Via Martin North:

Today the CBA has announced changes to some mortgage rates: interest only home loan rates for investors will rise by 12 basis points and Viridian Line of Credit (VLOC) products will increase by 4 basis points. The new interest only standard variable rate for investors will be 5.68% per annum, VLOC will move to 5.82% per annum.

These changes will be effective from 3 April. For customers who may want to switch to principal and interest repayments to avoid this increase, they can do so easily – online, over the phone or in branch – at no cost.

CBA supported 140,000 new home loans in the six months ended December 2016 and our standard variable rate (SVR) for owner occupiers of 5.22% per annum remains the lowest among the major banks.

They just released their 1H17 results, which show a statutory net profit after tax (NPAT) of $4,895 million, which represents a 6 per cent increase on 1H16 period. Cash NPAT was $4,907 million, an increase of 2 per cent on the prior comparative period. Return on equity (cash basis) was 16 per cent.

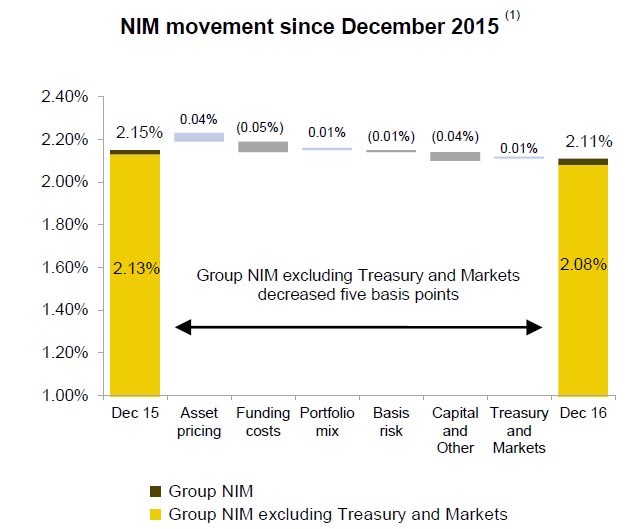

Strikingly though the net interest margin was down 4 basis points to 2.11%, or 2.08% excluding treasury, down 5 basis points.