No surprises last night as markets digested the Fed announcement to hold. DXY fell and other majors rose:

Commodity currencies rose:

Gold was stable:

Advertisement

Oil looks strong, it may want to see more US shale. If so, it will get it:

Base metals were flat:

Advertisement

Emerging market stocks too:

High yield debt fell:

US bonds were bought a little:

Advertisement

European spreads widened:

And stocks were flat:

The big news was no news from the Fed:

Advertisement

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has continued to expand at a moderate pace. Job gains remained solid and the unemployment rate stayed near its recent low. Household spending has continued to rise moderately while business fixed investment has remained soft. Measures of consumer and business sentiment have improved of late. Inflation increased in recent quarters but is still below the Committee’s 2 percent longer-run objective. Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will rise to 2 percent over the medium term. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1/2 to 3/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

It’s in wait and see mode viz fiscal policy.

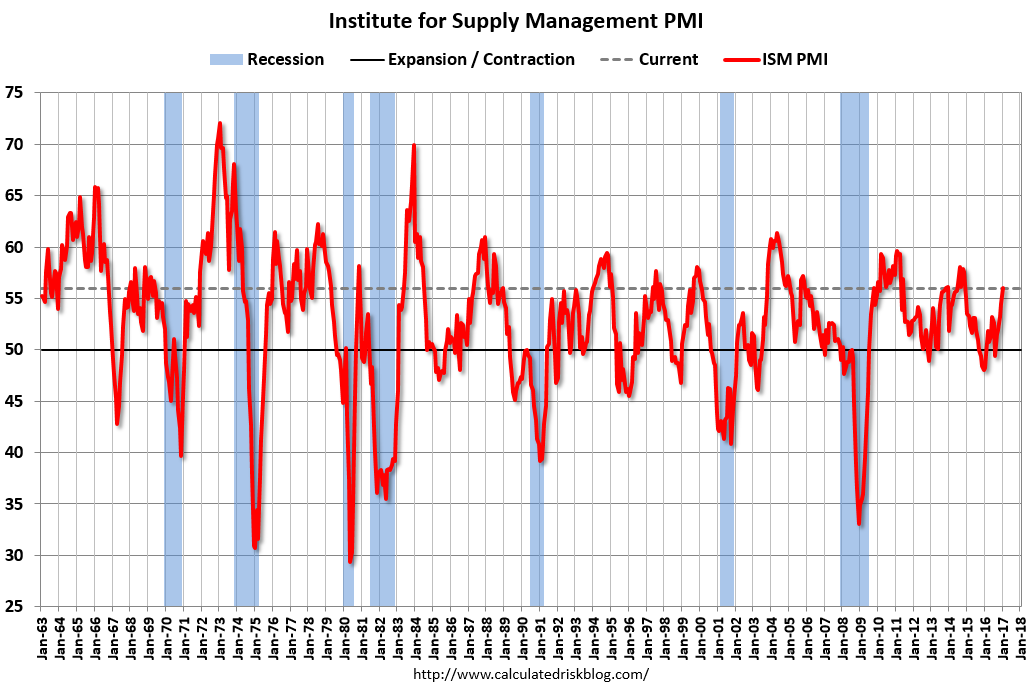

However, data was very good with the ISM powering back with the shale sector (chart from CR):

The January PMI® registered 56 percent, an increase of 1.5 percentage points from the seasonally adjusted December reading of 54.5 percent. The New Orders Index registered 60.4 percent, an increase of 0.1 percentage point from the seasonally adjusted December reading of 60.3 percent. The Production Index registered 61.4 percent, 2 percentage points higher than the seasonally adjusted December reading of 59.4 percent. The Employment Index registered 56.1 percent, an increase of 3.3 percentage points from the seasonally adjusted December reading of 52.8 percent. Inventories of raw materials registered 48.5 percent, an increase of 1.5 percentage points from the December reading of 47 percent. The Prices Index registered 69 percent in January, an increase of 3.5 percentage points from the December reading of 65.5 percent, indicating higher raw materials prices for the 11th consecutive month. The PMI®, New Orders, and Production Indexes all registered their highest levels since November of 2014, and comments from the panel are generally positive regarding demand levels and business conditions.

The ADP employment report powered:

Advertisement

“The U.S. labor market is hitting on all cylinders and we saw small and midsized businesses perform exceptionally well,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Further analysis shows that services gains have rebounded from their tepid December pace, adding 201,000 jobs. The goods producers added 46,000 jobs, which is the strongest job growth that sector has seen in the last two years.”

Mark Zandi, chief economist of Moody’s Analytics said, “2017 got off to a strong start in the job market. Job growth is solid across most industries and company sizes. Even the energy sector is adding to payrolls again.

And GDPNow is rocking:

The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2017 is 3.4 percent on February 1, up from 2.3 percent on January 30. After this morning’s ISM Report On Business from the Institute for Supply Management and the construction spending release from the U.S. Census Bureau, the forecasts for first-quarter real personal consumption expenditures growth and real private fixed investment growth increased from 3.0 percent to 3.8 percent and 4.7 percent to 8.0 percent, respectively.

It’s not exactly rude health but it’s pretty good. Add some moderate fiscal support and it’s boom times for a while.

The Fed will be forced to tighten a couple more times this year and a rollicking US dollar should do the rest.

Advertisement

MB our allocations remain:

sell AUD rallies;

buy S&P500 dips;

sell commodities on rallies;

buy Aussie bonds on dips;

buy gold on dips as portfolio insurance (not for imminent return).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.