From the LATimes, Chinese officials appear to have finally succeeded in choking off the flight of capital into foreign property:

The mansion on Fallen Leaf Road in the secluded Upper Rancho neighborhood of Arcadia has all the trappings a wealthy buyer from China could want: a crystal chandelier in the entryway, marble floors, a home theater outfitted with a dozen reclining leather chairs and, naturally, a fortuitous eight bedrooms and eight bathrooms.

At $9.8 million, the recently built property is a relative bargain. A similar-sized home in Beijing would cost twice as much.

Yet two months after it was placed on the market, the house remains unsold. Not long ago, real estate like this would have been snapped up almost immediately.

“It would have been gone in two weeks with multiple offers,” said Dee Chou, the property’s listing agent.Other real estate agents in the area report luxury homes geared toward Chinese buyers taking up to half a year to unload.

“All agents are crying that the money isn’t coming,” said Sanne Lee, an agent for A + Realty & Mortgage in Rowland Heights.

At the same time, high-end home seekers who plan to take out loans now have a fighting chance as they compete against a smaller pool of cash buyers.

The turnaround in activity, industry officials say, is directly linked to policies in China.

The San Gabriel Valley, long the destination of Chinese home buyers looking to provide their families a better living environment as well as safeguard their wealth in American assets, is feeling the effects of Beijing’s crackdown on capital flight.

…To defend against capital flight, Chinese regulators allow citizens to take out only $50,000 a year. But that’s been largely ignored and circumvented, often by asking dozens of friends and family to exercise their quota on someone else’s behalf.

“It’s like ants moving rice,” said Helen Chen Martson, a San Gabriel Valley real estate agent for Keller Williams.

The deluge in Chinese money made it exceedingly hard for local buyers to compete.

…But starting in 2015, Chinese banks began scrutinizing requests for foreign currency to ensure transactions were being used for legal business purposes. Regulators also increased their enforcement efforts given the many creative ways money is siphoned out — be it by forging trade invoices, smuggling jewelry and luxury watches out or even faking legal disputes to get cash into the hands of overseas lawyers.

Then on Dec. 31, China’s State Administration of Foreign Exchange, which swaps Chinese yuan for dollars, issued some of its strictest guidelines yet. Customers now have to pledge not to invest in foreign property and provide a detailed account of how foreign funds will be used. They also prohibited customers from taking foreign currency out for someone else.

The rules could have broad implications around the world for any city exposed to Chinese real estate investment such as Vancouver, Sydney and more recently, Seattle.

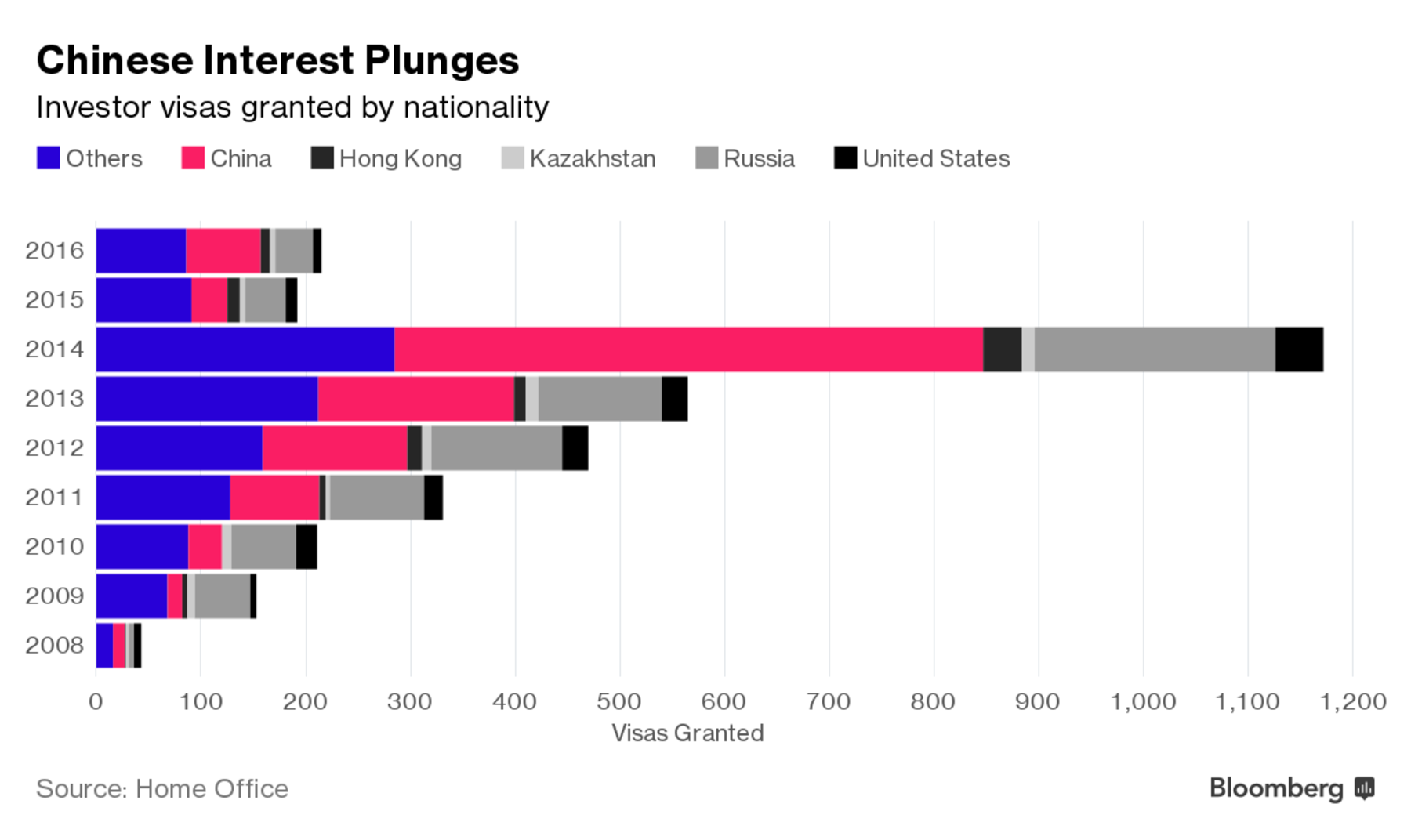

The number of wealthy people granted investor visas to live in the U.K. fell by more than 80 percent last year from the peak in 2014, a sign that luxury home sales in the capital may slump further.

While so-called Tier 1 investor visas rose 12 percent in 2016, the total granted was just 215, according to government data published on Thursday. That compares with 35,000 high-end properties planned for the city.

London’s luxury housing market has been beset by tax hikes, fears of oversupply and political uncertainty. Some developers hoped that the 16 percent fall in the pound since the referendum would help stabilize values in the capital’s best districts, which have fallen 12.5 percent from their 2014 peak as higher sale taxes and the Brexit vote damp demand, broker Savills Plc said in January.

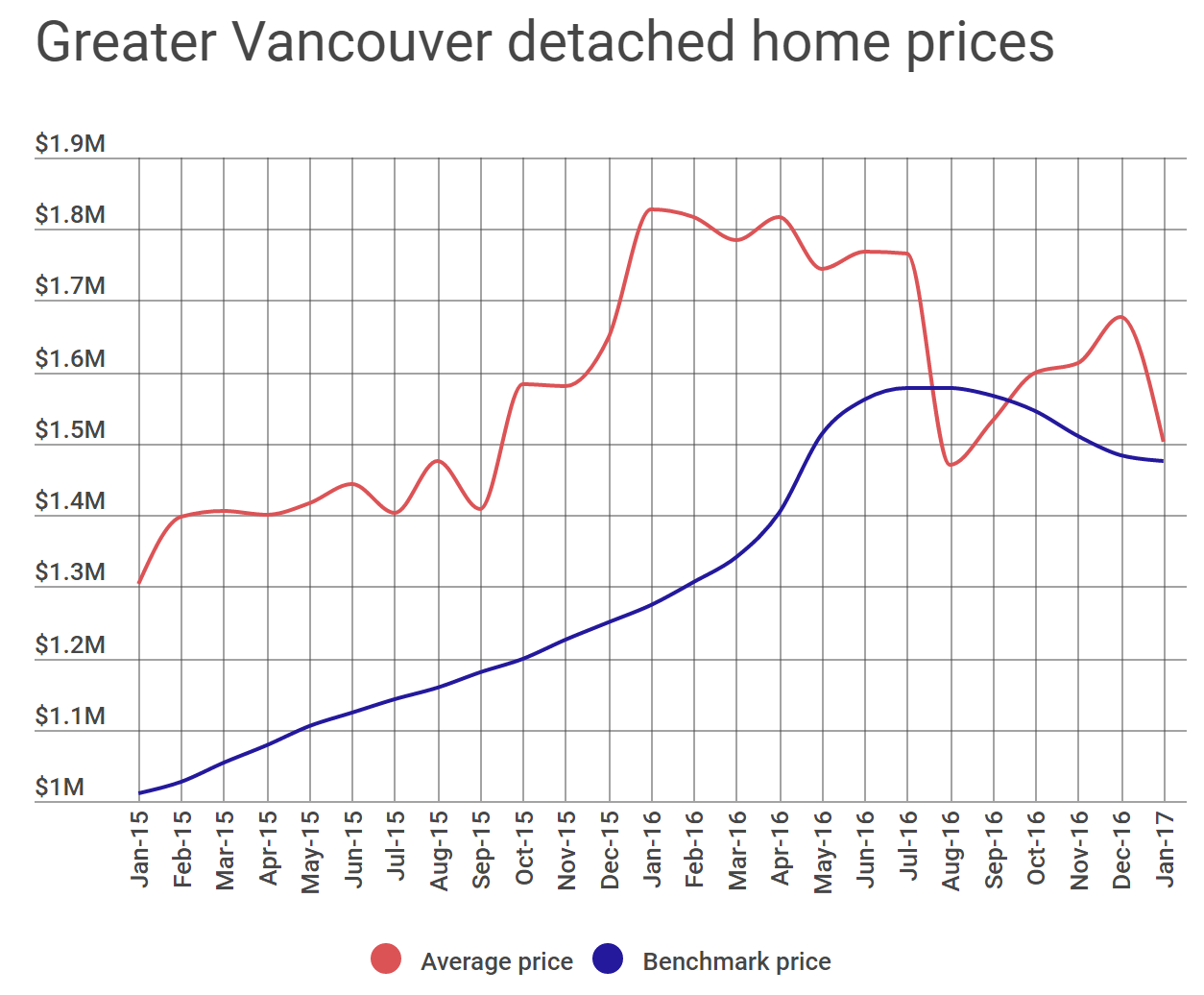

Residential home sales in B.C. are forecast to slide 14.1 per cent in 2017 and the average home price should fall nearly five per cent, according to a report from the B.C. Real Estate Association (BCREA).

The association says “rising property tax burdens aimed at foreign buyers and at sales of homes valued over $2 million have impacted home transactions, especially in Metro Vancouver.”

It also cites tighter federal mortgage regulation as a roadblock for first time homebuyers with low equity from entering the market.

On the supply side, a boom in new home construction is likely to keep the housing stock high, according to the report.

Those factors will likely drop the average home price down to $657,000, mostly due to a softening of the luxury market in Metro Vancouver.

The Australian government and media is so corrupt around this question that it is very difficult to know what’s happening here. However the FT is reporting it’s going sour:

Advertisement

Zhang Biao, a 32-year-old Chinese entrepreneur, has already thought about where his eight-year old will go to university. “We thought a flat overseas would be a good investment, and our son could use it for sixth form or university in Australia or the UK,” he says. Mr Zhang and his wife put an offer down on a A$600,000 (£354,000) flat in Melbourne in October — only to be told that they were no longer eligible for the 60 per cent loan-to-value mortgage they had applied for. Instead they decided to pay up front for a £120,000 flat in the English city of Liverpool.

…“Chinese buyers are increasingly nervous about Australia because of recent instability in regulation, tax and bank lending rules,” says Esther Yong, co-founder of ACproperty, a Chinese language property portal. “A lot of Chinese who bought apartments off-plan three years ago are now finding it difficult to find finance as Australian banks have blocked lending to foreign buyers,” she says. The big four Australian banks — NAB, Commonwealth Bank of Australia, ANZ and Westpac — have all stopped issuing loans to non-resident borrowers with no domestic income.

“We have essentially shut down mortgages to non-resident buyers,” Shayne Elliott, ANZ chief executive, told the FT. He said the apartment market in Melbourne was “a little bit concerning” due to the proliferation of small apartments, some under 50 square metres in size and with no bedroom windows, in the city centre.

…“For some Chinese buyers who have family connections in Australia then they will continue to buy there. But for others without these specific reasons, they will look at other opportunities,” said Ms Yong.

My guess is that the overall global market for Chinese property buyers has now been severely curtailed for anyone not rich enough to dodge Chinese capital flight rules. Whether Australia increases or decreases its market share within that shrinking pool is a moot question.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.