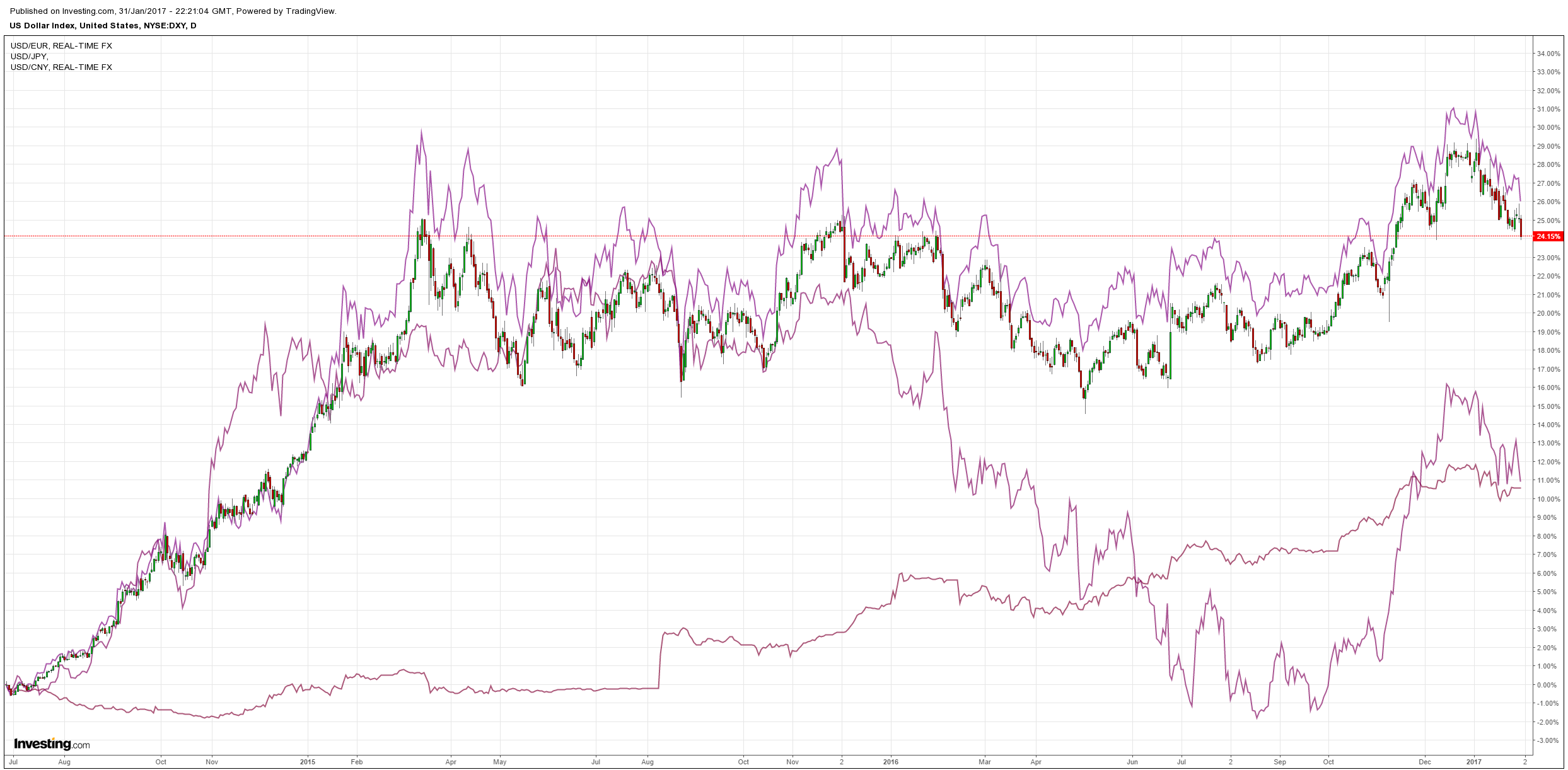

Running through the numbers of the past week is not pretty for the long US trade. DXY has been getting pounded and other majors rebounding:

Commodity currencies have been firm:

Gold has rebounded:

Advertisement

Brent is firm:

Base metals want to break higher as the USD slumps:

Advertisement

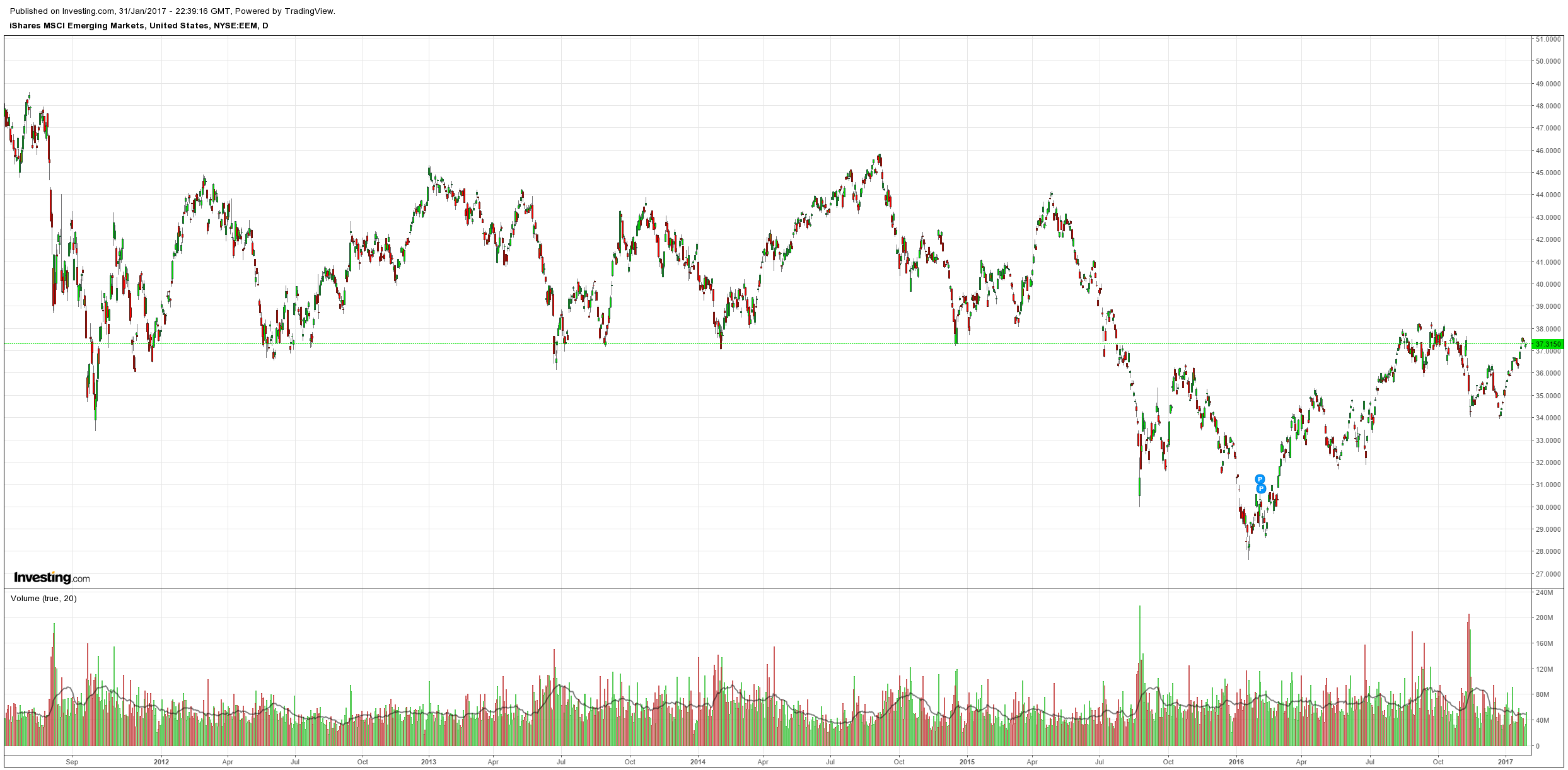

EM stocks have rebounded:

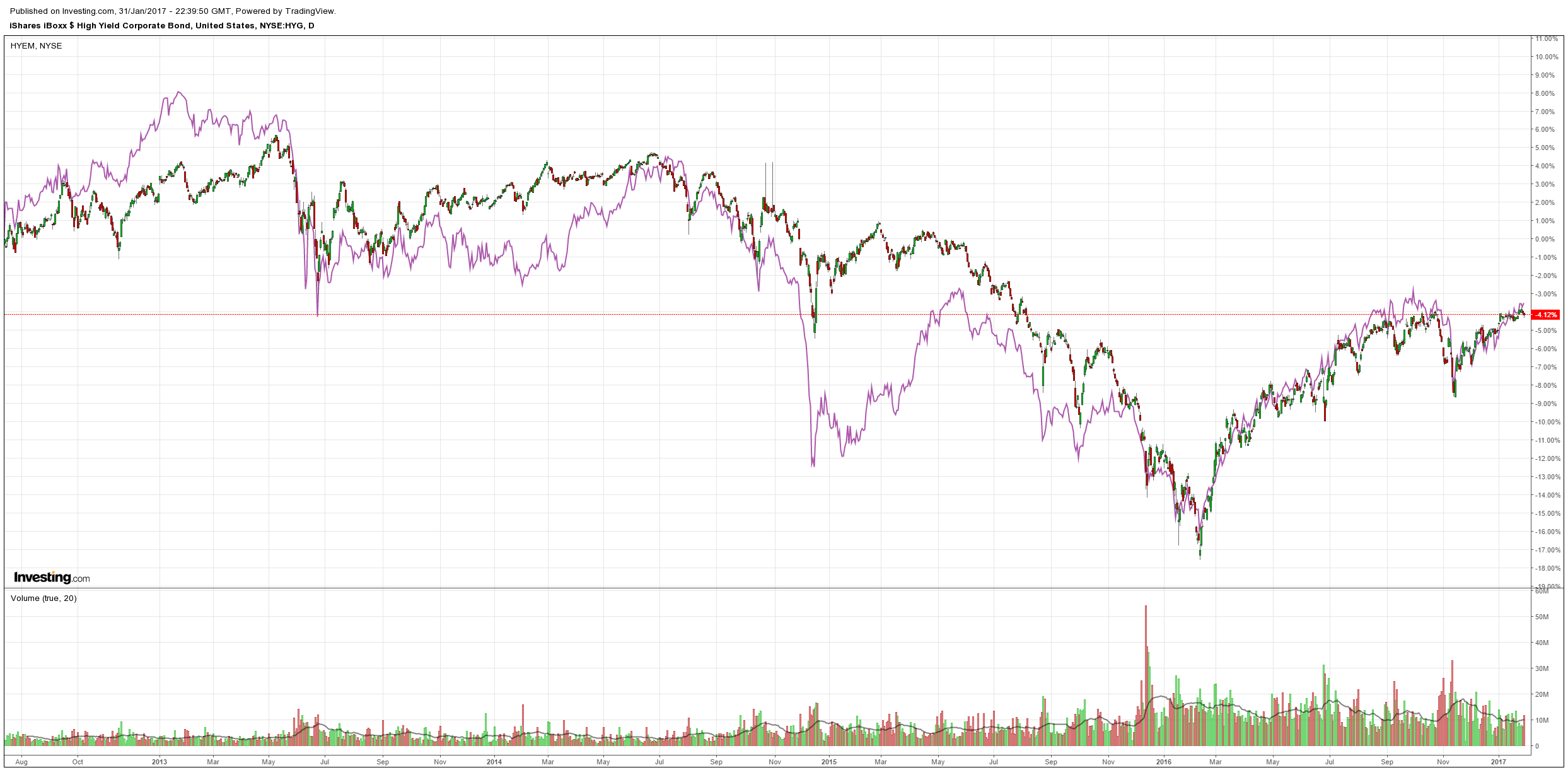

And high yield debt:

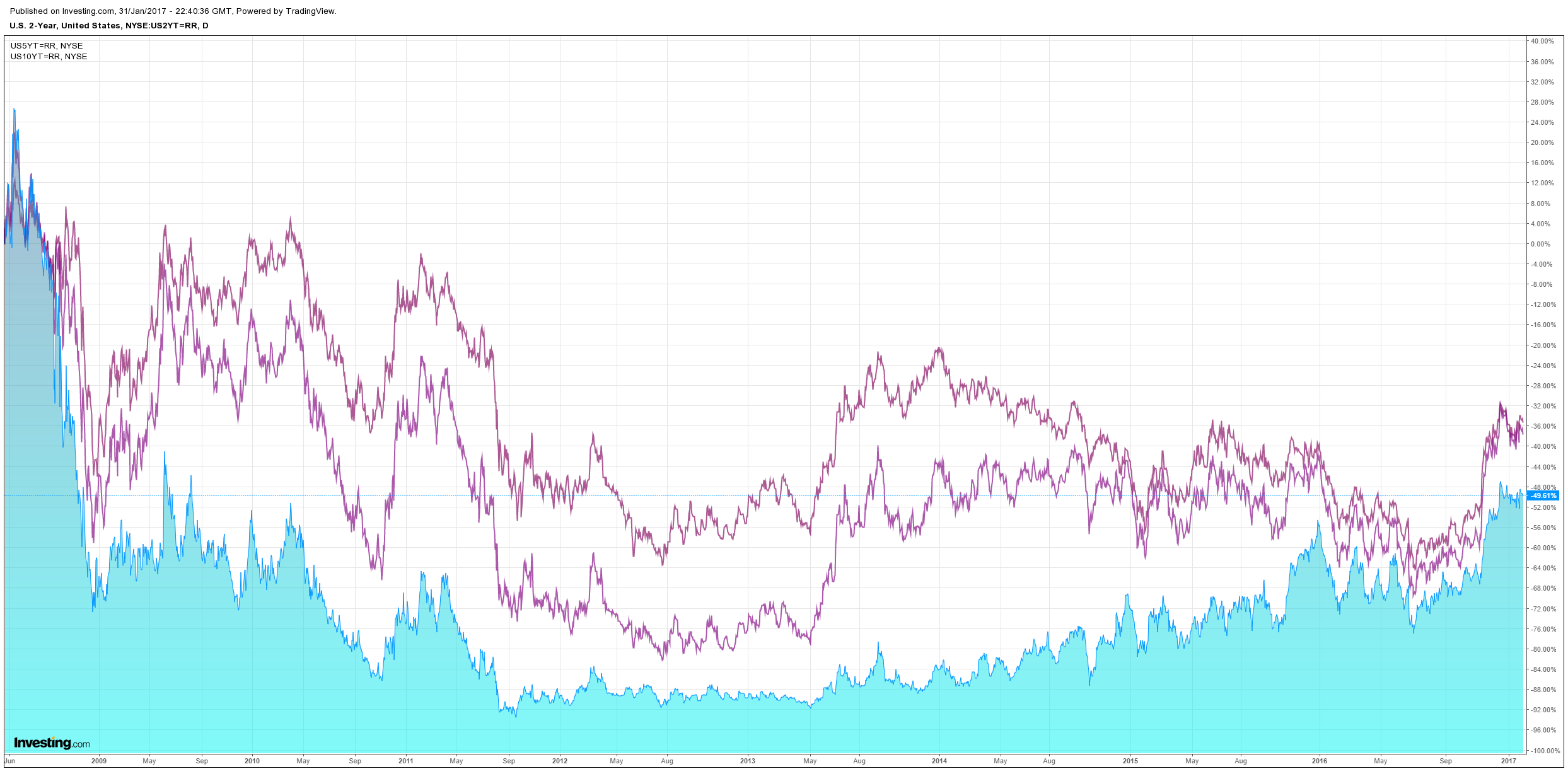

US bonds have been bought a bit:

Advertisement

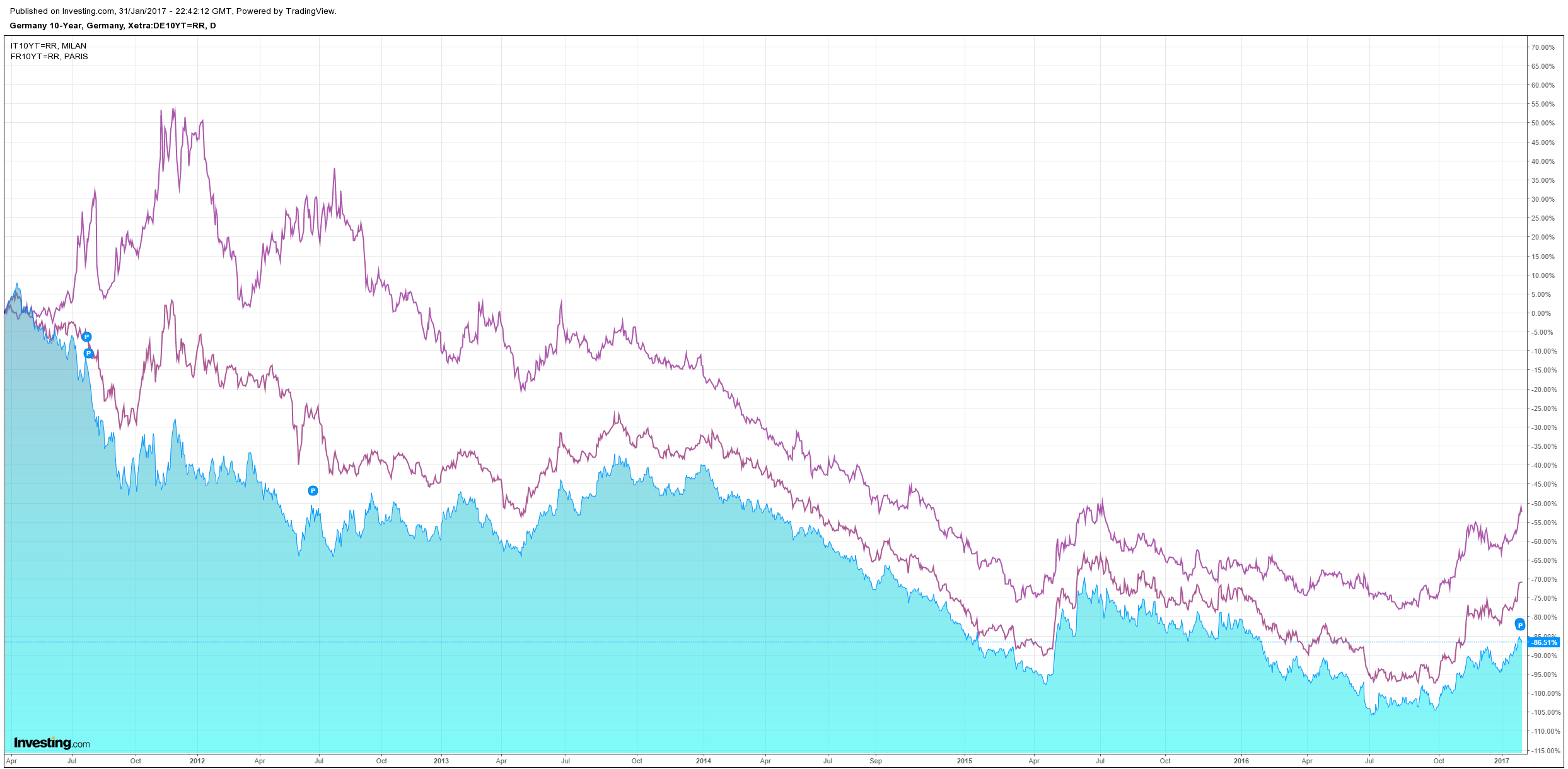

But European spreads are marching:

And Us stocks have tried but failed to sell:

Most of the damage to the long USD trade has been in the currency and HSBC has a good explanation for why:

Advertisement

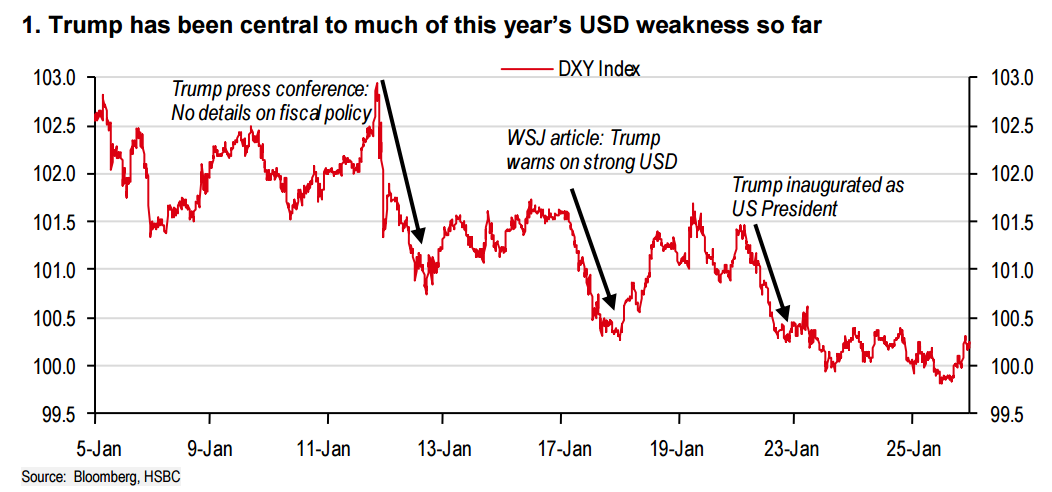

It has been a difficult start to the year for USD bulls. The currency has already reversed more than half of the rally seen in 2016 after Donald Trump’s unexpected election victory. But if Mr Trump was the catalyst for that earlier strength, it seems that he has also been the catalyst for much of the weakness in January. Chart 1 shows the DXY USD index during so far this year. Three of the big dips in the USD coincide with Trump-related developments.

The press conference

The first bout of USD weakness came after Trump’s press conference on 11 January. The market appeared disappointed that the then president-elect failed to offer any excitement regarding fiscal policy. This was perhaps a bit unfair as the press conference had been called to address the issue of how Mr Trump would manage his business conflicts of interest once president. It was not intended to be a broad discussion of policy plans. Nonetheless, the lack of a reflation focus saw the USD weaken alongside falling US Treasury yields.

Trump’s inauguration speech

The most recent setback for the USD came in the wake of Trump’s inauguration speech. The emphasis on putting America first echoed the tone of his campaign but consequently played more to themes of isolationism and protectionism rather than a comprehensive reflation of the US economy. Once again, the USD succumbed to Trump’s words. As president, his subsequent executive orders extracting the US from the Trans Pacific Partnership, calling for a renegotiation of NAFTA and commencing the process for building a wall on the Mexican border gave the market little reason to reassess their interpretation of his inauguration speech.

WSJ interview – the most pertinent

But it was his direct comments on the USD in an interview with the Wall Street Journal that was probably the most significant development. It was unusual not only because his observations ran counter to the long-standing strong USD policy of the US Treasury but also because comments on the USD have typically been the purview of the Treasury secretary and occasionally the US Federal Reserve. But presidents have generally steered clear of this topic, especially any hint that USD weakness would be preferred.

An example of this occurred during the Obama presidency. At a G7 summit in June 2015, Bloomberg reported that President Obama had said that a strong dollar was a problem according to a French official. The White house subsequently denied that any such observation had been made suggesting instead that he had simply said that “global demand is too weak and that G7 countries need to use all policy instruments, including fiscal policy as well as structural reforms and monetary policy, to promote growth”. This clarification not only contained no reference to a desire for a weaker USD, it contained no reference to the dollar at all. The White House traditionally does not step on the Treasury’s lawn when it comes to the USD.

So Trump’s observations on the USD were another break from convention and were the catalyst for a sharp sell-off in the USD. His Treasury Secretary Nominee later said Mr Trump’s comments “were not meant as a longer-run policy” and that a strong and “dependable” USD remains important. But for a currency market, seniority is crucial and if the President is talking about the USD, he is going to out-rank the Treasury in terms of market potency.

Trump verbal intervention behind January weakness

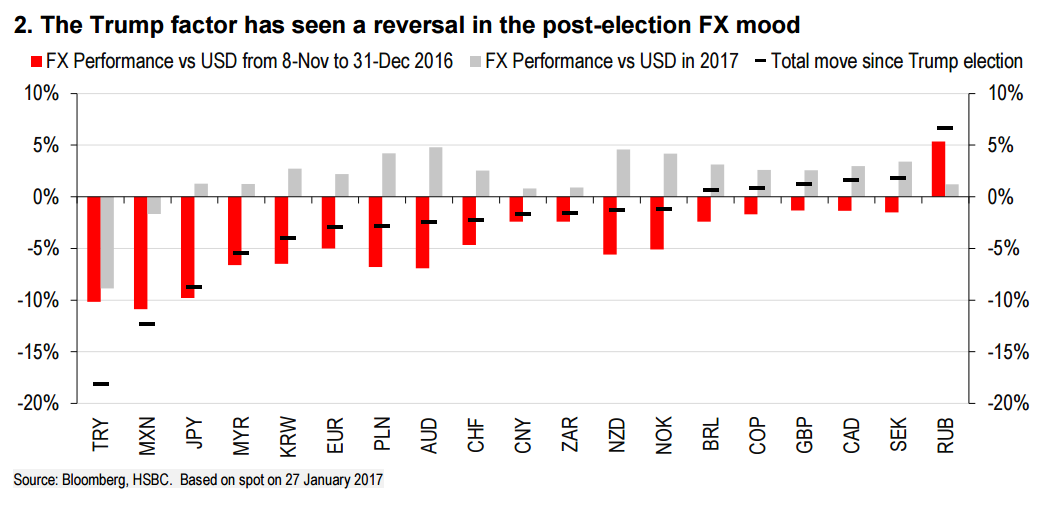

Therefore, the Trump factor in January has been a key driver of the reversal of currency trends that had been in play during November and December 2016 after his election win. He has talked the USD down and failed to talk reflation expectations higher. Chart 2 illustrates this swing in sentiment.

It is interesting to note that EM FX has participated in this swing in sentiment even though some of the USD retracement has been prompted by the President’s more protectionist tendencies. One might have expected protectionist fears to be negative for these currencies. Even the MXN, which is at the forefront of many Trump developments, is actually the best performing currency in the world since Trump’s inauguration day.

Positioning may be a key part of the explanation. The flipside to the Trump-prompted liquidation of USD longs may have been a reduction in shorts elsewhere. Judging by the price action, it seems that the position adjustment has been widespread.

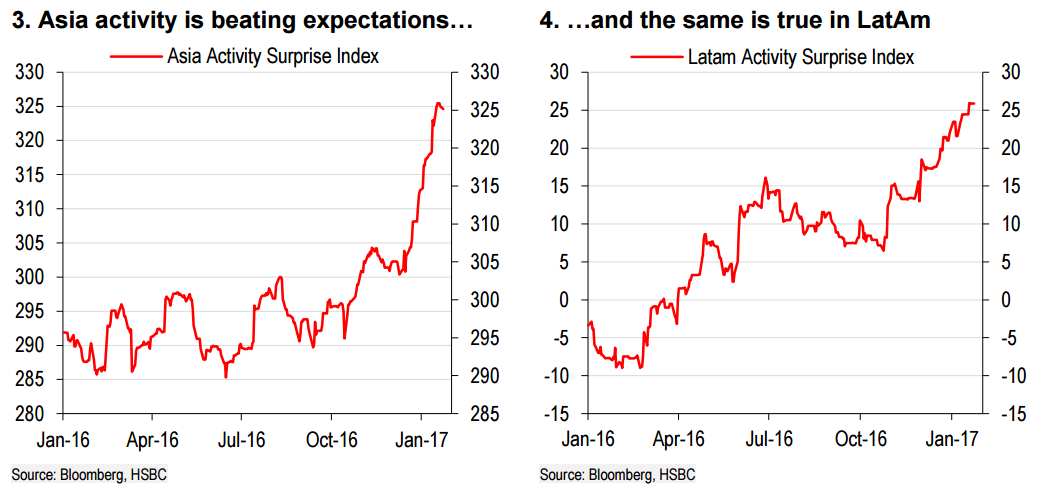

Another potential reason that EM FX has not succumbed to Trump’s more protectionist tone is that while the US president is spending less air-time talking about his reflation plans, the rest of the world is enjoying its own reflation. Economic activity has been picking up globally and in many cases more swiftly than expected. Charts 3 and 4 show the economic surprise indices for activity in Asia and LatAm respectively. The trend is clear. The data have been consistently better than expected. In the world of FX where everything is about relatives rather than absolutes, the growing realisation that the reflation theme need not be exclusive to the US is holding back the USD.

USD rally to resume

President Trump may have been a key element of why the USD rally has stalled in January, but he is also likely to be the reason why the rally will resume. In the wake of UK Prime Minister Theresa May’s recent speech on her vision for Brexit, the Der Spiegel newspaper dismissed her strategy as a list of “I want, I want, I want”. Similarly, Trump may want a weaker USD to help in his fight to make America more competitive and rein in the trade deficit, but he wants lots of other things too that point to USD strength, not weakness.

In economics, we hear the phrase “impossible trinity”, which states it is impossible to control the exchange rate, have independent monetary policy and allow the free movement of capital. Looking at Trump’s policy agenda, he also has elements and strategies which may be mutually exclusive – an “impossible Trump-ity” perhaps.

You can’t have everything

He thinks the USD is too strong and that it is killing the US economy. But he also wants to cut taxes and increase spending, a strategy that is likely to see the USD rise. He wants to encourage investment in the US and discourage capital from leaving, again a USD positive. He wants to bring jobs back to the US and limit immigration, implying a tighter labour market, a more hawkish Fed and a stronger USD. Repatriation of overseas earnings and a border adjustment tax would only add to the appreciation pressure.

So it is possible that Trump will continue to express the merits of a weaker USD but rhetoric loses its potency after a while unless it is followed up by action to deliver that depreciation. One only has to look at Japan’s experience. Frequent expression of discomfort by Japanese policymakers with JPY strength during Q3 16 seldom had a lasting impact because it was never followed by action.

In addition, the USD will get support from a likely shift in US policy focus back to the more reflationary themes of tax cuts, spending increases and deregulation. The protectionist tone evident during January is because the initial policy focus was on areas that Trump could act on swiftly through executive orders, notably trade and immigration. Acting on these fronts has demonstrated the president is going to act on his campaign promises. In the coming months, this will require him to work with Congress to deliver his fiscal reform plans. This is when the USD will recapture its reflationist mojo and rally. The US will regain the initiative in the global reflation theme. When the rest of the world is enjoying a rather passive upswing in activity, the US will be super-charging its economy with fiscal stimulus. That, at least, will be the likely tone in the currency market.

Conclusion

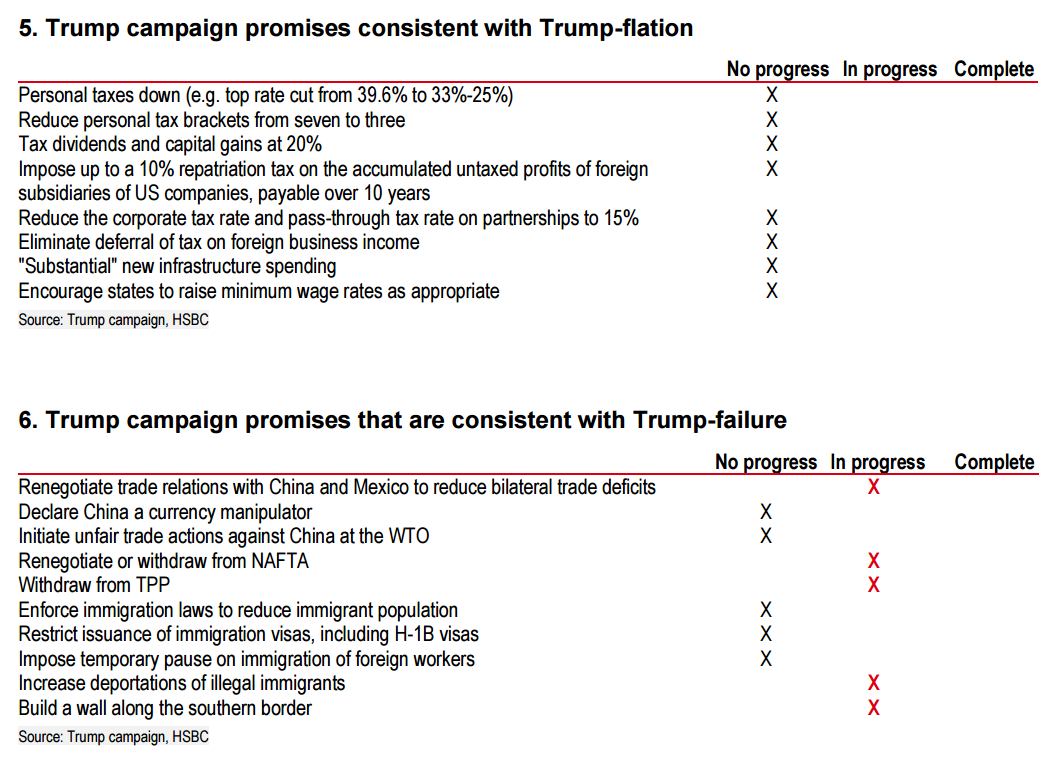

President Trump has broken with convention by talking the USD down. He has been a key factor behind the USD’s retreat in January. His policies so far have been consistent with Trumpfailure, and he is yet even to get the ball rolling on his campaign promises consistent with Trump-flation (tables 5-6). This means the President is also likely to be the key element that restarts the USD rally as his policy focus moves from executive orders on trade and immigration to the USD bullish theme of reflation through tax cuts, increased spending and deregulation. The President may want a weaker USD but his campaign promises point in the opposite direction. January’s price action has not changed our view that the USD is set for a strong H1 16 before reversing lower in H2. January has simply been a taster of the reappraisal to come. For now, we expect the USD bulls to regain the upper hand.

That is very nice summary of where we’re at. The politics of symbolism is dominant for now and is as good a reason as any for the long US trade to pull back from what were very over-bought levels. But that is an opportunity not as reversal. Next up, Trump must deliver higher growth and a better jobs market to his voters or all of the symbolic politics in the world won’t save him from an electoral caning.

As well, Europe and the euro remain structurally buggered, Japan will remain loose and China, as well as EMs will slow.

Advertisement

At MB our allocations remain:

sell AUD rallies;

buy S&P500 dips;

sell commodities on rallies;

buy Aussie bonds on dips;

buy gold on dips as portfolio insurance (not for imminent return).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.