Following the issue of the first 30 year bond by the Australian government in October last year, we asked whether the action symbolised a coming of age for the Australian bond market or a ringing of the bell to signal the end of a 30 year global bond market rally. It is likely that the issue did symbolise a coming of age for the domestic bond market, the significance of which should become more apparent as time goes by, but there is also mounting evidence that we were indeed hearing a bell being rung.

There were other momentous events around that time that pointed to the last hoorahs for a global bull market for bonds.

At the end of June last year there was US$11.7 trillion of negative yielding sovereign debt on issue around the world, according to Fitch Ratings. But since then bond yields have been trending upwards and by the end of December, Fitch reported negative yielding sovereign debt had reduced to US$9.1 trillion.

This is still a very large sum but a trend is becoming apparent.

In an environment of increasing negative yields on sovereign bonds Ireland and Belgium were able to sell 100 year bonds with coupons of just 2.35% and 2.3% per annum respectively, in the first half of 2016. And, in the same month that Australia issued its first 30 year bond, Italy was able to sell €5 billion of 50 year bonds with a coupon of 2.8% per annum, against an order book of €18.5 billion!

Both deals have since gone south.

The thirty year Australian government bonds sold by AOFM, had a face value of A$7.6 billion and were sold at a yield of 3.27% per annum. The bonds were trading in the secondary market at a yield of 3.79%, last week.

This means that investors, who bought the bonds at issue, are now nursing a 15% capital loss. Ouch!

Investors in the Italian 50 year bonds have not fared any better, and those that missed out on buying the bonds didn’t have to wait long to realise that they were in fact, the lucky ones. In less than a month after the sale, the bonds had lost 14% of their capital value in the secondary market, as investors began to fret about the outcome of the yet to be held referendum on constitutional change.

Investors feared political upheaval if the referendum was unsuccessful. It was unsuccessful and Italy’s then Prime Minister, Matteo Renzi, resigned, leaving a caretaker to run the government until elections can be called.

And in the meantime, the Italian government has had to grapple with a growing non-performing loan problem among Italy’s largest banks that threatens to evolve into a systemic crisis.

The 50 year Italian bonds were trading at just 81.5 cents in the euro last week, and a week earlier had been trading at 79.25 cents.

Thirty years, and indeed 100 years, is a long period of time and anything can happen before bonds with such terms to maturity come due to be repaid. But it is very unlikely that anyone who bought the bonds at issue will be there to collect when they mature, the bonds will have to be sold at some point and a capital gain or loss, will be realised.

In the short term, more capital losses appear assured for holders of the Australian and Italian government bonds in question. While the official cash rate in Australia may remain at 1.5% per annum throughout this year, the US economy appears to be picking up steam and US Federal Reserve Chairman, Janet Yellen, last week signalled that the next increase in the Fed Funds rate may be just a month away.

As a capital importing nation, bond yields will inevitably rise in Australia as yields increase in the US.

As for investors in the Irish and Belgian 100 year bonds, they face the same prospects.

Ireland and Belgium are price takers and not price makers, too. And then, there are all of the uncertainties that are confronting the eurozone.

Brexit needs to be negotiated and elections are looming in France, Germany and the Netherlands, in which right wing nationalist, anti-euro, parties may emerge victorious. Marine Le Pen, leader of the National Front in France, has already threatened to exit the euro and reintroduce the French franc.

And then, in 2018, a fourth bail-out of Greece will be due, and the prospect of Grexit will re-emerge, as the Greek Prime Minister, Alexi Tsipras, is already threatening. This assumes of course, that the European Union and the eurozone are still intact by then.

A moderating force on rising bond yields may be a surge in demand for German bunds and US government bonds.

This is why MB has an allocation away from duration in Aussie bonds. Phil is right that there are probably more losses ahead out the curve given it is the US bond market that drives these rates not the RBA. BofAML reckons another tantrum may be on the way:

Sowing the seeds of tantrum

• While Fed Chair Yellen revived the probability of a March hike, the market reaction was still disappointing. We await three remaining triggers (minutes, tax plan, payrolls) in the coming weeks before revisiting our bearish belly view.

• A historical comparison shows that that current divergence between real yields and risk assets (credit, VIX and equities) is unsustainable and sowing the seeds for the next taper tantrum. Three triggers left As we have repeatedly said, a string of strong data and balanced to hakwish Fed speak should revive March probabilities. While this happened to some extent this week, the fact that the market still assigns only a 25% probability after what has undoubtedly been much better than expected data is disappointing, to say the least. Our bearish views (short the 5y point, short real rates and bear flatteners) remain contingent on triggers by early March:

1) the minutes next week, which could offer a better clue if March is alive;

2) President Trump’s fiscal plan, which is likely due before February 28;

3) the February payroll report on March 10.

If these triggers fail to reignite the belly-cheapening trade, this would be reason to rethink our views. After March, headlines are likely to be dominated by the European election cycle and Congress going back and forth on the tax plan – both primed with room for disappointment and offering little reason to hold on to negative carry trades.

The next tantrum

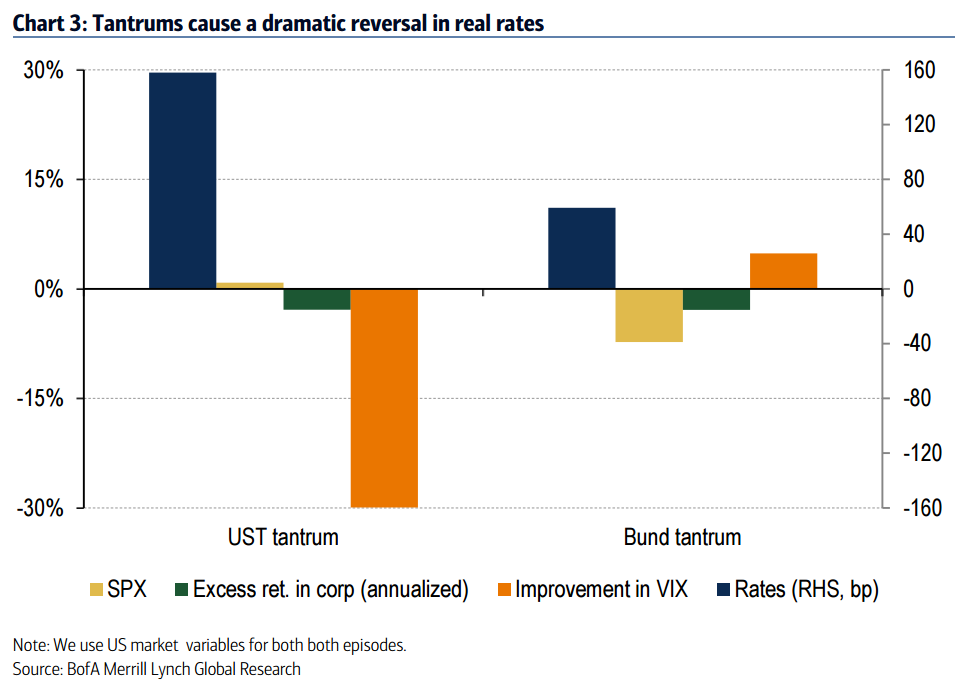

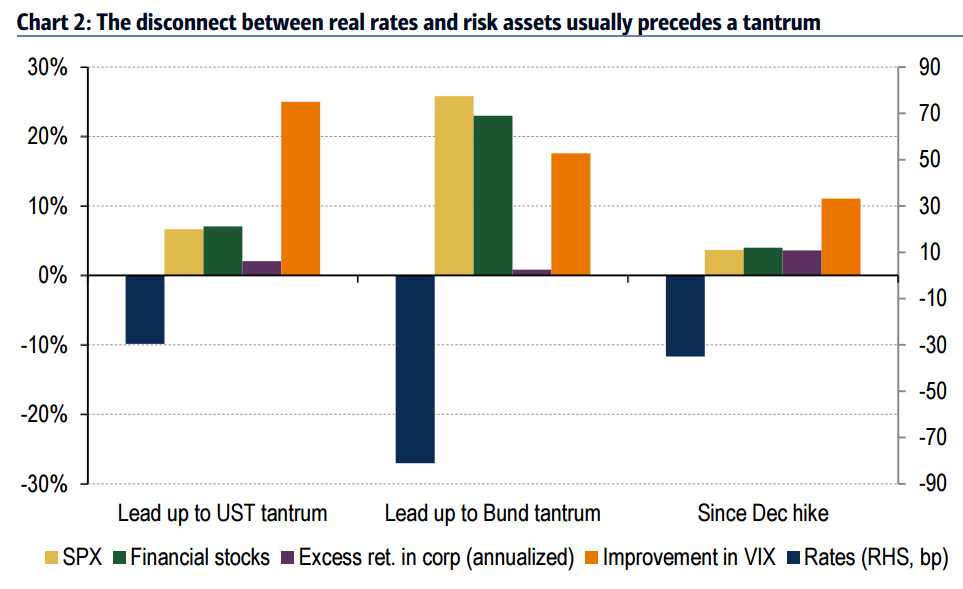

Tactical considerations aside, history offers a compelling reason to be cautious on duration after recent market moves. We look at the divergence between real rates and a combination of risk assets – equities, financial stocks, credit spreads and VIX, three months into and after the prior tantrum episodes. There is no doubt that low real rates help fuel risk assets higher, feeding this disconnect. But at some point, it becomes wide enough to trigger a real rate catch-up (Chart 2 and Chart 3).

• Leading up to the US tantrum: In 2013, real rates were richer by 30bp despite equities and financials being up by 7%, the VIX declining by 25% and annualized excess return in credit exceeding 2%. The following three months brought the taper tantrum where real rates shot higher by 160bp.

• Into the bund tantrum: In the 2015 lead-up to the Bund tantrum, the disconnect was wider – real rates were lower by 80bp and equities higher by 25% before the catch-up happened. The following three months saw nearly a 60bp rise in real rates.

• Since the December Fed hike: Real rates are richer by 30bp, equities are up 4%, financials by 4%, VIX is lower by 11% and annualized excess return in credit exceed 3% – a similar cocktail to the months leading up to the US tantrum, while still somewhat away from the divergence in the Bund tantrum.

Either way, the message is compelling. A wide enough disconnect between real rates and risk assets is usually a precursor to an ugly sell-off in duration and urges caution, specifically on real rates.

The alternative scenario is a selloff in risk assets. Everything is awfully hot right now.

Advertisement

Anyways, this is why MB is only buying dips in short end Aussie bonds. We expect further curve steepening yet, fast or slow, as the Fed tightens and RBA loosens. The other interesting point of note is that so long as it persists, the bank are going to be bought.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.