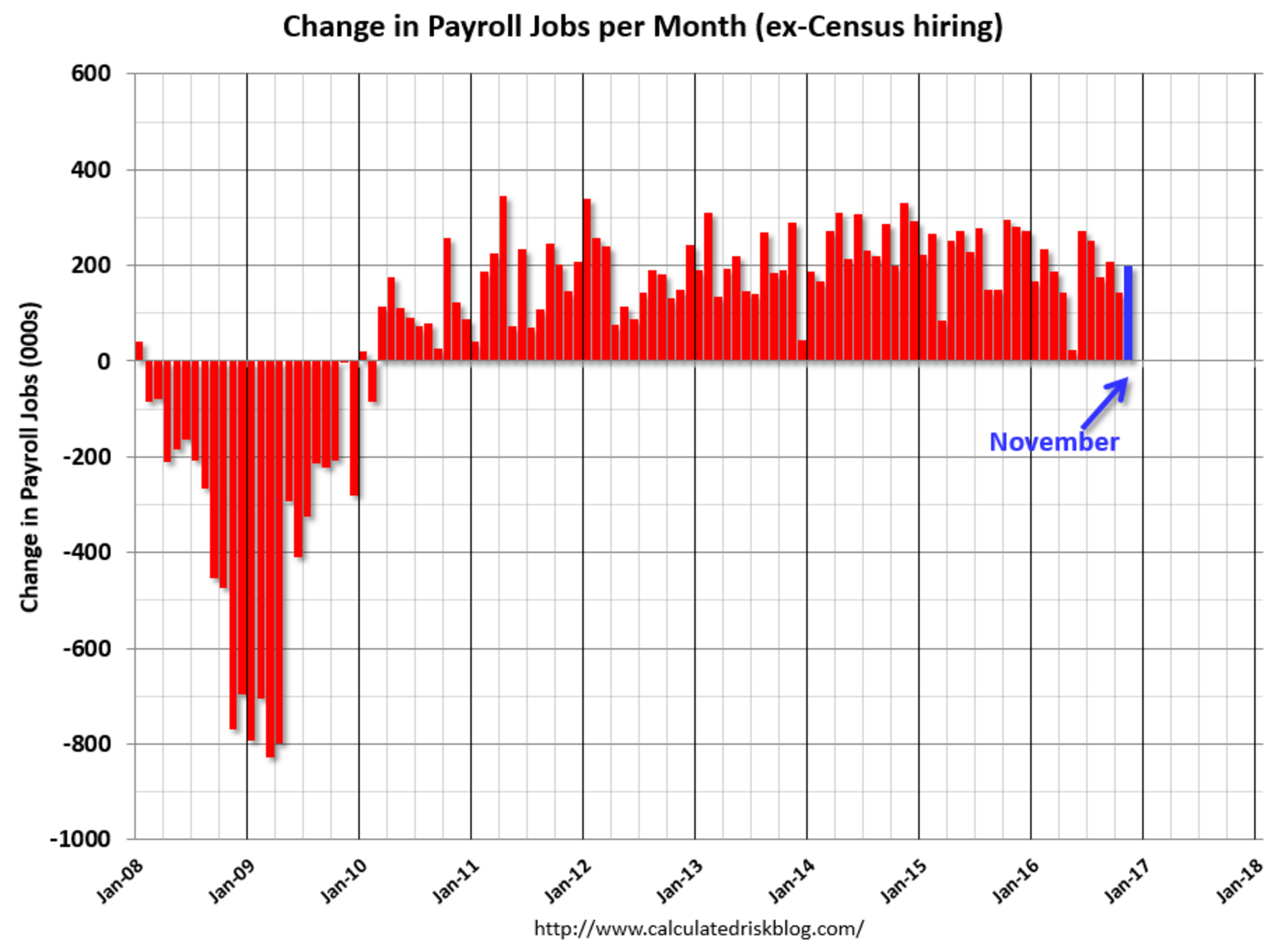

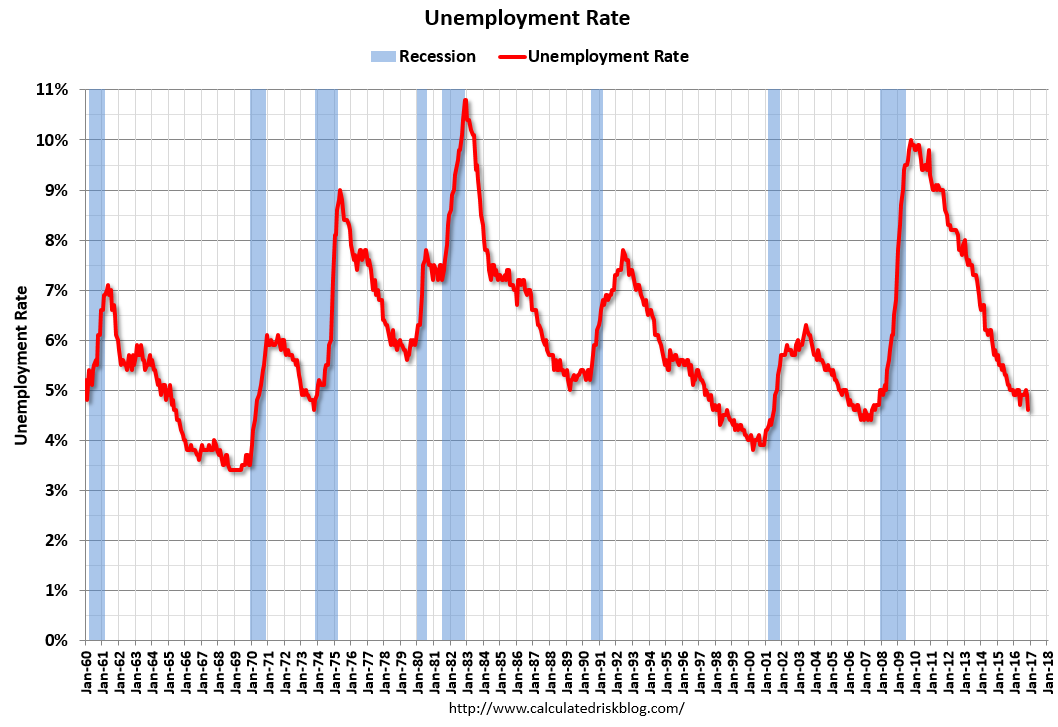

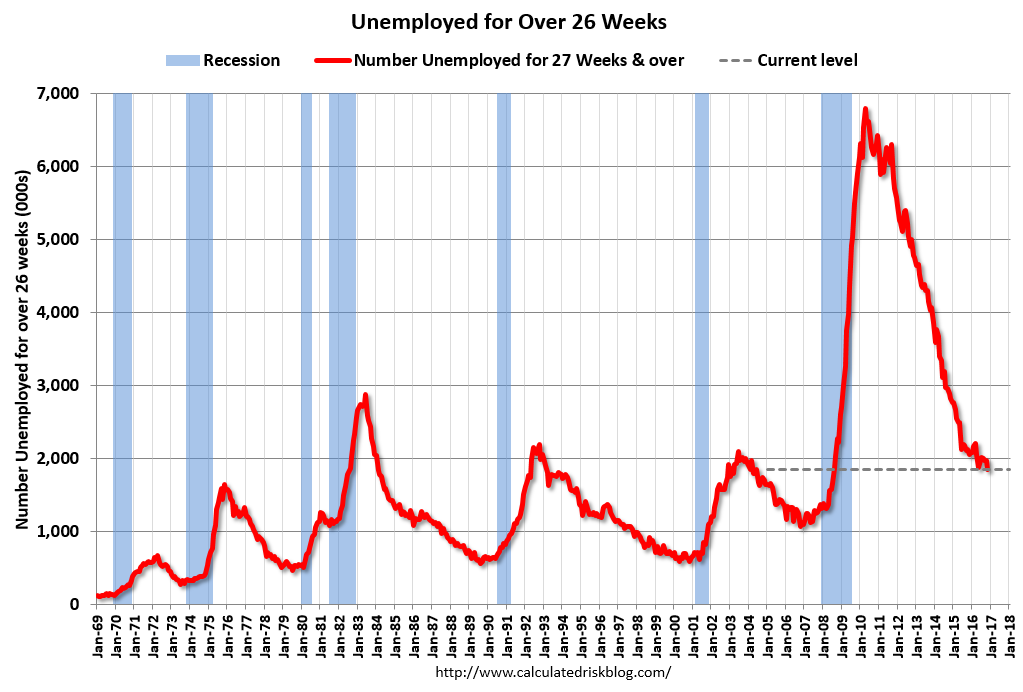

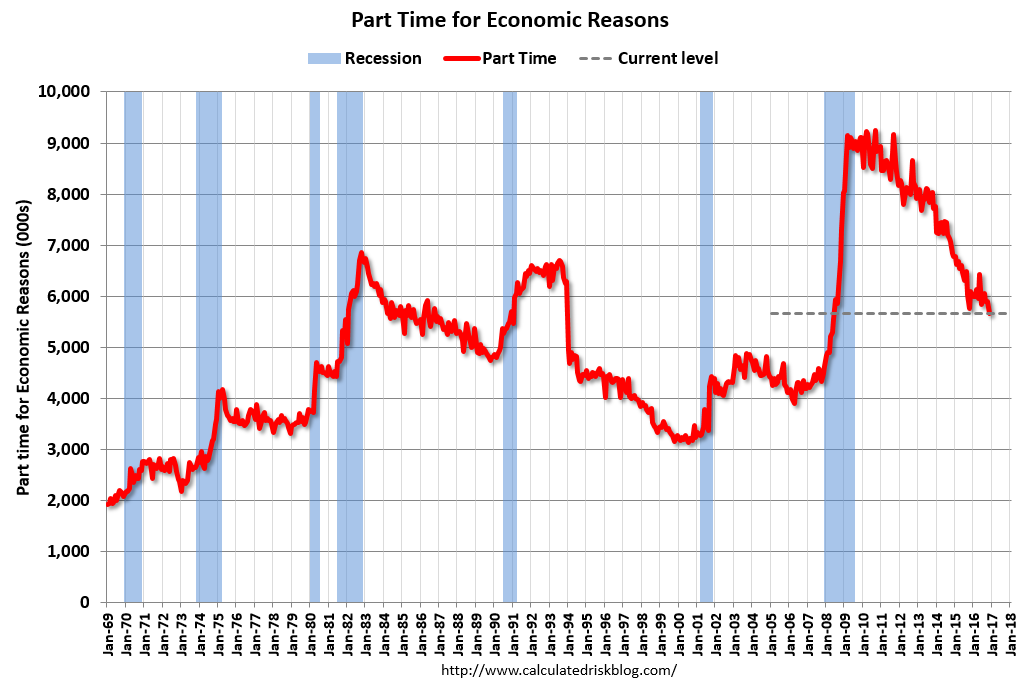

The unemployment rate declined to 4.6 percent in November, and total nonfarm payroll employment increased by 178,000, the U.S. Bureau of Labor Statistics reported today. Employment gains occurred in professional and business services and in health care.

… The change in total nonfarm payroll employment for September was revised up from +191,000 to +208,000, and the change for October was revised down from +161,000 to +142,000. With these revisions, employment gains in September and October combined were 2,000 less than previously reported. Over the past 3 months, job gains have averaged 176,000 per month.

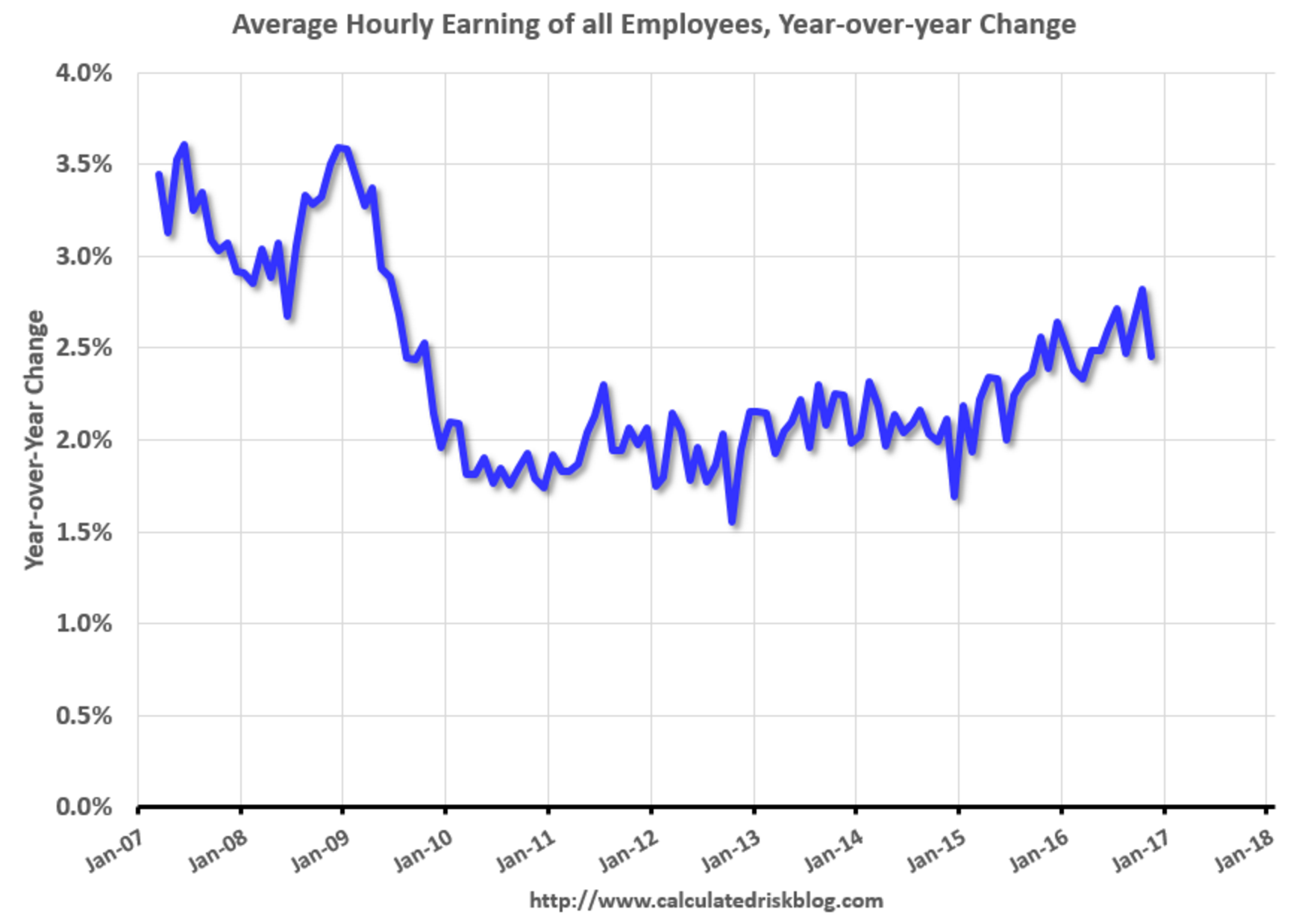

…In November, average hourly earnings for all employees on private nonfarm payrolls declined by 3 cents to $25.89, following an 11-cent increase in October. Over the year, average hourly earnings have risen by 2.5 percent. Average hourly earnings of private- sector production and nonsupervisory employees edged up by 2 cents to $21.73 in November.

Which is why income gains are still only rising slowly (with a big pull back in this report):

Some relief for the Fed trajectory of rate hikes there. Needless to say, the USD pulled back and other majors rebounded:

Advertisement

Commodity currencies mostly rose:

Gold rebounded a little:

Advertisement

Brent carried on:

Base metals were mixed:

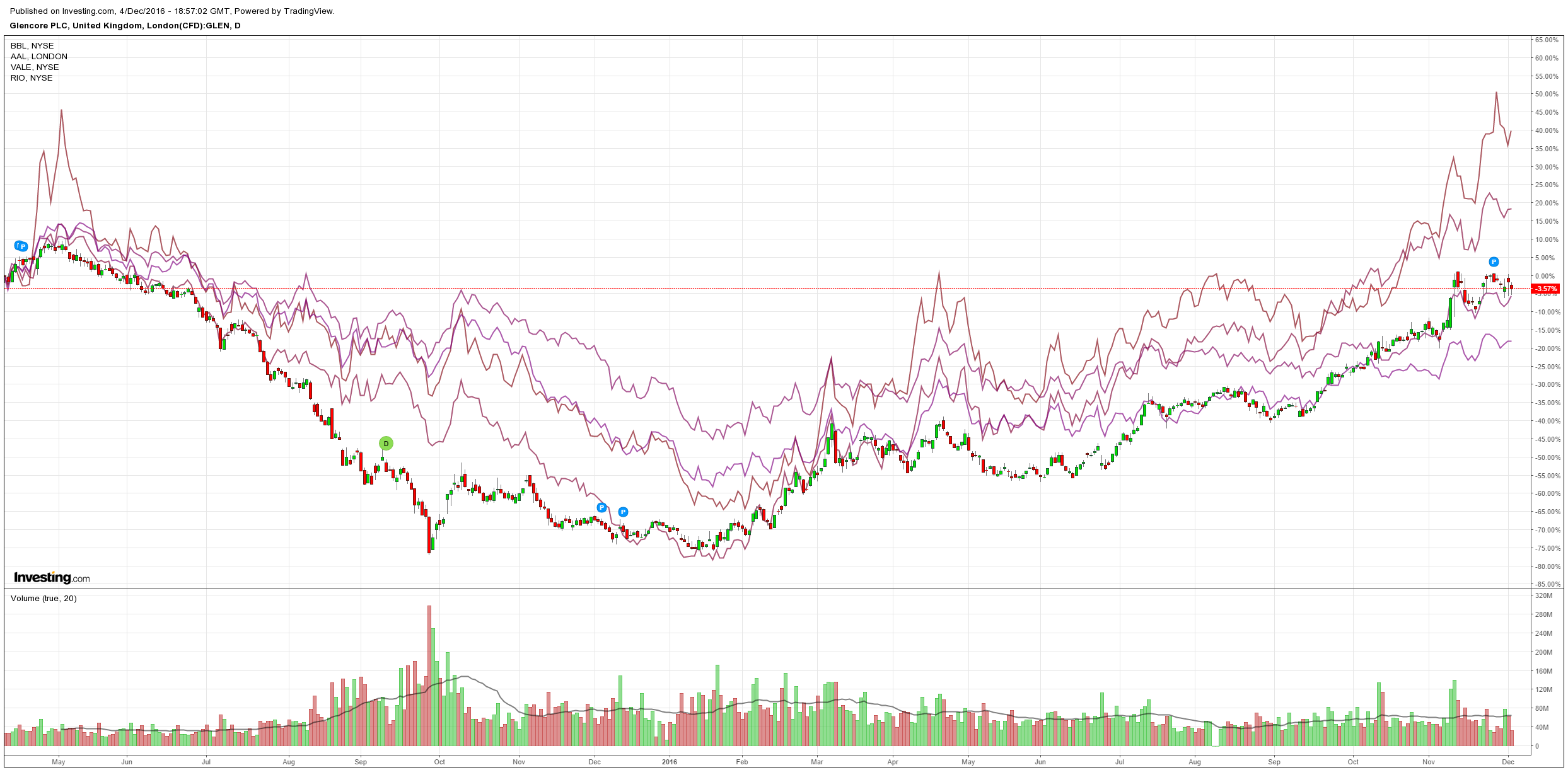

And miners:

Advertisement

US high yield bounced with oil but EM kept sinking. I expect this split to continue:

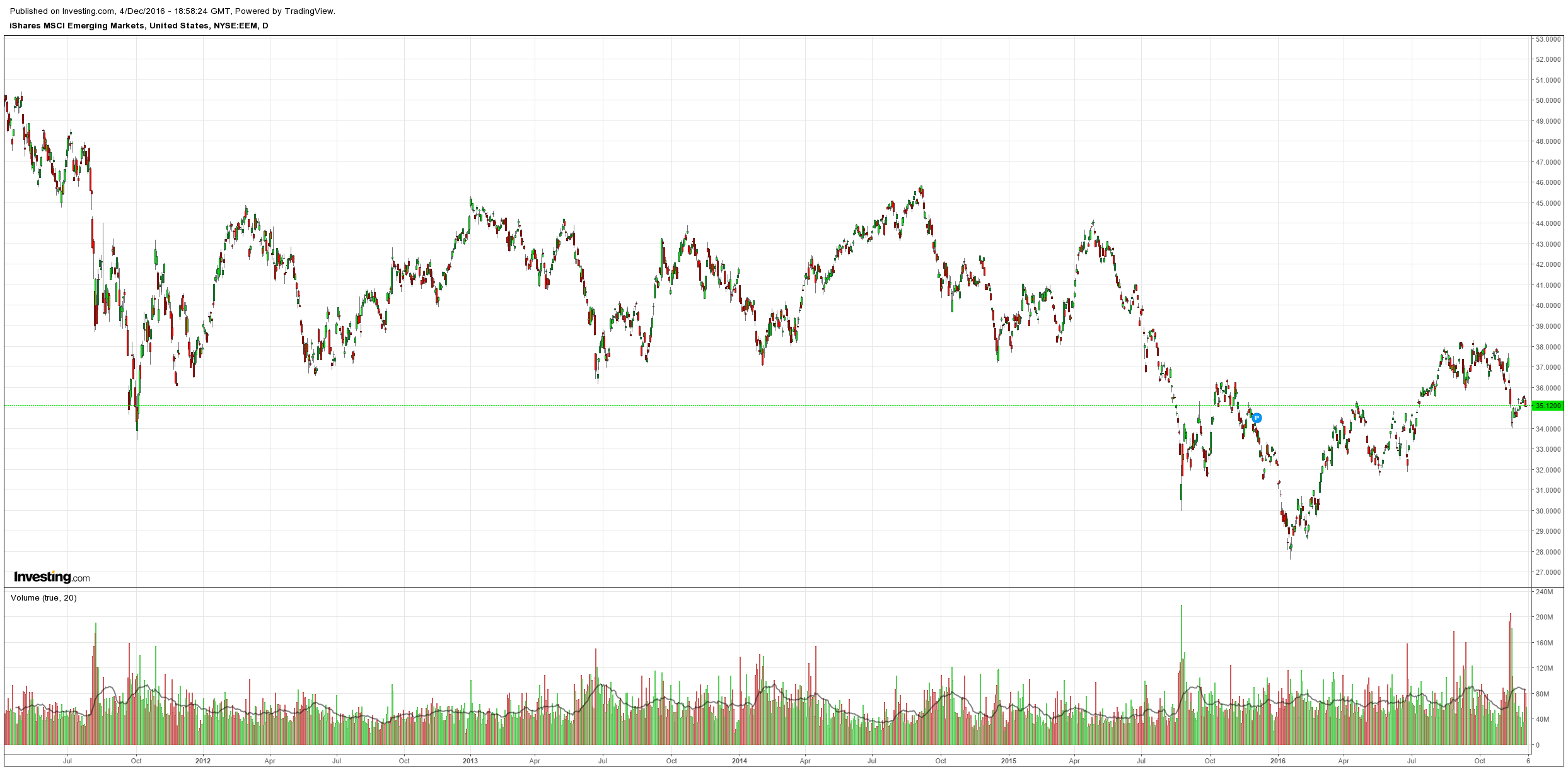

EM stocks fell:

Advertisement

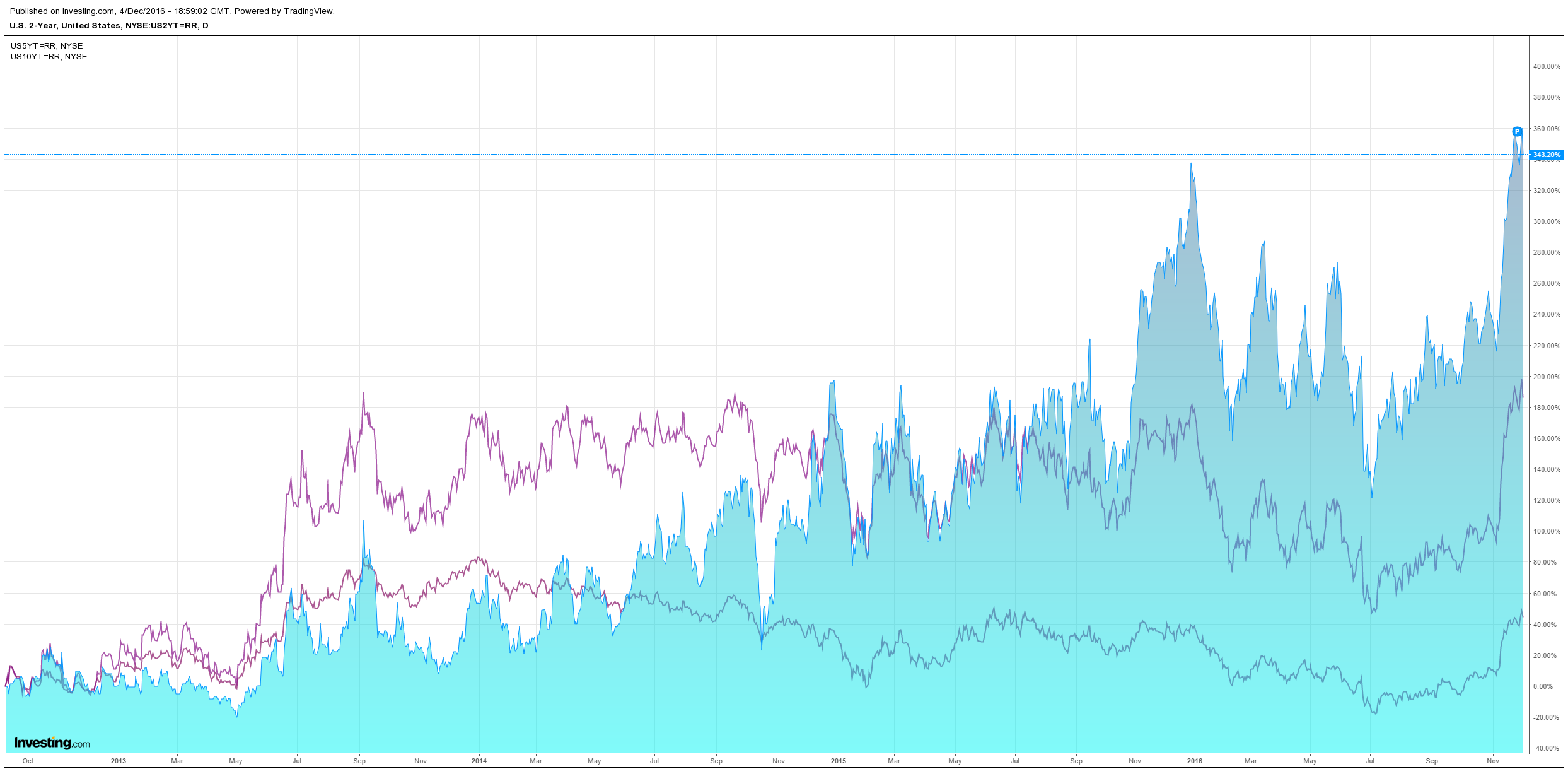

US bonds were bid:

And stocks struggled:

All in all, a chance for the global inflation trade to consolidate. The FT’s Gavyn Davies has more on that:

Advertisement

A year ago, there was a pervasive mood of gloom among economists and investors about prospects for the global economy in 2016. China was in the doldrums, and fears of a sharp renminbi devaluation were rife. The oil shock had caused major reductions in capital spending in the energy sector, and consumers seemed reluctant to spend the large gains they were enjoying in real household incomes.

Deflation risks dominated the bond markets in Japan and the Eurozone. In the US, the Federal Reserve seemed determined to “normalise” interest rates, despite the rising dollar and the weakness in foreign economies.

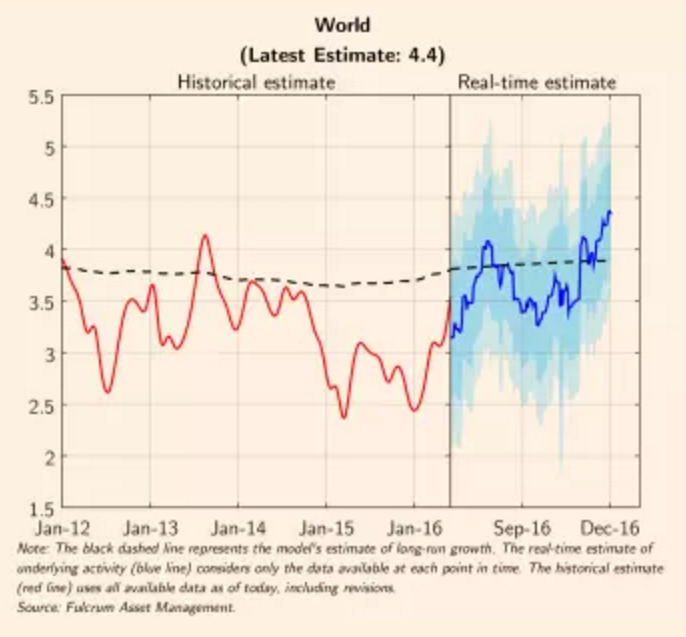

At the turn of the year, there were forecasts of global recession in 2016. At the low point for activity and risk assets in 2016 Q1, the global growth rate (according to the Fulcrum “nowcasts”) had dipped to about 2 per cent, compared to a trend growth rate of 4 per cent. It was a bleak period. The dominant regime in financial markets was clearly one of rising risk of deflation.

Since then, however, there has been a marked rebound in global activity, and in recent weeks this has become surprisingly strong, at least by the modest standards seen hitherto in the post-shock economic recovery. According to the latest nowcasts, the growth rate in global activity is now estimated to be 4.4 per cent, compared to a low point of 2.2 per cent reached in March.

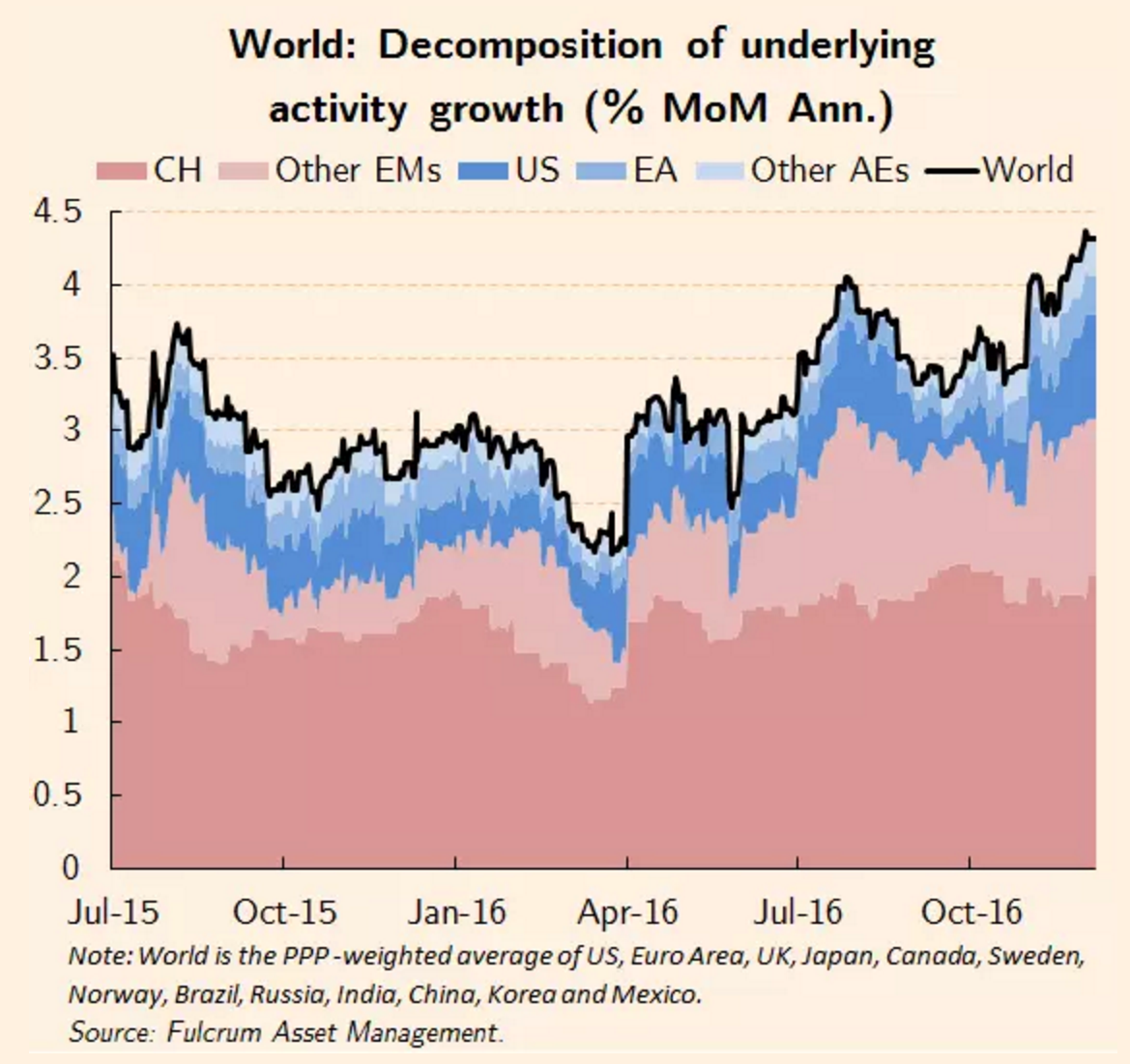

…We can use the nowcasts to calculate the numerical contributions made by each of the major geographical regions to global growth [1]. Here are the results:

Based on PPP weights, China alone is contributing almost half of the total growth in the world economy, with the other emerging economies contributing a further quarter. That leaves about a quarter coming from the AEs, of which more than half stems from the US. Europe and Japan are making a negligible contribution to global growth at the present time.

…Attempts to forecast inflexion points in global activity a year or two ahead are not very accurate. Having said that, there are some reasons for optimism that the firmer tone currently identified in the nowcasts might persist during 2017.

As noted above, the main reason for the recent uptick in global growth has stemmed from the EMs, notably from the major easing in fiscal policy in China, and the flattening in deep recessions in Russia and Brazil. The main downside risks to growth prospects in the EMs are a return to tighter credit control in China and an outflow of capital as an aggressive tightening in Fed policy pushes the dollar higher. These risks need to be watched, but do not seem imminent.

In the AEs, fiscal policy is being eased, monetary policy is still accommodative and the manufacturing sector is gaining from firmer corporate investment as the energy shock dissipates. These developments may lead to an upgrade to growth forecasts in the AEs for the first time in many years, provided that a major shock to confidence can be avoided from a shift towards populism in elections in the Eurozone next year.

Overall, we can perhaps be hopeful, though certainly not yet confident, that the global economy will begin to overcome the powerful forces of secular stagnation next year.

China is now the key driver of global industrial cycles. I expect it to slow into the H1 2017 but hold up. The big question will arrive in October 2017, post Communist Party Congress, and whether China’s new emperor will return to reform. I still think so.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.