With a surge in exports driving a sharp narrowing in the Australian current account deficit, there could well be further upside to the AUD.

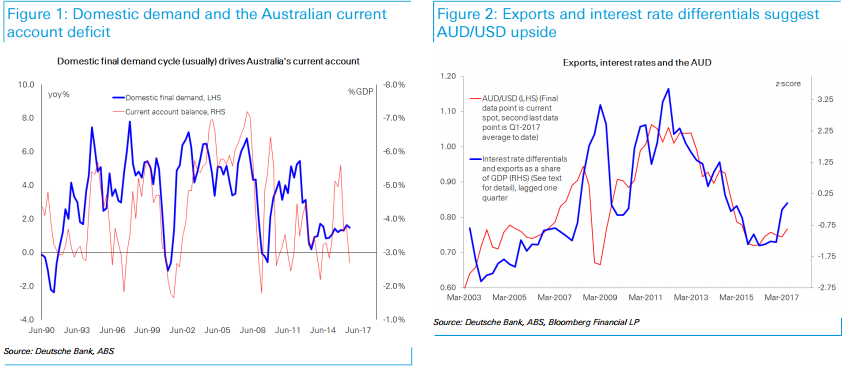

Typically, using the current account deficit to form a view on the AUD is problematic. This is because the current account deficit typically increases when the domestic economy is strong as shown in Figure 1. Such an environment (i.e. strong domestic demand) also sees rising interest rates in Australia and higher returns on Australian assets generally, complicating the relationship between trends in the current account and trends in the AUD. That also makes current narrowing in the current account deficit a little unusual (DB expects the current account deficit to have narrowed to 1.5% of GDP in Q4-2016 versus 5.5% of GDP a year earlier, with a further improvement appearing likely in Q1-2017). Instead of being driven by a weaker domestic economy lowering imports, the current narrowing in the current account deficit is being driven by a surge in exports.

That also makes current narrowing in the current account deficit a little unusual (DB expects the current account deficit to have narrowed to 1.5% of GDP in Q4-2016 versus 5.5% of GDP a year earlier, with a further improvement appearing likely in Q1-2017). Instead of being driven by a weaker domestic economy lowering imports, the current narrowing in the current account deficit is being driven by a surge in exports. It also prompts the question of whether or not an export driven narrowing in the current account can tell us something about the likely direction of the AUD? Interestingly, it appears that it can. In Figure 2 we plot AUD/USD against a combination of export values as a share of GDP and the ratio of the Australian

Interestingly, it appears that it can. In Figure 2 we plot AUD/USD against a combination of export values as a share of GDP and the ratio of the Australian

In Figure 2 we plot AUD/USD against a combination of export values as a share of GDP and the ratio of the Australian ten year bond yield to the US ten year bond yield (specifically, we calculate z-scores for each and then plot the sum of the two). In essence we are comparing export driven movements in the current account deficit to interest rate differentials; arguing that an export driven narrower current account, for any given interest rate differential, should see a higher AUD/ USD exchange rate (and vice versa). As Figure 2 shows, aside from a ‘miss’ during the GFC, our construction is not only highly correlated with the AUD, but in fact tends to lead movements in the currency. (The miss during the GFC reflected the extreme risk aversion at the time, but also the fact that Australian commodity export prices were based on longer-term contracts which lagged the turn in the global economy.) Exports as a share of GDP are likely to have been around 21.2% of GDP in Q4-2016, with a further increase to ~22% likely in Q1-2017 (given the increase in the RBA’s commodity price index in January). That surge in exports combined with the prevailing interest rate differential suggests

Exports as a share of GDP are likely to have been around 21.2% of GDP in Q4-2016, with a further increase to ~22% likely in Q1-2017 (given the increase in the RBA’s commodity price index in January). That surge in exports combined with the prevailing interest rate differential suggests risk of further upside in the AUD toward and indeed above 0.8000 as shown in Figure 2. That said, we doubt the AUD will make it all the way to the mid 80s against the USD as Figure 2 would currently imply. After all, such an appreciation in the AUD would likely feed back into the domestic economy and see interest rate differentials adjust lower.

So long as the terms of trade hold up this is a definite risk scenario. If the Coalition were to unveil any kind of housing stimulus in the budget then it would shift to a base case.

However, if ti happens I would see it as another great opportunity to get offshore. Chinese housing is going to slow this year and at some point the terms of trade come under pressure so I’d see any rise in the AUD as a temporary spike.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.