyclical components of the market, upgrades were lacking for the defensives (Staples, Telecoms, Infrastructure, Utilities and REITs). While defensive stocks were in demand this time last year, when dividends were being cut elsewhere, they are less sought after this year as more cyclical company distributions recover.

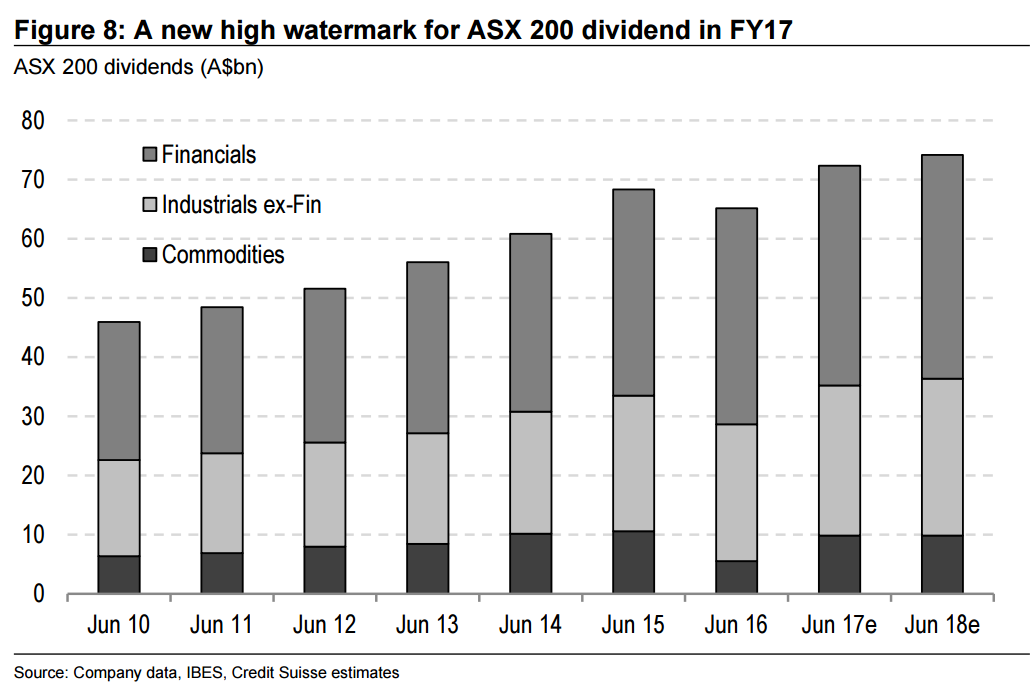

The upgrades now mean ASX 200 DPS growth should be around 10% for the 12 months to June 2017. Analysts expect a further 3% growth to June 2018. These forecasts stood at +3% and +6% in August last year. The forecast suggests a new high watermark in Aussie dividends will be achieved. The previous high watermark was A$68bn in June 2015. Now distributions are set to increase to A$72bn for June 2017. Australia Inc. continues to do its best to appease their income seeking investors.

Sales upgraded, capex downgraded

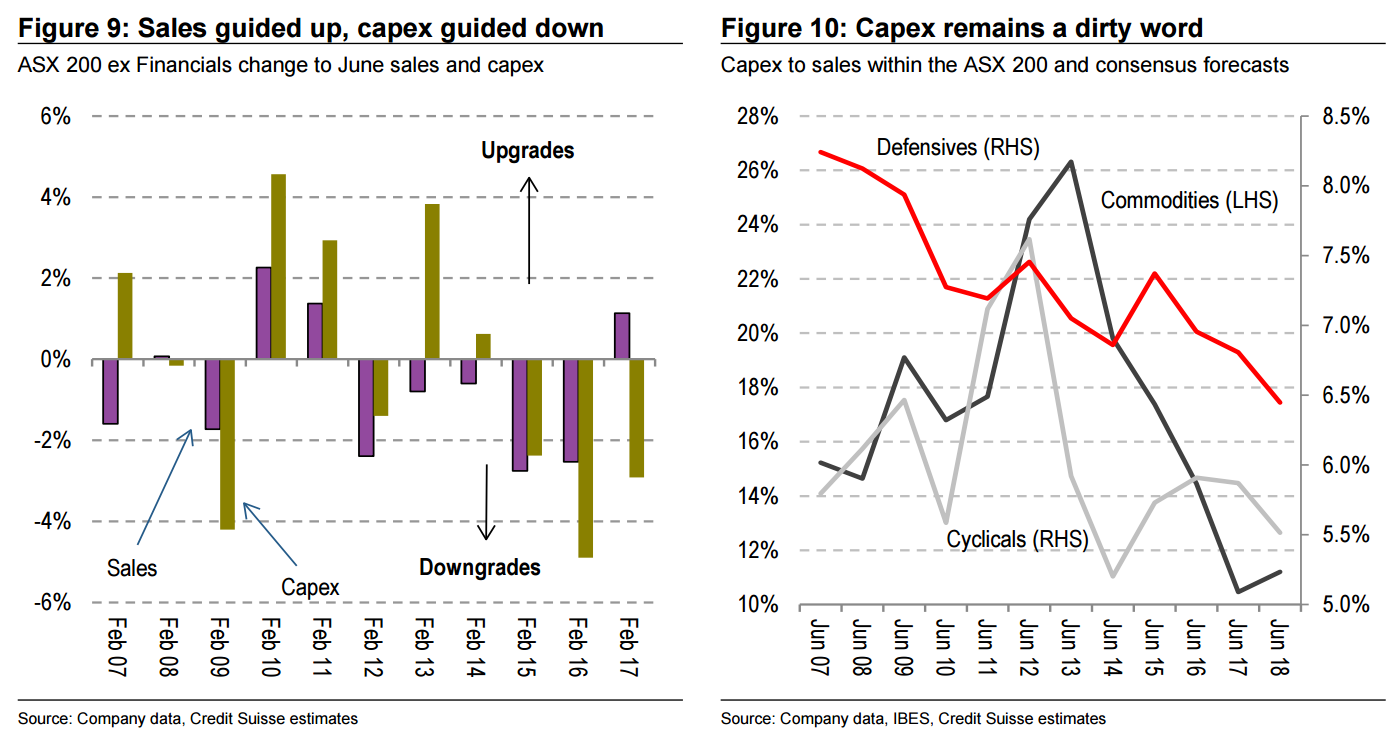

While EPS and DPS upgrades should keep investors positive on Aussie equities, we think the most bullish finding during the February reporting period was the guidance for sales and capex. In aggregate, Aussie companies guided to higher sales but lower capex. This is unusual (Figure 9). In fact it hasn’t happened in the past ten years. Australia Inc. has revealed a new found conservatism when it comes to capital allocation and are resisting the temptation to spend. Expectations are for capex to sales ratios to fall even further from here (Figure 10).

We saw this frugal approach on display in many of the results meetings. When Whitehaven was asked how it would use its now powerful balance sheet, the company replied that all forms of capital distribution were on the table. When investors asked Rio Tinto what their growth plan was, the company talked about its buyback. When Aurizion was asked if it intends to diversify away from coal, the new CEO quipped that he will focus on creating shareholder value and is not diversifying for diversifications sake. Crown made it even clearer that it will release capital by exiting Macau and Las Vegas and distribute more back to shareholders. Meanwhile, Nine Entertainment, despite signs of an improving ad market, reiterated its guidance for cost-cuts which had first been announced during a much bleaker period for the company. Although the profits backdrop has improved, Australia Inc. continues to target shareholder value. Aussie investors should be pleased.

Strategy outlook

Aussie companies have enjoyed their strongest interim reporting period since 2010. Analysts have upgraded their June EPS forecasts by more than 1% for the ASX 200. Usually, during this time of year, they downgrade their outlook by about 1%. While much of strength in profits has been in the commodity companies, we find fledgling signs of the earnings expansion broadening to other parts of the market. There have been small upgrades for some of the classic cyclicals like the contractors, retailers and even Nine Entertainment! Meanwhile, outside the big misses for AMP and Suncorp, there were upgrades amongst the Financials. We anticipate a further broadening of the profits recovery from here.

So far Australia Inc. is resisting the temptation to spend. They have rather focused on increasing distributions. For the first time in over a decade Aussie companies guided to higher sales but lower capex. Further evidence of an earnings expansion and conservative capital allocation keeps us positive on Aussie stocks. We stick to our year-end target of 6000 for the ASX 200.

I only wish that I could agree. As coal and iron ore deflate so too will the earnings lift, long before it leads to any new investment. Meanwhile the dwelling construction downdraft and car industry collapse will weigh as well. These earnings are an unlooked for boon from a one-off Chinese policy error. They do not herald a change for an economy with a broken structure. Business clearly agrees.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.