Some good material from the sell side today helps us flesh out the scenario. From SocGen via FTAlphaville:

In fact, nearly 37 percent of China’s exports to the US in 2015 consisted of value-added imported from other countries (Figure 3). Redistributing the imported value-added to their original source countries gives a very different deficit decomposition picture for the US (Figure 4).1 While China still has the biggest “responsibility” for the US’s trade deficit, its share is only 16.4 percent. It is nowhere near the jaw-dropping 49.6 percent in Figure 1, which is about the combined share of the top 4 surplus partners (China, Japan, Germany and Korea) in the value-added based decomposition. Taiwan, previously not among the top 10 surplus partners in Figure 1, now ranks no. 6, accounting for 6.6 percent of the US’s trade deficit in 2015.

So, a trade war with China is also one with China, Japan, Germany and Korea!

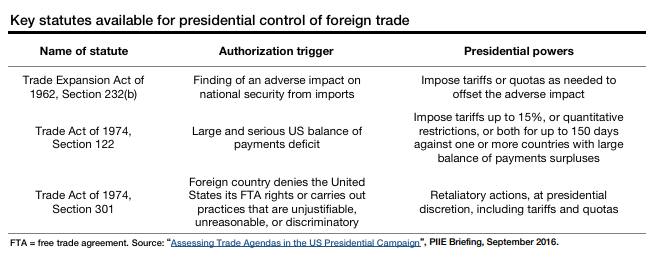

Deutsche reckons “the US would have three objectives: (i) reduce trade deficit; (ii) boost growth, and (iii) “bring jobs back” (in the President-elect’s own words).”:

Advertisement

Advertisement

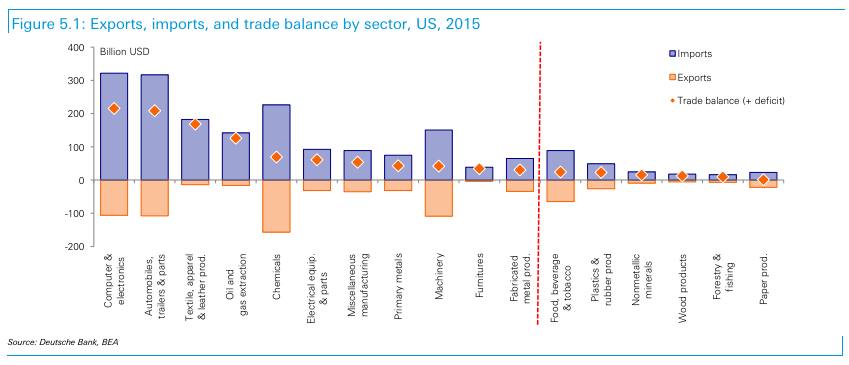

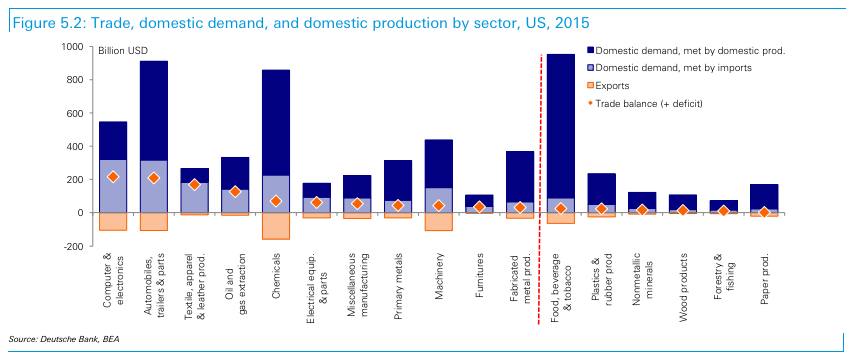

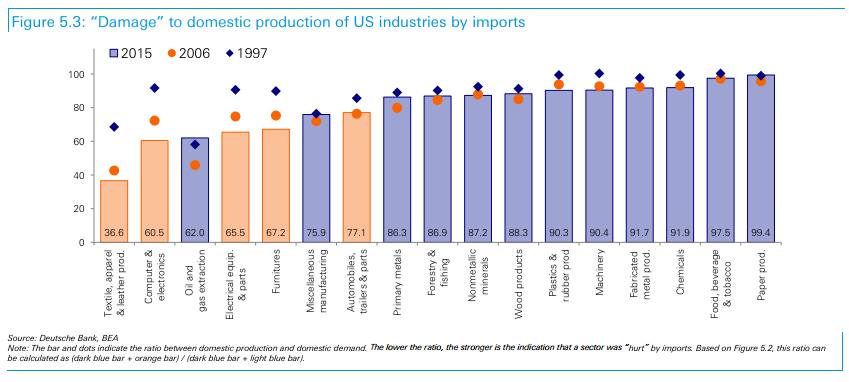

Thus “ Computer and electronics; Automobiles, trailers and parts; Apparel, leather and allied products; Electronic equipments and parts; and Furniture” are the likely targets.

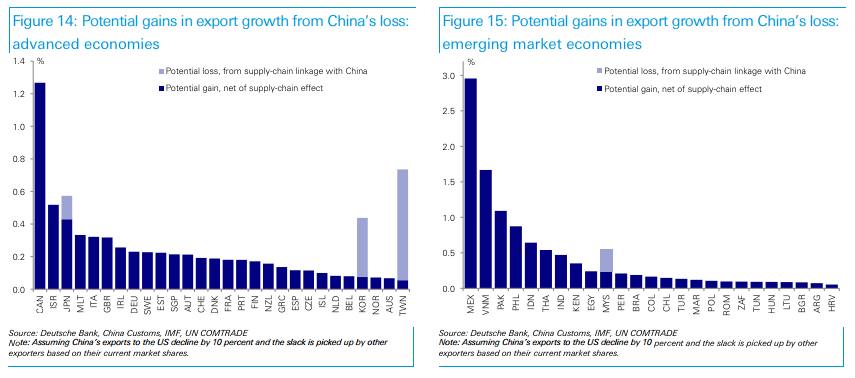

Around the world, who would pay the highest price and who would win?

Some might wonder the overall impact of a US-China trade war on other countries, considering both the positive and negative implications at industry level. To shed some light on this, we conducted an simple “experiment”, perhaps an over oversimplified one:(i) suppose China’s exports to the US decline by 10 percent across the board as the result of a trade war; (ii) assume the slack (China’s export decline) is picked up by other exporters to the US, and the split follows exactly their current market shares; (iii) consider the damage from supply-chain linkage with China (without second round effect) for, and only for, Korea, Taiwan, Japan and Malaysia; (iv) holding everything else constant, calculate the impact on a country’s overall exports. The result of this experiment is illustrated in Figures 14 and 15

Advertisement

And what would China respond with?

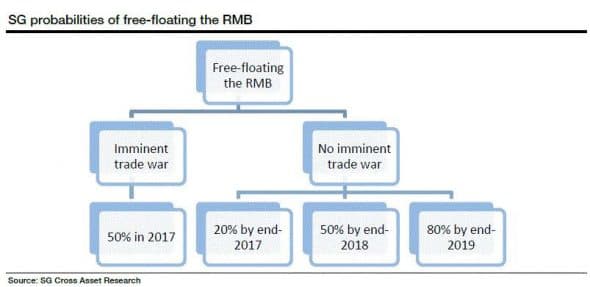

Many analysts also think China would let the yuan sink, SocGen among them:

If the US were to engage, or credibly threaten, trade restrictions on China (a label of currency manipulator or punitive tariffs on a wide range of goods), the probability of a free floating RMB in 2017 could be as high as 50%. Given that China has a reasonably strong external position (current account and net international investment position), a freefloating regime is unlikely to cause the RMB to fall more than 20% from current levels (i.e. USD/CNY 8.60 should be the upper bound of depreciation)

Advertisement

But that seems to me very unlikely. China is caught in the early stages of a financial crisis as it braves the impossible trinity, that a country can only choose two out of the following three:

control of a fixed and stable exchange rate

independent monetary policy

free and open international capital flows

China has been trying to run this gauntlet by sustaining an overly high growth rate via loose monetary policy and recently liberalised capital markets plus exchange rate. But it can’t have stability in all three and so is in full reverse on the last two to prevent a currency rout. If it let that last one go then it’s local credit conditions are likely to tighten to the point of strangulation. Indeed, if crisis outflows eventuated then it may well be forced to go entirely the other way and close its capital account.

Advertisement

No, it would counter with a few punitive tariffs is all.

Which means it may be worthwhile for Donald Trump. Indeed, if he is of a mind to use it, it may be a quite handy way to retard Chinese development.

If it were to happen then the fallout for Australia is pretty obvious. Sell it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.