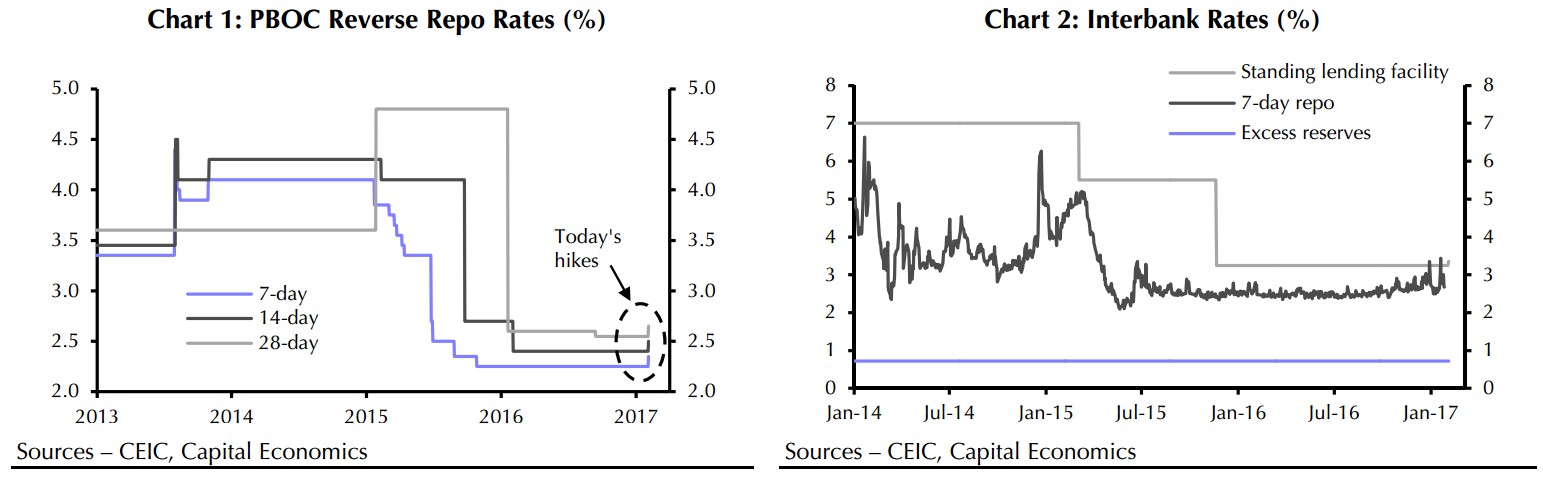

The People’s Bank has raised the interest rate that it charges when providing funds in China’s repo market. This is the clearest evidence so far that monetary policy is being tightened and that supporting growth is no longer the primary immediate goal of China’s policymakers.

Effective today, the People’s Bank has raised the rates on the reverse repo operations it conducts with banks by 10 basis points. (See Chart 1.) The hikes are small and may not have much of an immediate effect on interbank repo rates which were already trading well above the rate offered by the PBOC.

Instead, the move is best seen as an official acknowledgement of the on-the-ground tightening that has been evident since November: the PBOC had previously been pushing interbank rates up by adjusting the quantity (rather than the price) of the funds it provides. In late January, the PBOC also increased the rate offered on its Medium-term Lending Facility (MLF). Nonetheless, the repo rate hikes provide the clearest confirmation yet of a shift toward policy tightening.

Repo rates are arguably more useful guides to the policy stance than the more closely-watched benchmark rates. Indeed, in our view, the 7-day PBOC reverse repo now functions as China’s de-facto policy rate. (See our Focus, “A primer on China’s new monetary policy regime”, 10th October 2016.)

After all, the repo market is now the primary channel through which the PBOC manages monetary conditions. Last year alone, the PBOC injected a gross RMB25trn via reverse repos, partly to offset liquidity withdrawals from foreign exchange sales. In contrast, gross injections via MLF, its next biggest channel for regular liquidity provision, totalled a mere RMB4.3trn.

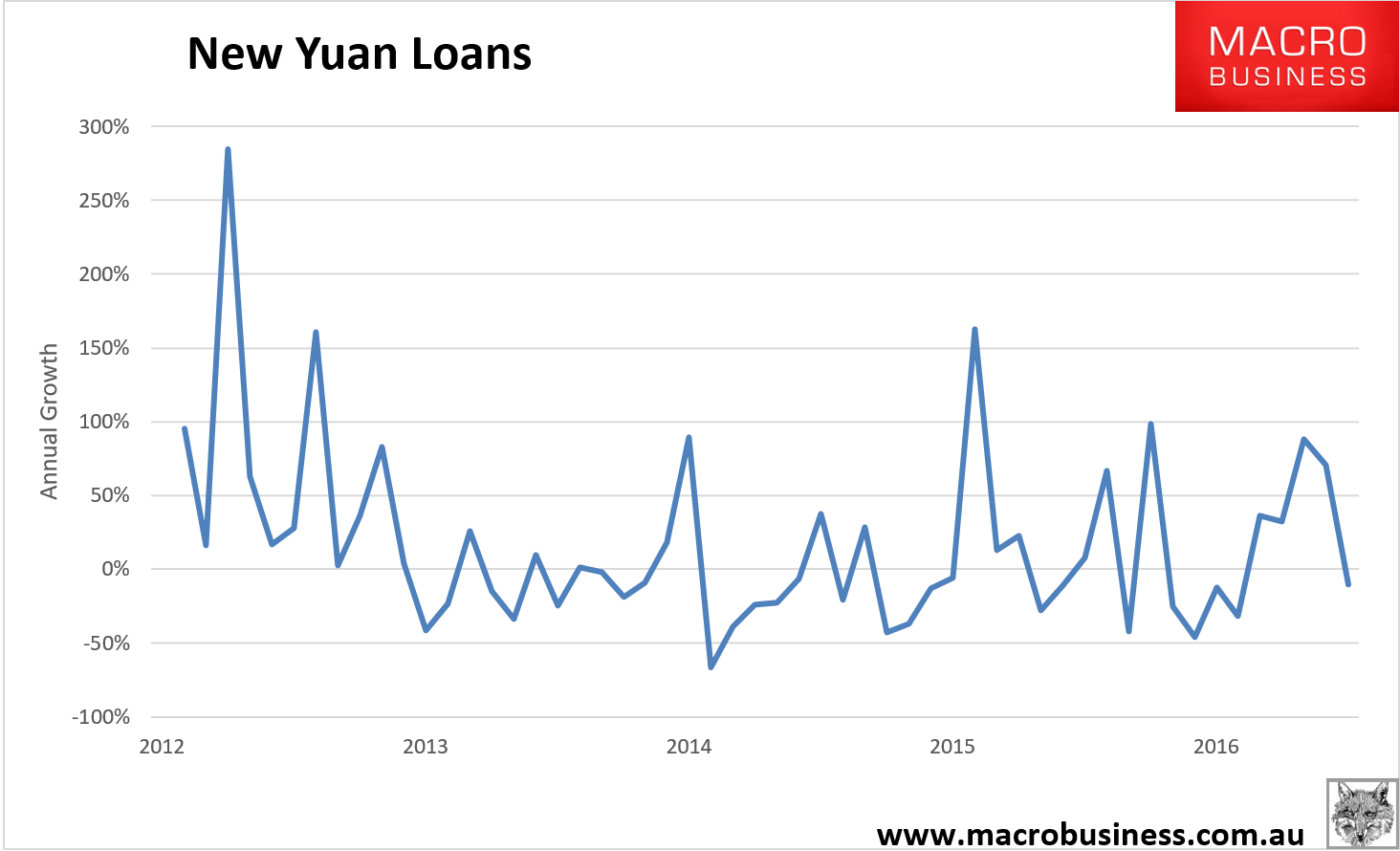

The growing importance of interbank rates reflects the diminished effectiveness of the traditional reserve requirement and benchmark rate tools in setting monetary conditions as credit markets have diversified. Unconfirmed reports suggest that the PBOC also raised the 7-day SLF rate today, from 3.25 to 3.35. This is noteworthy as the PBOC has previously suggested that it is operating an interest rate corridor around the 7-day interbank repo, with the rate on excess reserves serving as the floor and the SLF rate serving as the ceiling. (See Chart 2.)

The shift toward a tighter monetary stance appears driven by a desire to rein in credit growth and mortgage lending in particular. The PBOC began intervening to this end last autumn when it ordered banks to limit new mortgages. This window guidance appears to have had only limited success, however, and household lending remained strong at the end of last year. Local media reports suggest that the PBOC has since given banks much broader orders to tighten all new lending in Q1.

An increase in repo rates helps these efforts by feeding through into increased financing costs for bond issuers and shadow bank borrowers. It may also encourage banks to price their traditional loans at higher multiples of the benchmark lending rates, thereby dampening loan demand. We think that the PBOC is reluctant to adopt the more traditional route of raising benchmark lending rates for fear that doing so will hurt existing bank borrowers, whose interest payments are typically adjusted annually in line with changes to the benchmark rate. We are not expecting any benchmark rate moves this year but expect the PBOC 7-day reverse repo rate to end 2017 at 3.00%, up from 2.35% now.

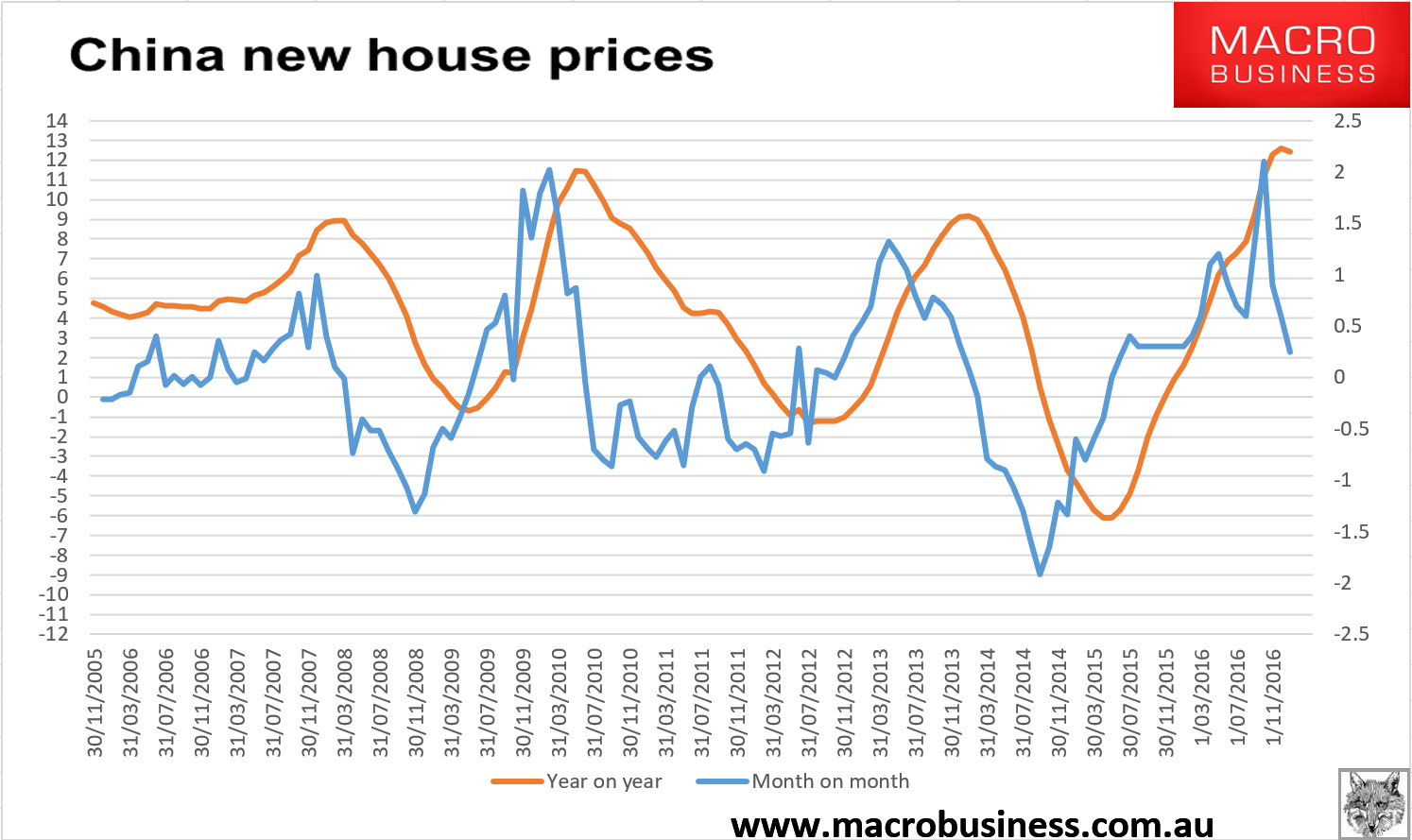

In sum, today’s rate hikes leave little doubt that the PBOC is prioritising efforts to contain credit risk over measures to support growth. Given this, it’s only a matter of time before credit growth, a key tailwind behind the economic recovery in 2016, starts to become a drag.

Actually, it’s been a drag already for a quarter as year on year new yuan loans begin to fall:

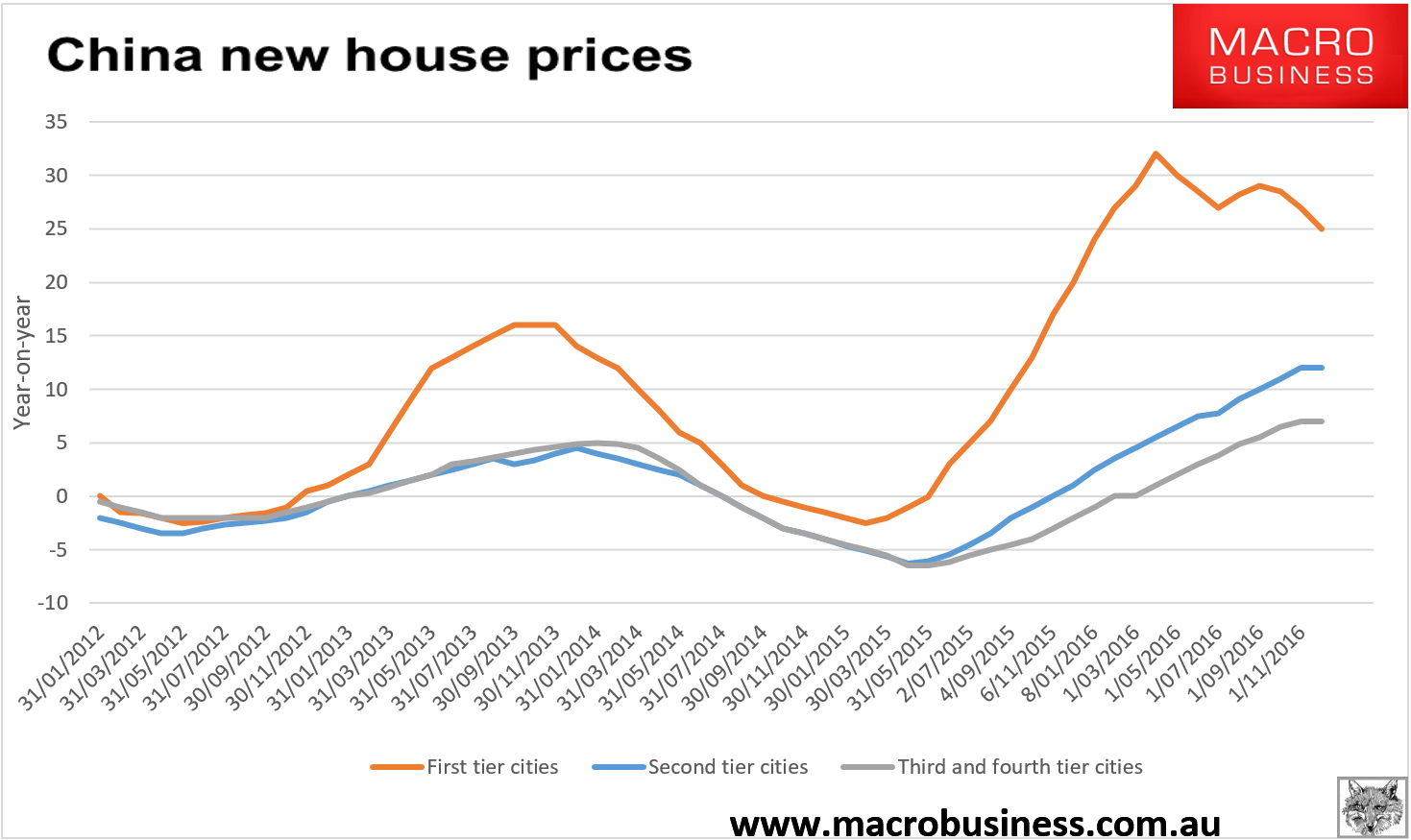

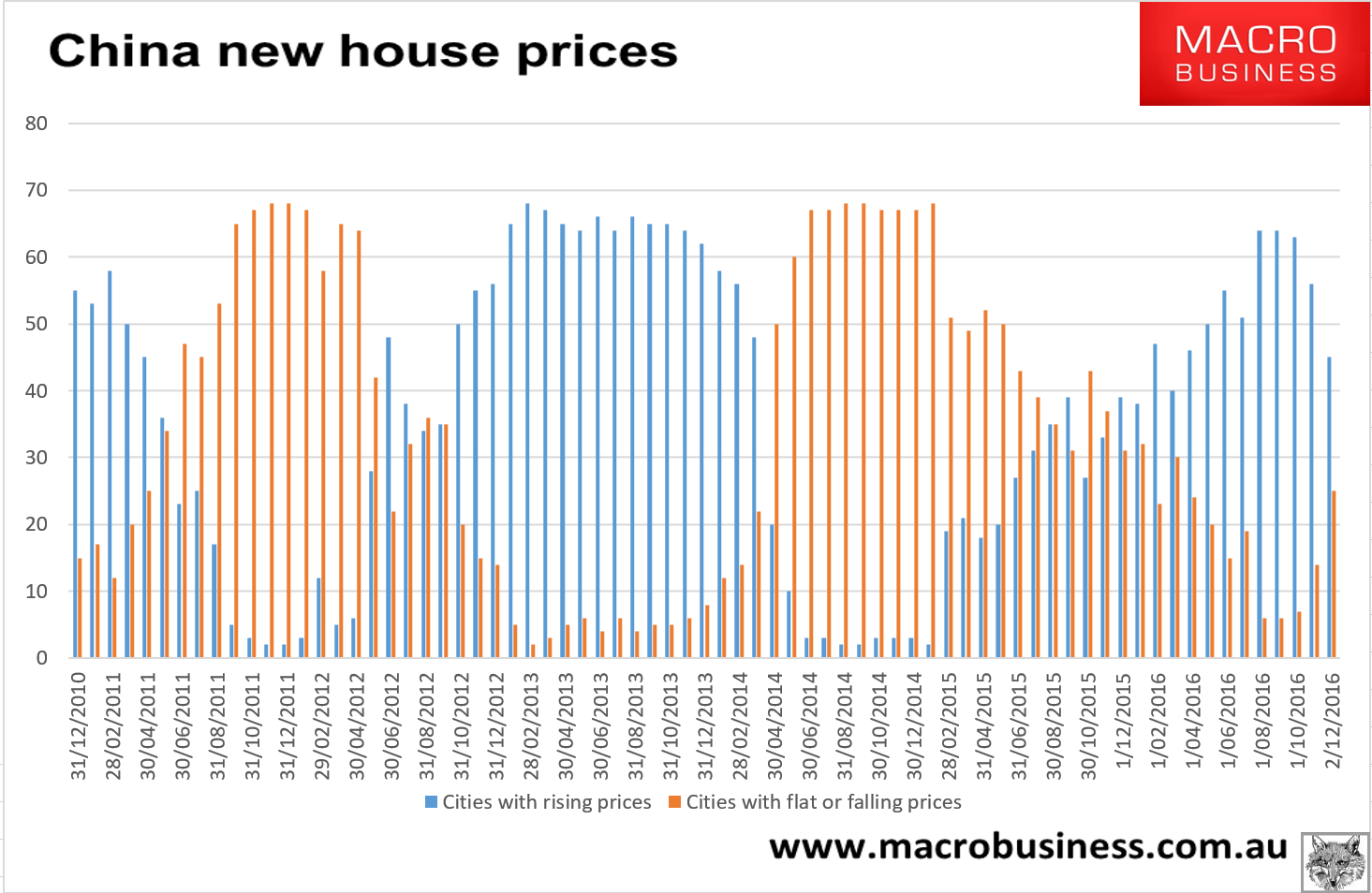

“Farewell Chinese stimulus” is a little strong. I expect the infrastructure roll out to continue. But the housing component is done. New house prices are already rolling over on last year’s prudential tightening:

Advertisement

The top tier city boom is over and year on year prices have a long way to slide back. Lower tiers have already slowed as well:

Advertisement

As the breadth of price falls begins to rise:

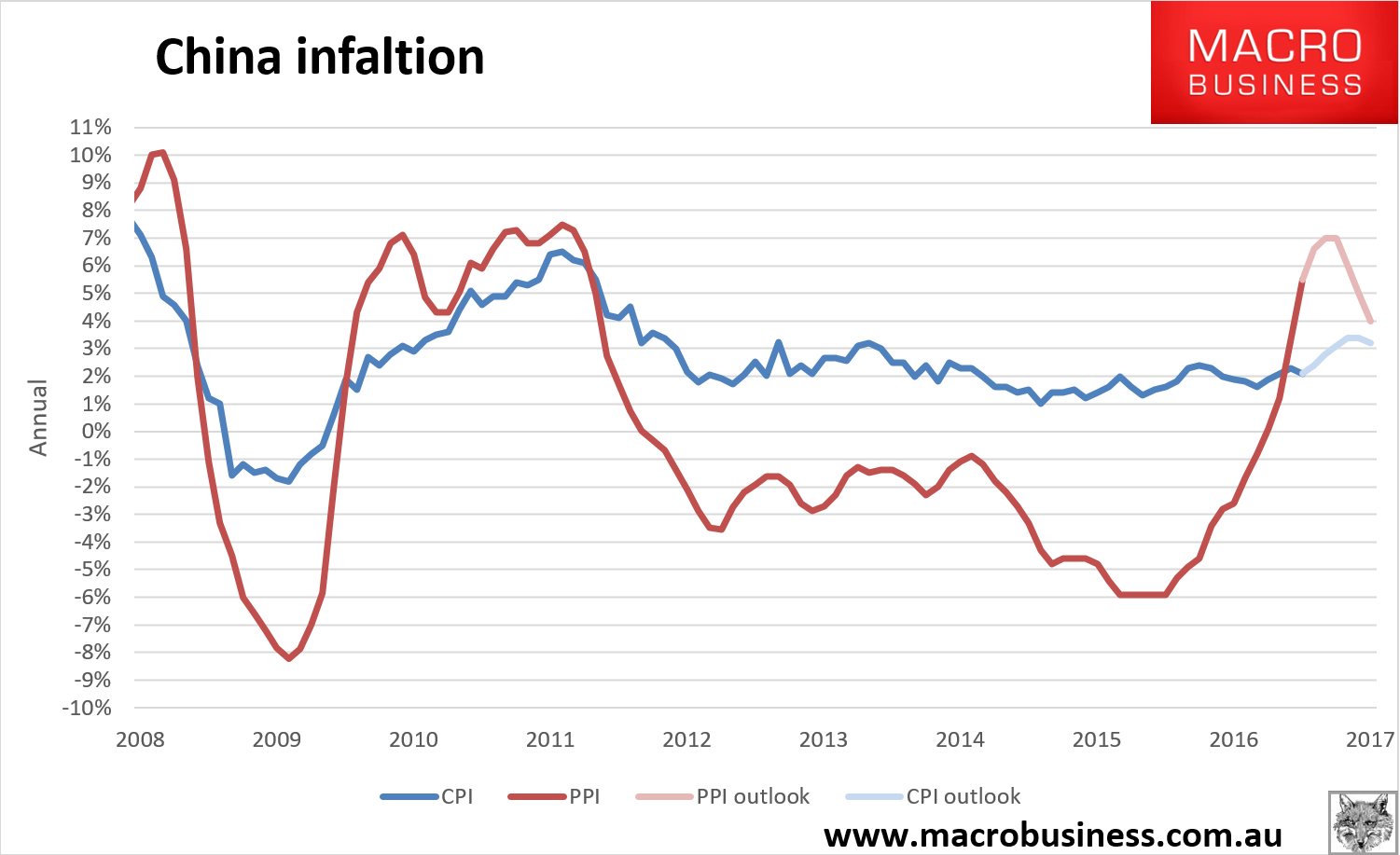

I mean, can we really be surprised here? Chinese producer inflation is off the hook:

Advertisement

I’ve maintained that China will slow modestly not crash this year and I’ll stick with that. But there’s quite a bit of tightening going on now and the risk of a sharper slowdown in H2 this year is rising with it.

Bulk commodity markets are so not positioned for this.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.