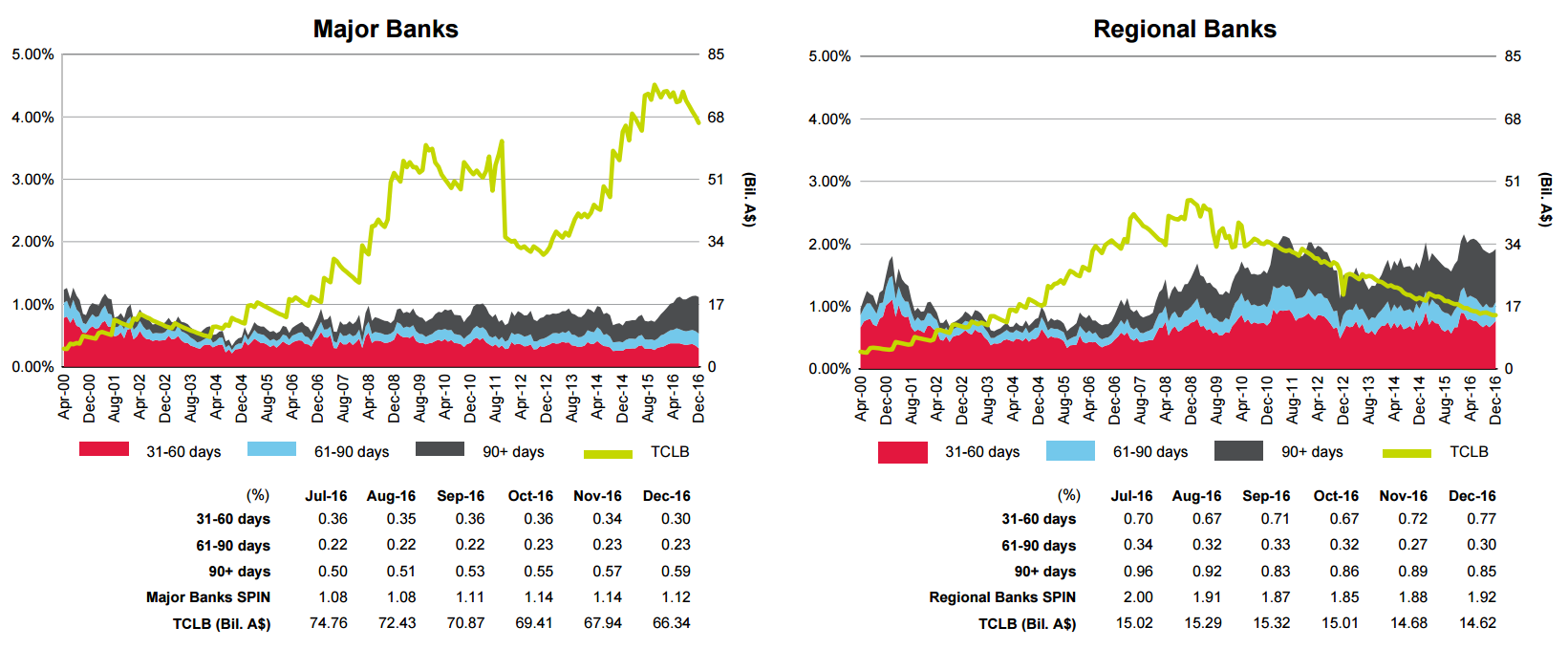

The number of delinquent housing loans underlying Australian prime residential mortgage-backed securities was unchanged in December from November, according to a recent report by S&P Global Ratings. Arrears typically rise between November and April. Arrears in December 2016 were up 20% from the same month a year earlier, but the rate of increase has slowed in recent months. A total of 1.15% of the mortgages underlying Australian prime residential mortgage-backed securities (RMBS) were more than 30 days in arrears in December, as measured by Standard & Poor’s Performance Index (SPIN), according to the “RMBS Arrears Statistics: Australia” report. Arrears are still low at these levels, but it is interesting that prime arrears have increased by around 0.19% during the past 12 months, despite an around 0.40% reduction in standard variable rates. Mortgage arrears typically are sensitive to interest-rate movements because most loans underlying Australian RMBS transactions are variable rate. In recent months, however, there has been a divergence from this trend. Arrears movements were mixed among the originator types. Major banks was the only category that reported a fall in arrears, slipping to 1.12% in December from 1.14% in November, and arrears remained unchanged for nonbank originators, at 0.95%. Regional banks have the highest arrears of all originator types, at 1.92%, and the highest percentage of loans more than 90 days in arrears, at 0.85%. Nonbank financial institutions have the lowest number of loans more than 90 days in arrears, at 0.25%. Major banks recorded the largest year-on-year increase in mortgages that are more than 90 days in arrears, but at 0.59%, advanced-stage arrears remain low for this sector.

Expect new highs in H1 as the pot-Xmas squeeze arrives.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.