As folks start blathering about bottoms in Australian interest rates, I thought it was time to again assess where the Australian zero bound is, given that’s where we’re very likely going.

I have long argued that because we run an externally funded little economy, the Australian zero bound is not actually at zero. That is, we’ll need to preserve some carry uplift or our cost of funds will soar or the currency collapse or both. For several years now we’ve assessed that at 50bps.

With US interest rates now rising, however, that lower bound is also rising, given the point at which capital decides we’re not such a good risk will also be higher, so let’s run some scenarios.

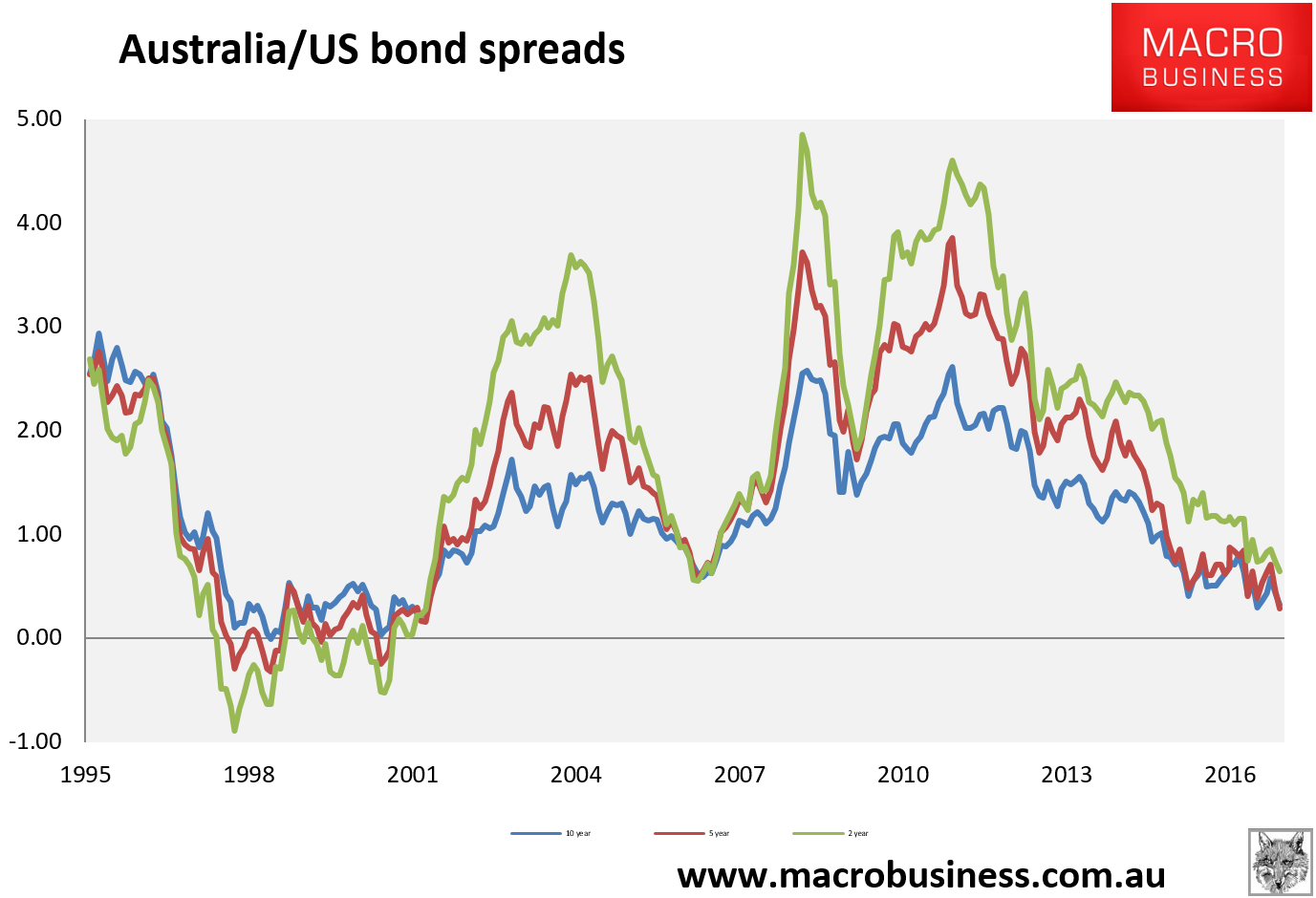

Here’s the recent history of the US-Australian yield spread (which hit new lows overnight):

The Fed is proposing to hike three times next year. Twice seems much more likely to me (and at some point soon it’ll be one too many) but let’s stick with the FOMC. By year end 2017 the US two year bond will yield 1.5% if it doesn’t see the need to discount any further hikes (which it may). If Backbone Phil cuts twice here then the spread on the two year bond will be -81bps.

The absolute bottom in modern negative yields for the Australian spread was -89bps in late 1997 during the Asian Financial Crisis. The Aussie dollar was trading in the mid-to-low 60 cents range.

Later, in 2001, the dollar was at 47.5 cents when the spread was -50bps.

This tells you that there is no fixed zero bound above zero. Not until markets tell you that you are there by gutting your currency to the point where you have an inflation problem. It is contingent not absolute and will rely upon myriad factors including:

- relative global growth orientations;

- commodity prices;

- wider spreads;

- sentiment;

- fiscal position.

And on it goes.

What we can say for now is that with the Aussie dollar still trading in the mid-70s, the yield spread having plumbed much lower levels previously without crisis, the terms of trade still at nosebleed levels and China still considered sound enough by markets, there is no reason to not expect multiple further rate cuts yet.

And a much lower Aussie dollar.