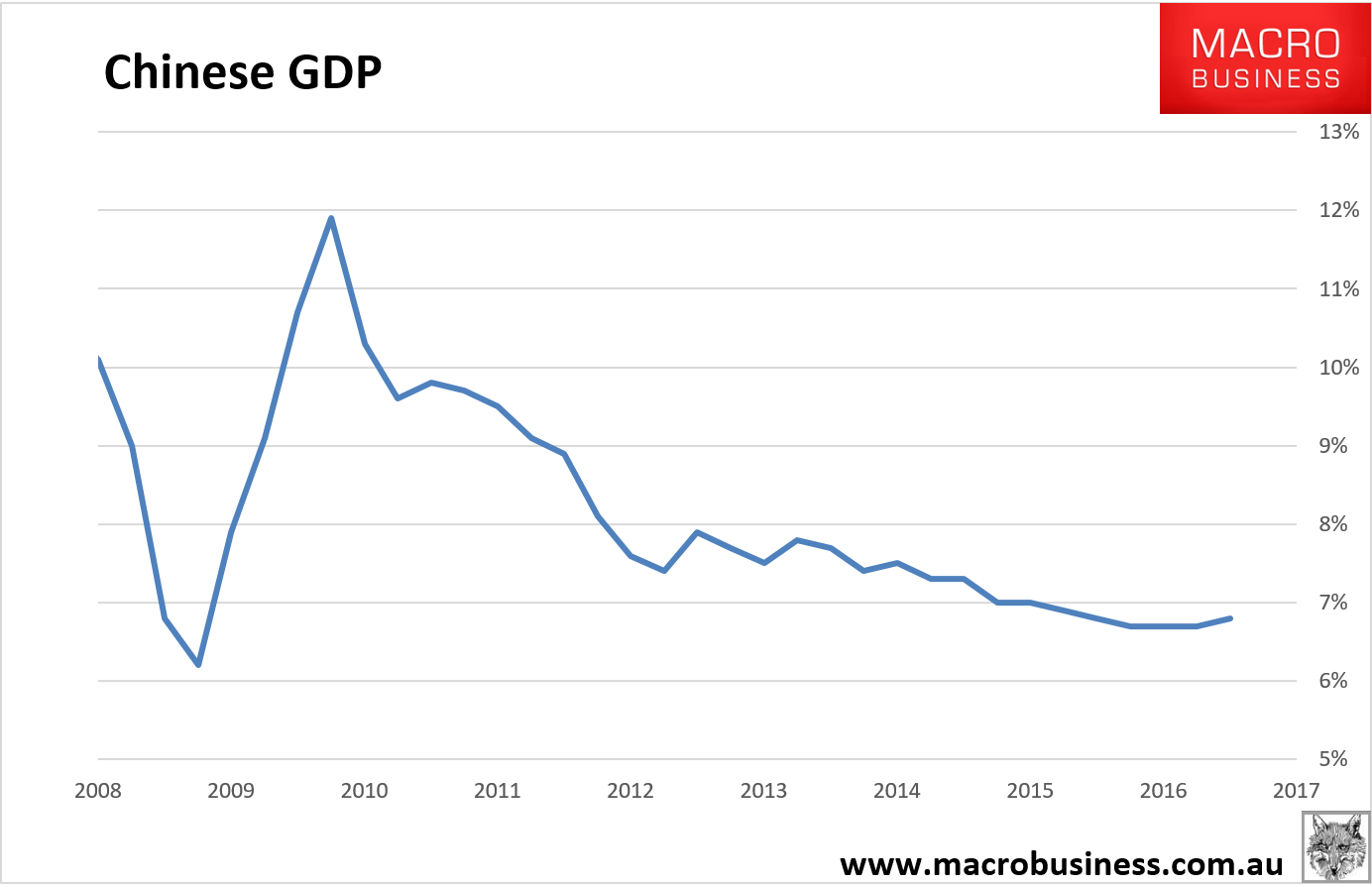

Here is an updated summary of Chinese data as we enter 2017 proper. China ended the year strongly with GDP at 6.8%:

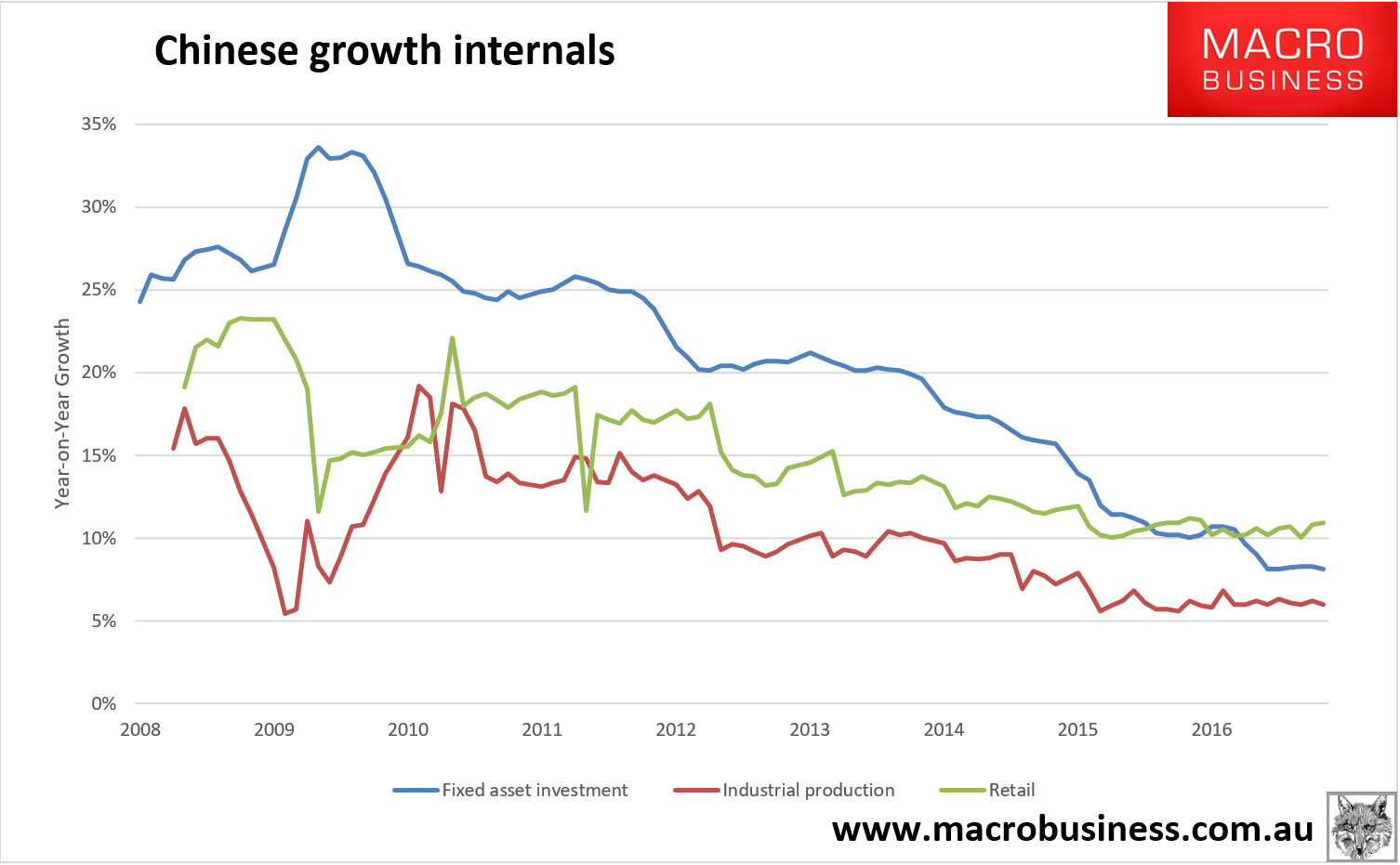

Growth internals were solid with retail sales at 10.9%, industrial production at 6% and fixed asset investment at 8.1%. There was a hint of softening in the latter two:

Advertisement

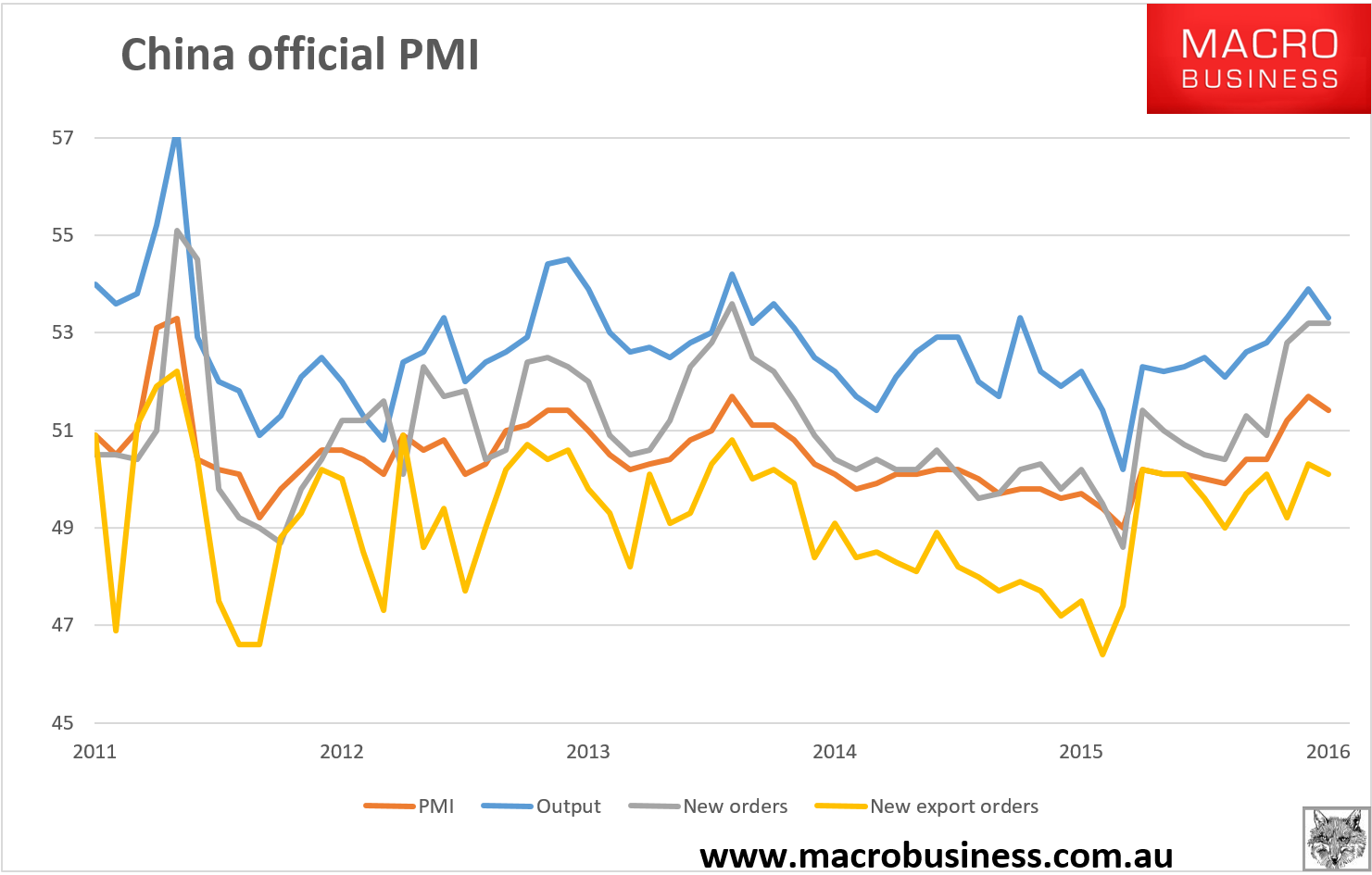

The manufacturing PMI also showed slowing down to 51.4 and new orders also off a little:

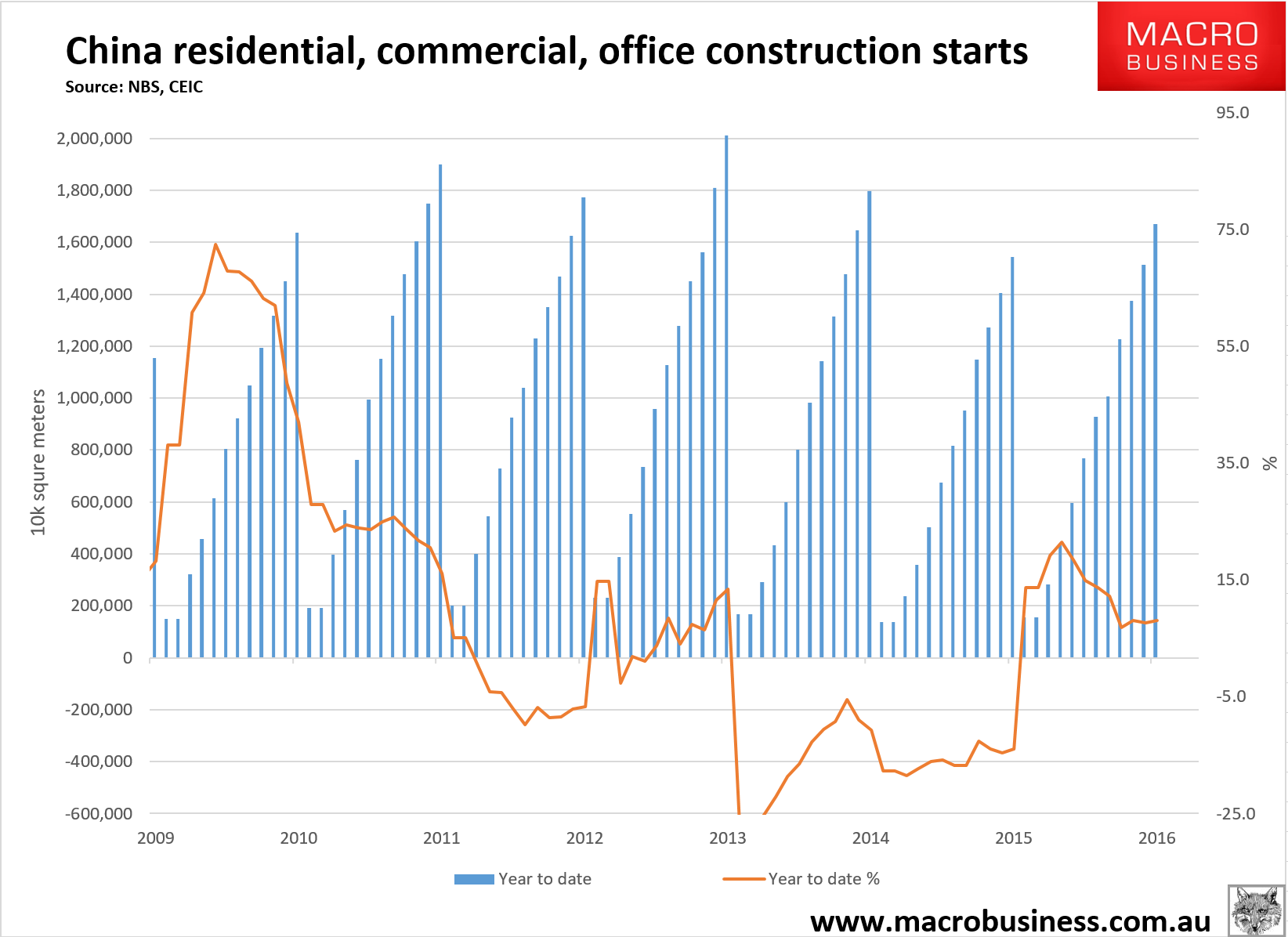

Digging a little further into leading growth drivers, real estate was holding up with new starts up 8.1% year to date, though they are down year on year for several months now:

Advertisement

That is likely to continue. Year on year comparisons will get more difficult in the next few months as the base effect from last year’s rebound kicks in. Starts should begin falling in H1.

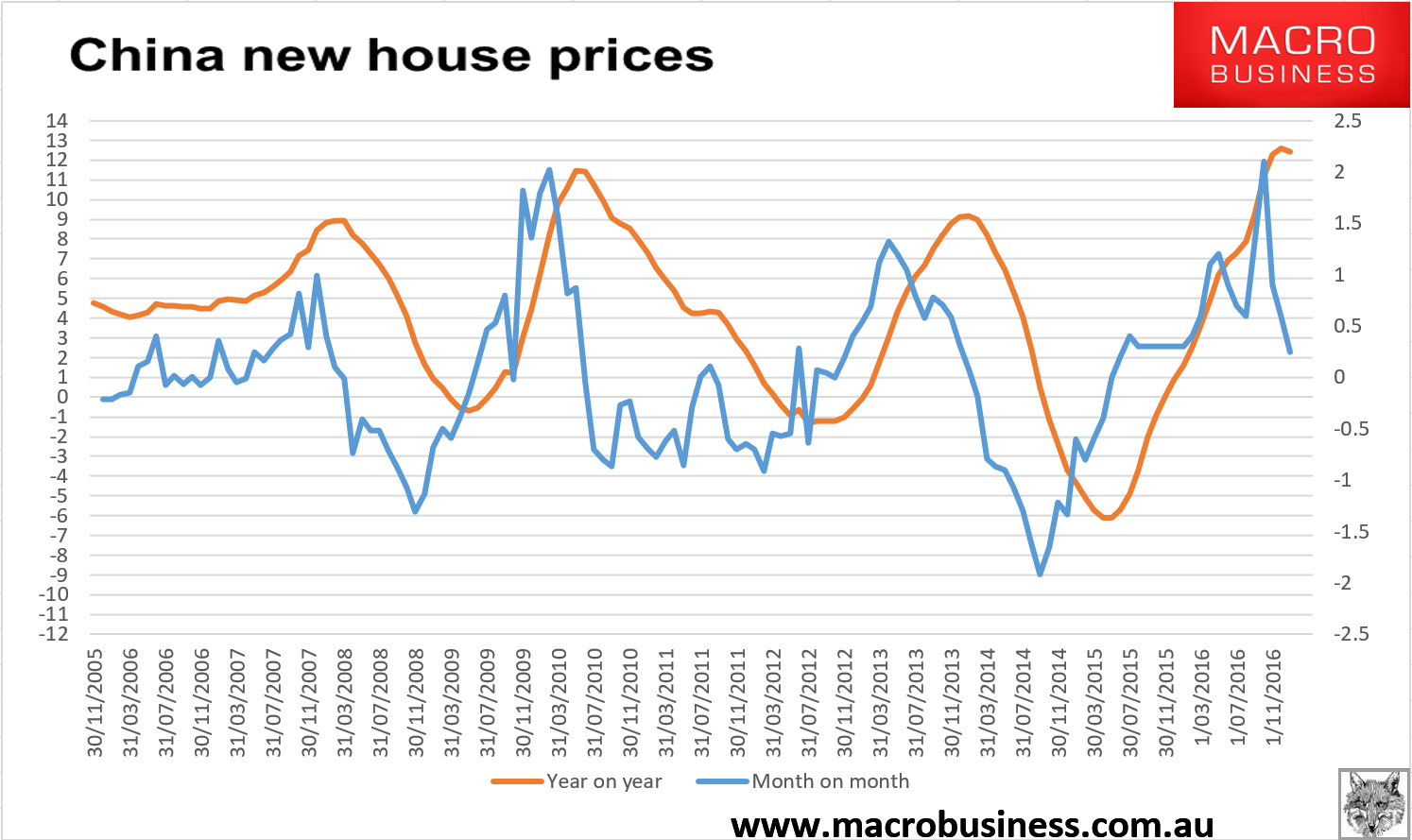

Moreover, house prices have peaked and are slowing swiftly with month on month growth slipping towards zero:

Advertisement

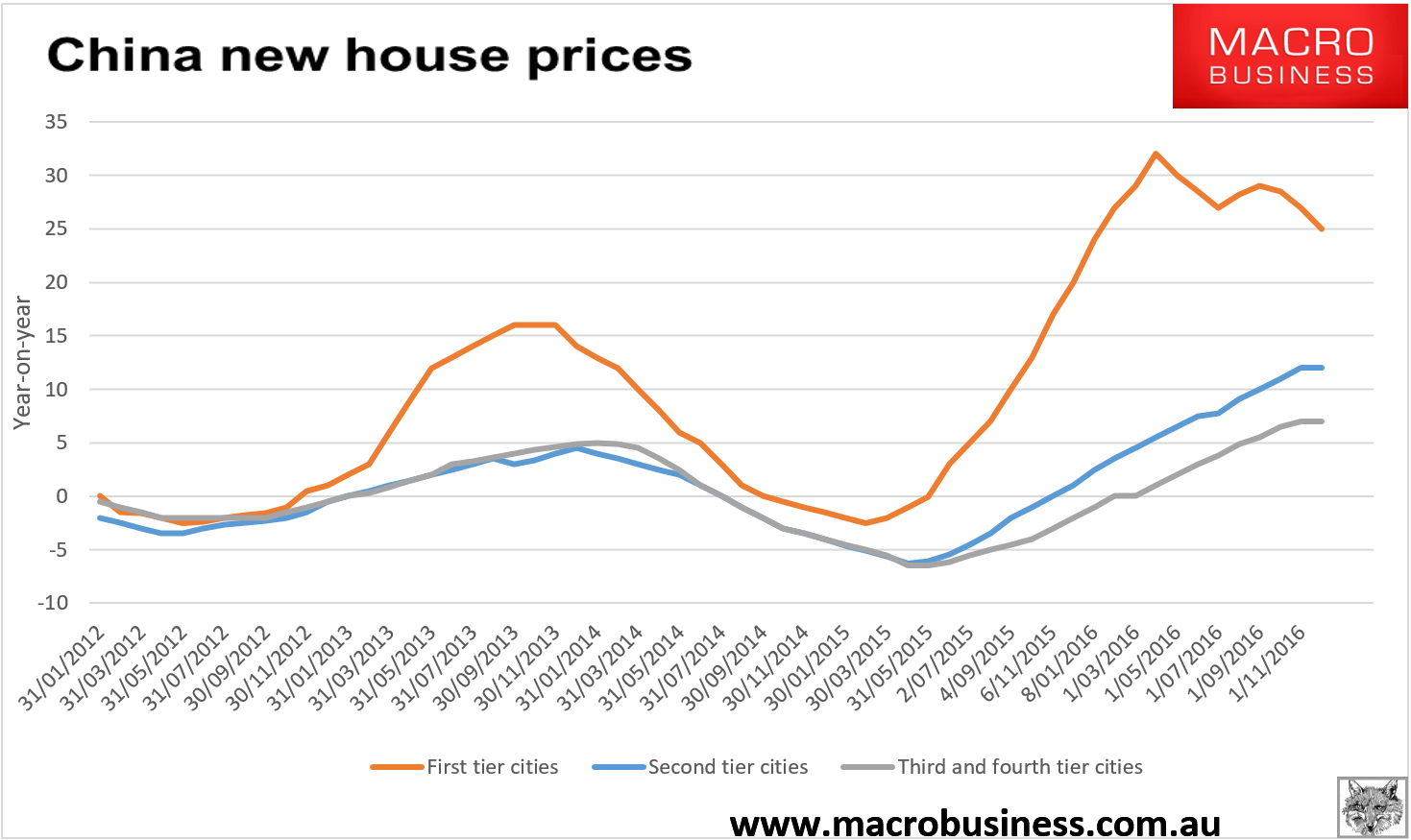

The top tier city boom is over and year on year prices have a long way to slide back:

Advertisement

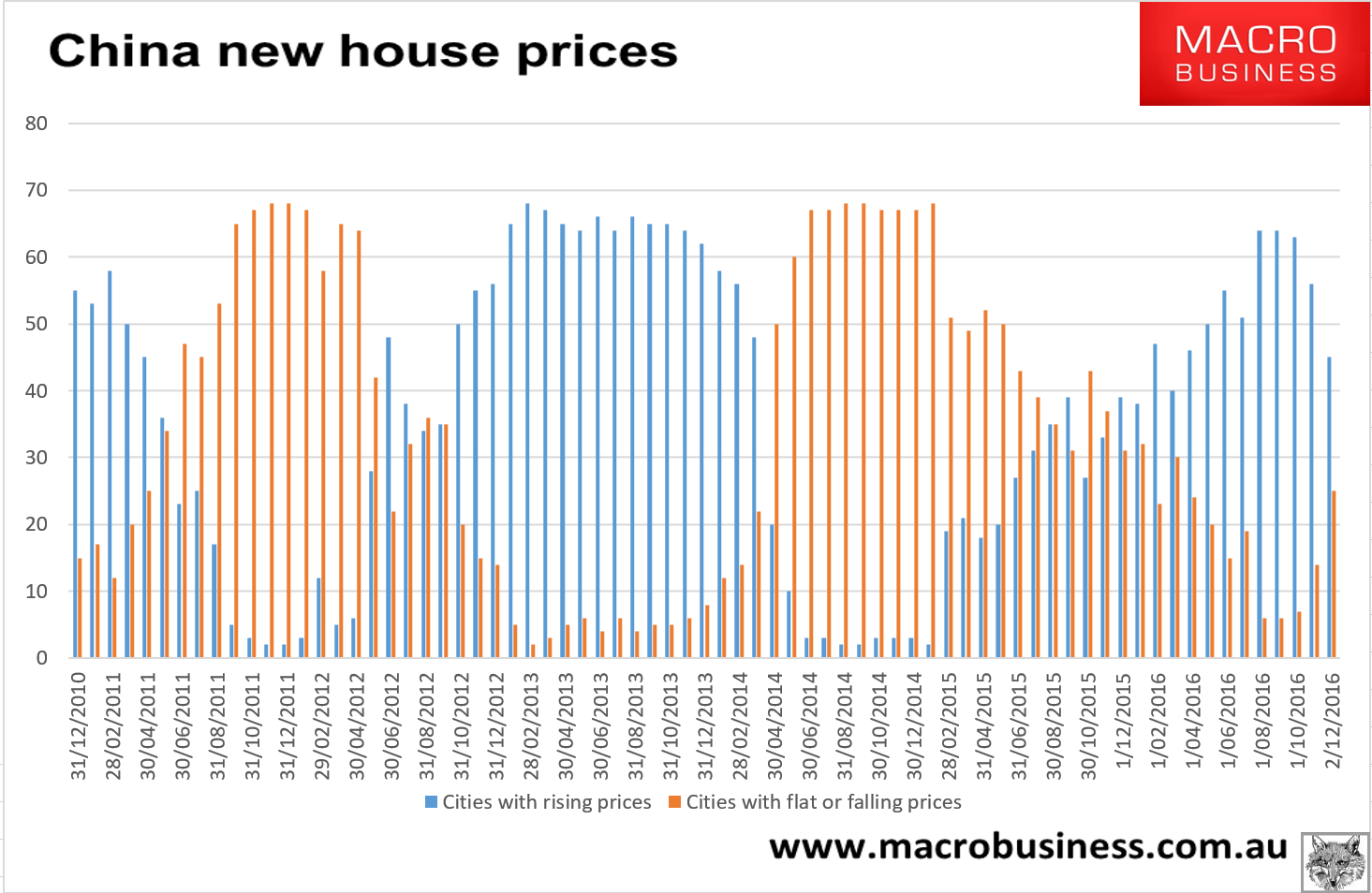

As the breadth of price falls begins to rise on prudential tightening:

The key question now is how much will the top tier house price slowdown filter into lower tier cities. My guess is more than authorities would like. Some form of “shrinkflation” seems a decent bet for Chinese property this year as top tier cities do not bust but the overall market stagnates.

Advertisement

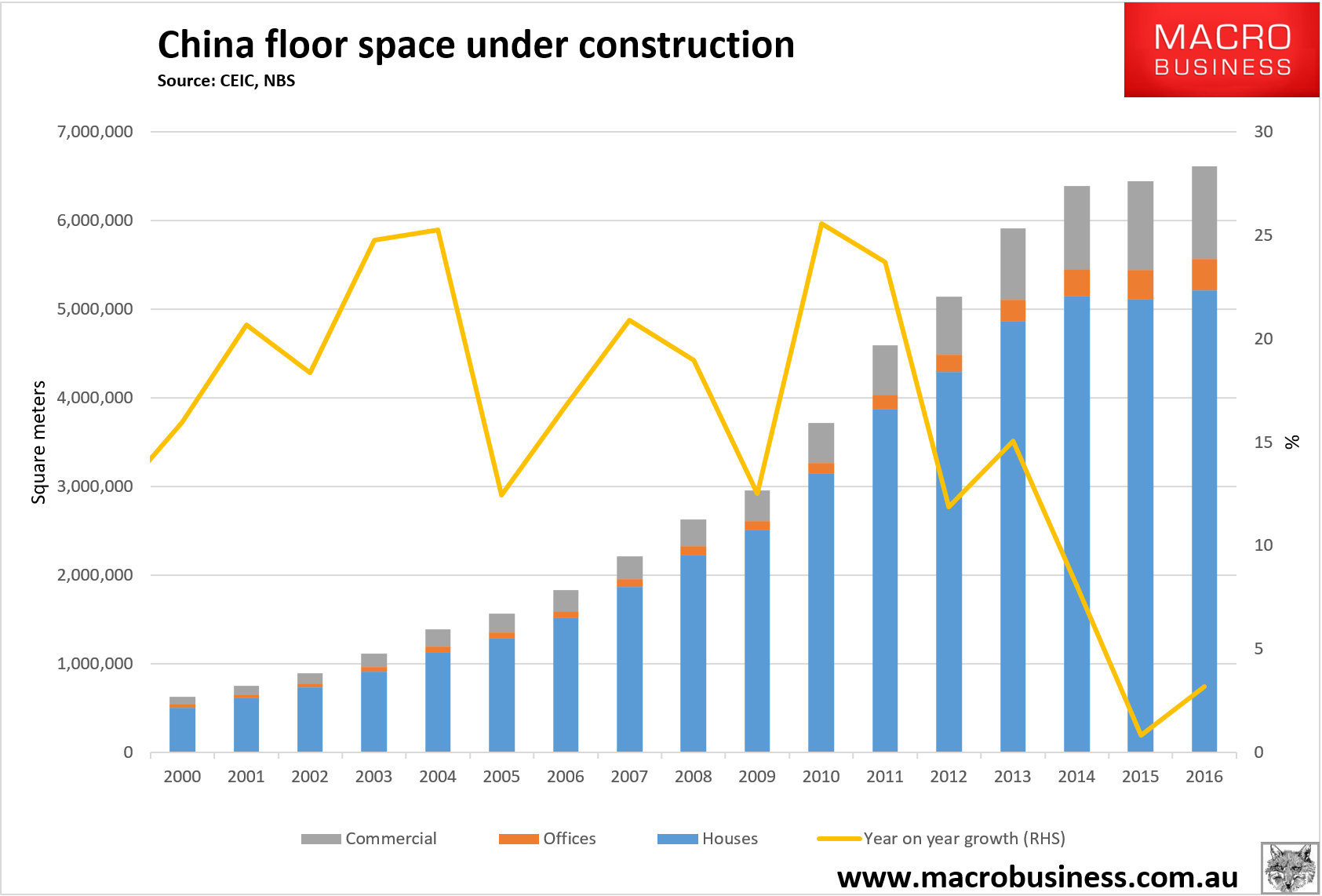

That will leave construction peaking in H1 and declining in H2. Overall floor space under construction should end the year with modest falls from its current 3.2% 2016 growth rate:

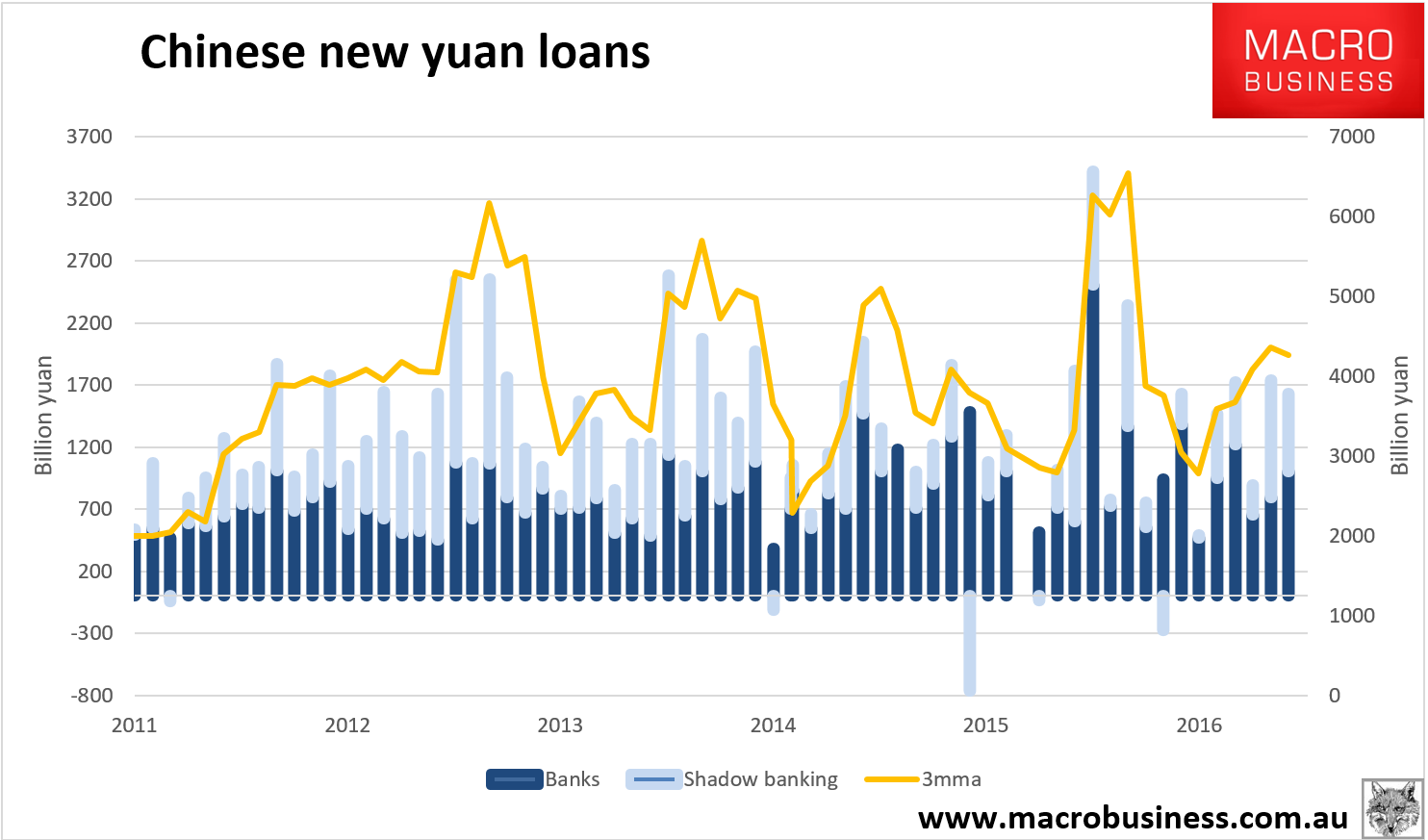

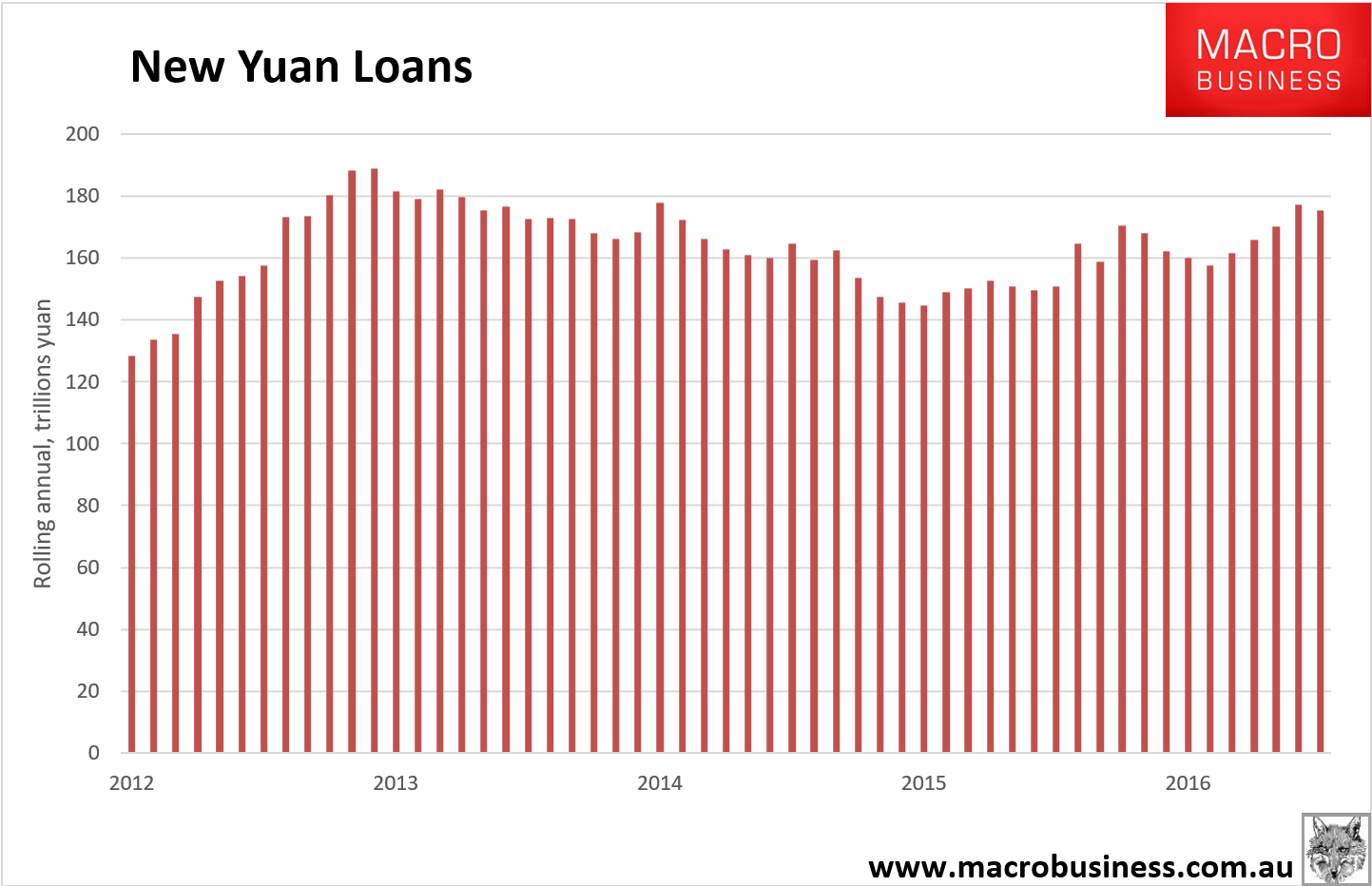

Another leading indicator showing incipient softening is credit where we find year on year comparisons already beginning to bite. December credit was firm at 1.63tr yuan new yuan loans:

Advertisement

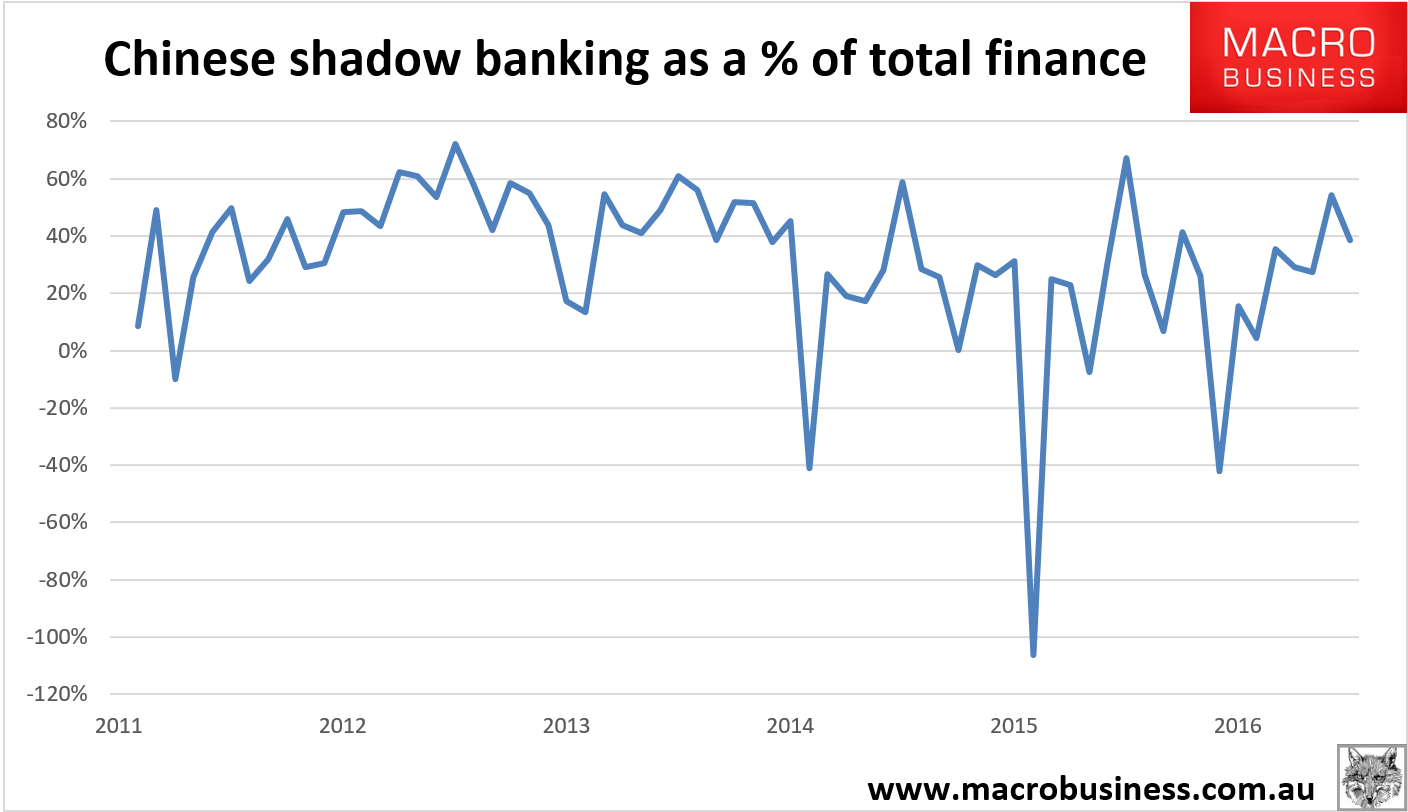

And shadow credit is still off the hook:

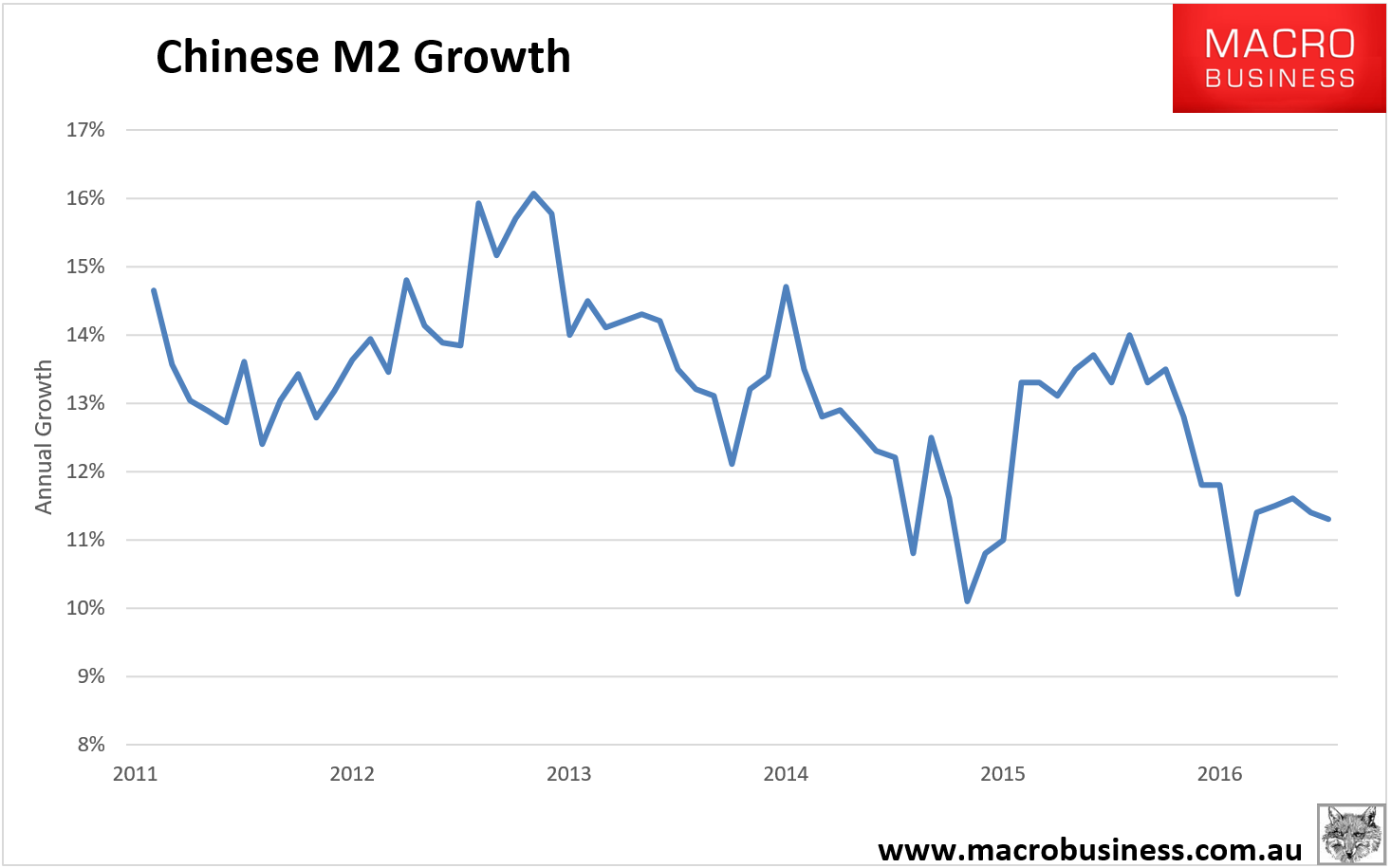

But M2 is fading:

Advertisement

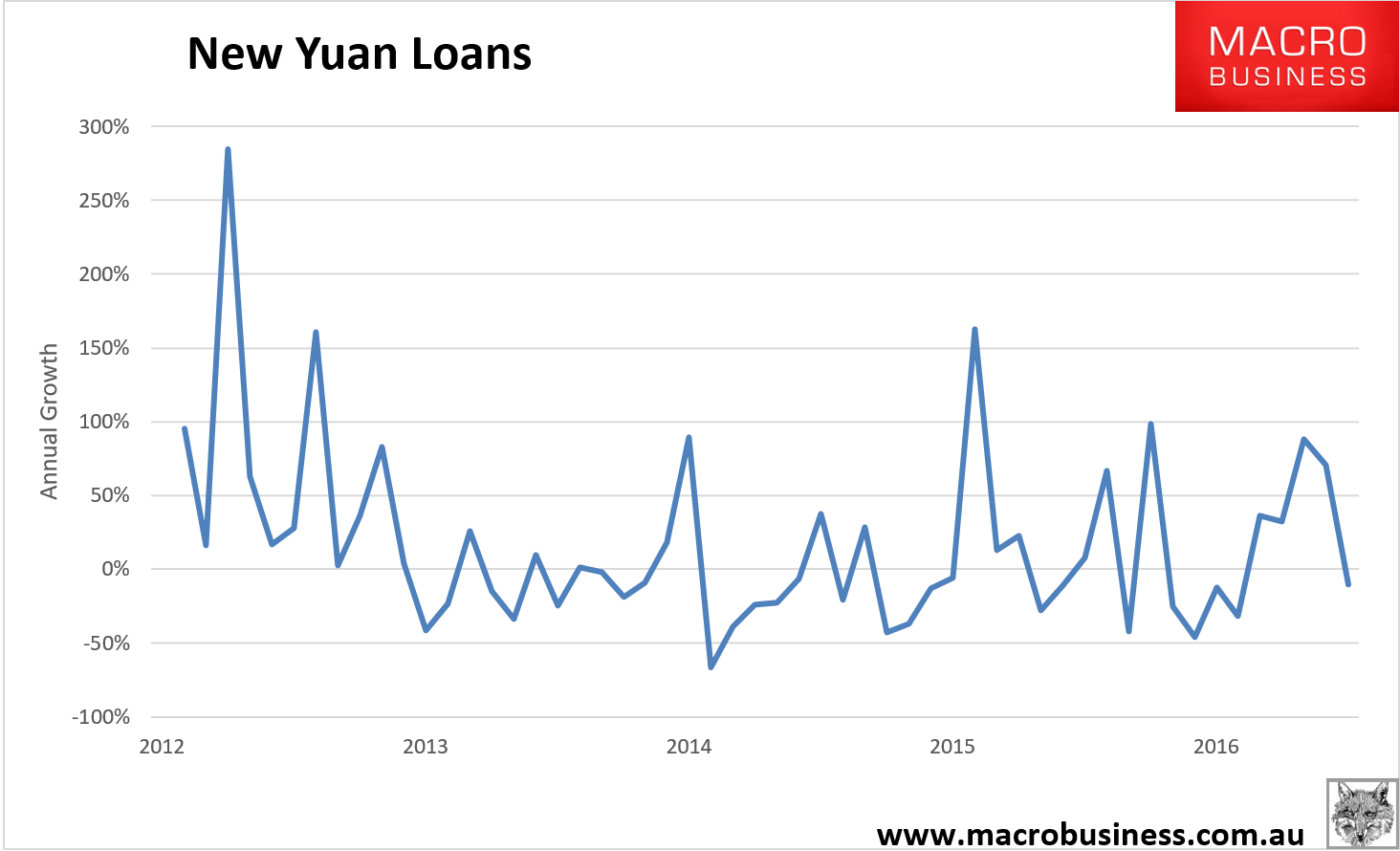

And year over year new loans are now falling as last year’s stimulus lifts the base:

And rolling annual has rolled:

Advertisement

Plus, the new housing sector prudential measures are yet to fully materialise in the data. Credit will slow further year over year in H1.

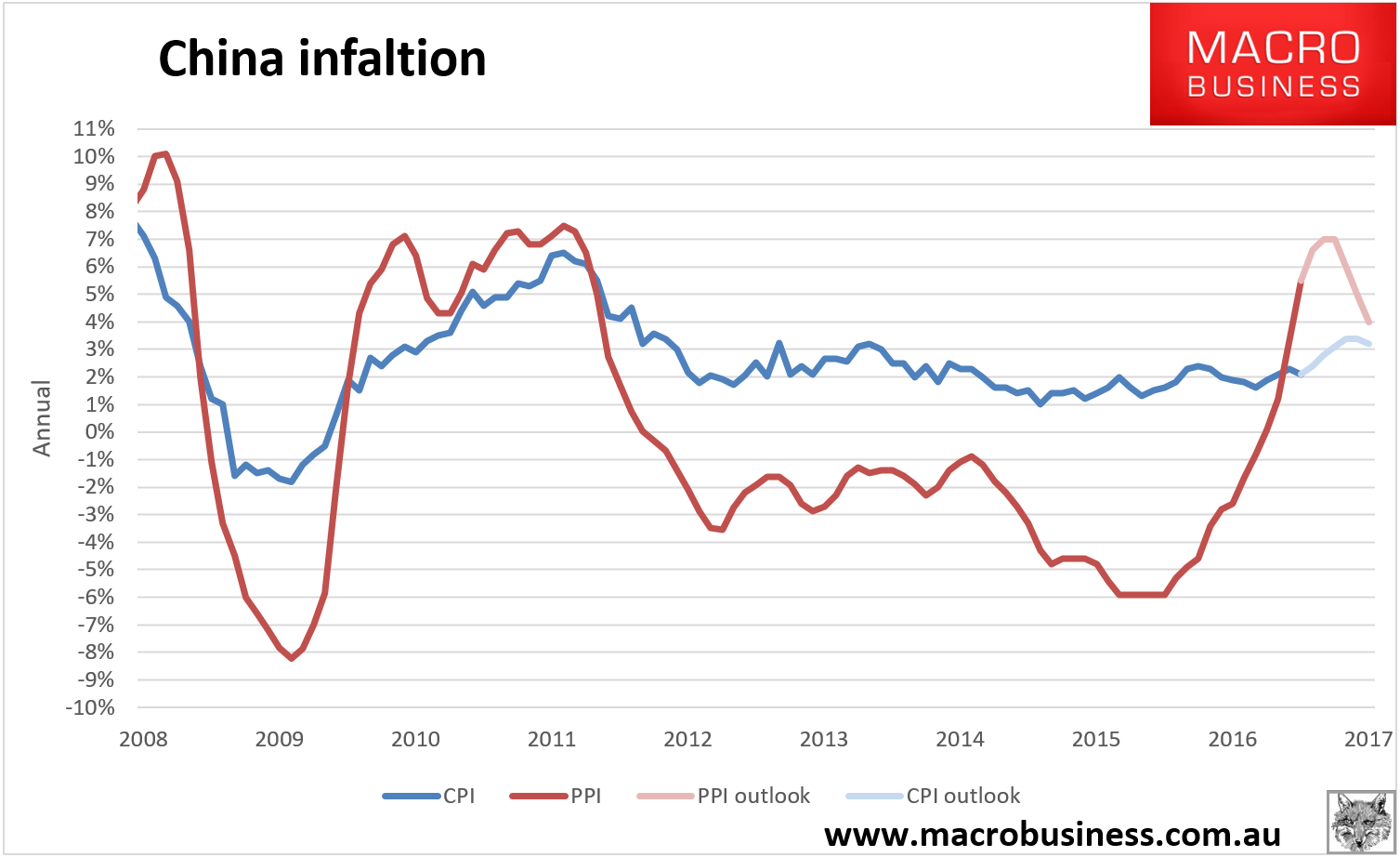

Although opting for prudential tools over rising interest rates (which shows a real willingness to let the yuan fall), authorities are moving so quickly to tighten because the stimulus has generated a large inflation pulse. December producer inflation was even worse than my bearish outlook at 5.5%. It’s yet to filer through to CPI but based upon the past relationship it will and soon:

Advertisement

As well, patience with credit-fueled growth cycles is clearly much lower than it was yesteryear. UBS has more on how close China is to its debt peaks:

China’s debt is set to rise further in the coming years, likely exceeding 300% of GDP within 2 years. As the government continues to rely on credit-fuelled investment growth to offset downward pressures within the domestic economy and from a subdued global environment, unless there is major debt restructuring, China’s debt/GDP ratio is set to rise further. We don’t think that there is a “magic” level at which a debt crisis will take place. Many countries ran into debt crises at levels of debt significantly lower than China’s current level, often because debt was financed by foreign resources due to low domestic savings, and/or because of duration mismatch (Figure 11).

Conversely, there are countries (e.g. Japan, Figure 2) where debt levels have risen ever higher without triggering any obvious financial sector distress.

Four factors make a typical systemic debt crisis unlikely for China. Typical debt crises are often liquidity crises of the financial system. In China,

1) over 95% of debt is domestic debt financed mainly via banks;

2) there is a very high domestic savings & under-developed capital markets, so saving largely exists as deposits or quasi-deposits in the banking system to finance debt (Figure 12);

3) capital controls still exist to keep liquidity at home; and

4) a high degree of government control over the financial sector and largest borrowers (SOEs) means that debt restructuring can take place gradually with government coordination rather than in a disorderly manner forced by the market. A central bank that always stands ready also helps to shore up depositor confidence in the banking system, helping to reduce the risk of liquidity events. This is why we still think that China’s credit cycle may be a more drawn out process than one that is disrupted by a typical liquidity-related debt crisis.

The fact that debt is rising much faster than output year after year and an increasing share of debt is allocated in nonproductive or excess capacity sectors means misallocation of resources. Such systematic misallocation will depress long term productivity and economic growth, and wasted resources mean more potential bad debt will be created. While the aforementioned unique factors can allow China’s credit cycle to last much longer than in other economies and with less volatility, this lack of a market-clearing mechanism could depress corporate profitability and investment, leading to lower or stagnant economic growth over a prolonged period of time. Eventually, the cost of accumulating so much bad debt will have to be borne by the financial sector and savers, asset prices will have to correct, and the ultimate cost of adjustment may be substantially larger.

In the likely scenario that China’s debt cycle is a drawn out process, the government would have to balance the need to stabilize growth and defuse debt problems by slowing credit expansion gradually, taking actions to gradually restructure the stock of debt (including by writing off bad debts, divesting some state assets and closing down “zombie” companies), and reform to encourage growth in less debt-dependent sectors. In any large credit event, banks and related financial institutions would likely be required by the government to bring some of the culprit debt on to their balance sheets, to gradually restructure its underlying assets to help the economy avoid a serious liquidity/credit crunch. If confidence in shadow bank channels drops, so long as the government retains control over the capital account, liquidity would most likely flow back to the banking system

Risk of a more disruptive break in the credit cycle has risen in recent years. The credit cycle could be more easily disrupted if 1) banks run out of “free” liquidity and have to rely on wholesale funding to finance balance sheet expansion, which provides less reliable funding. Banks may be forced to slow credit expansion sharply in the event of a market confidence collapse or asset price plunge; and 2) Large capital outflows persist for a prolonged period, with the resultant domestic liquidity tightening increasing banks’ exposure to international market conditions. Indeed China is experiencing rising capital outflows as a result of the government’s earlier push for capital account opening and the more recent weakening of market confidence (Figure 13).

The rapid shadow credit expansion is a risk. Shadow credit is less regulated and adds multiple layers of intermediation that increases risks and financing costs. More importantly, when multiple layers of shadow credit underpins the economy’s overall funding structure, it becomes much harder for the government to quickly identify where funding problems may be or as they appear, compromising their ability to promptly oversee and manage any liquidity situation to prevent it from warping into a bigger systemic issue. As shadow credit becomes increasingly important, the government’s ability to use banks to bailout the shadow banking sector will also be diminished.

That is a sensible view. It’s going to be a long struggle between debt and reform in China. 2017 will be a year when the latter slowly resumes control and growth slows once more. The 6.5% growth target is reasonable for H1. By year end I’ll be looking for a return to 5-handle quarters.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.