From the cowardly S&P:

The number of delinquent housing loans underlying Australian prime residential mortgage-backed securities increased in October from the previous month, according to a recent report by S&P Global Ratings. It was the second consecutive month in which mortgage delinquencies bucked the cyclical trend of falling arrears between April and November.

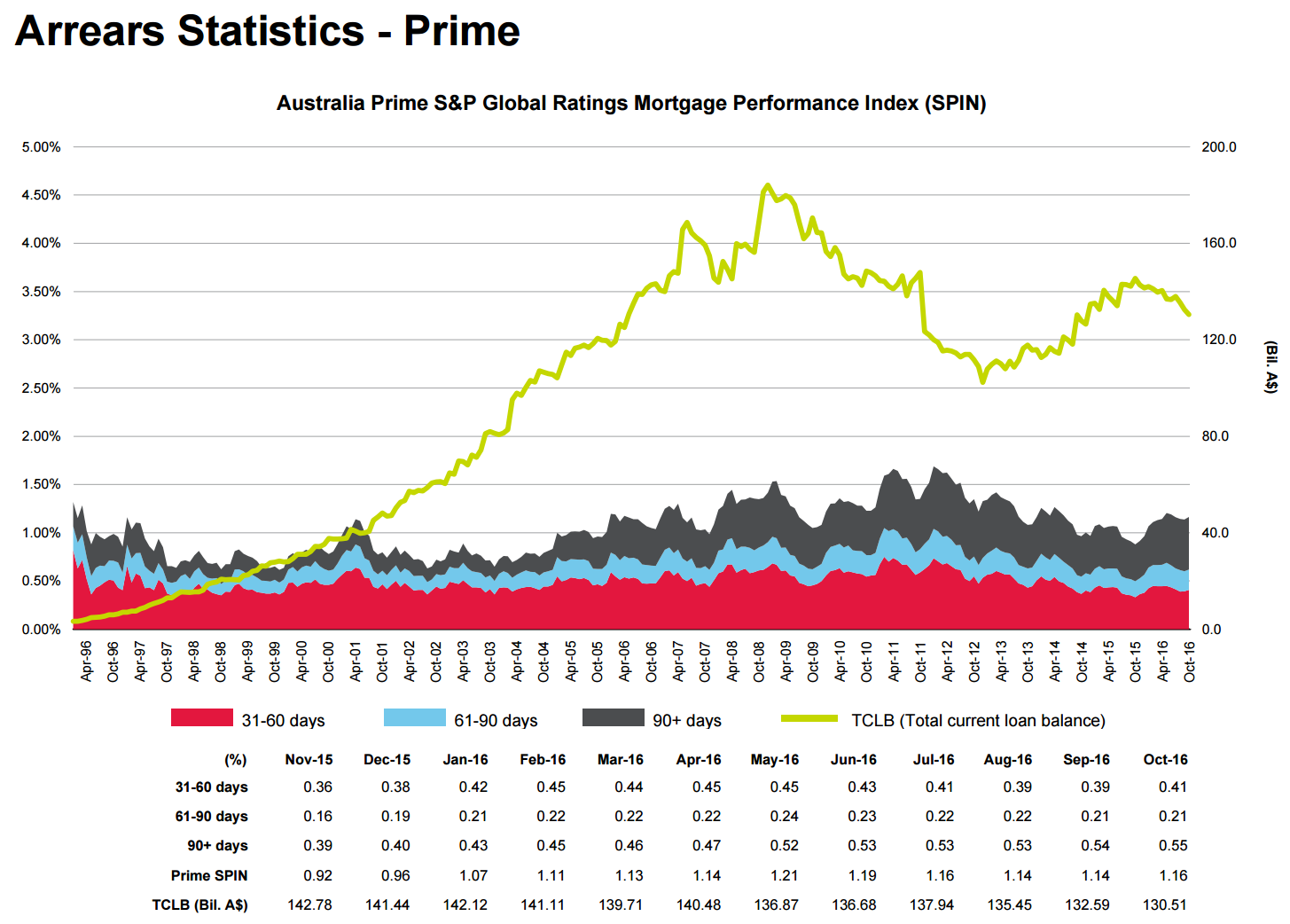

A total of 1.16% of the mortgages underlying Australian prime RMBS were more than 30 days in arrears in October, as measured by Standard & Poor’s Performance Index (SPIN), up 2 basis points from September. It was the first month-on-month increase in October since 2011, when arrears–and interest rates–were at higher levels.

Mortgage delinquencies are up year on year, but 2015 and 2014 were a period of historically low arrears. Arrears were below 1% during the third and fourth quarters of 2015; a level not seen since 2005. However, arrears now have started to rise, even while interest rates remain low and the unemployment rate is relatively stable. While arrears remain below their peak and 10-year average, mortgage stress is apparent in parts of the country.

The SPIN for nonconforming loans meanwhile fell in October to 3.99%, its second-lowest level, from 4.36% in September. The decline is partly due to an increase in loan balances outstanding, but the overall improvement during the past four years reflects the better collateral quality of nonconforming portfolios with a greater proportion of full-documentation loans and near-prime loans in current outstanding nonconforming transactions.

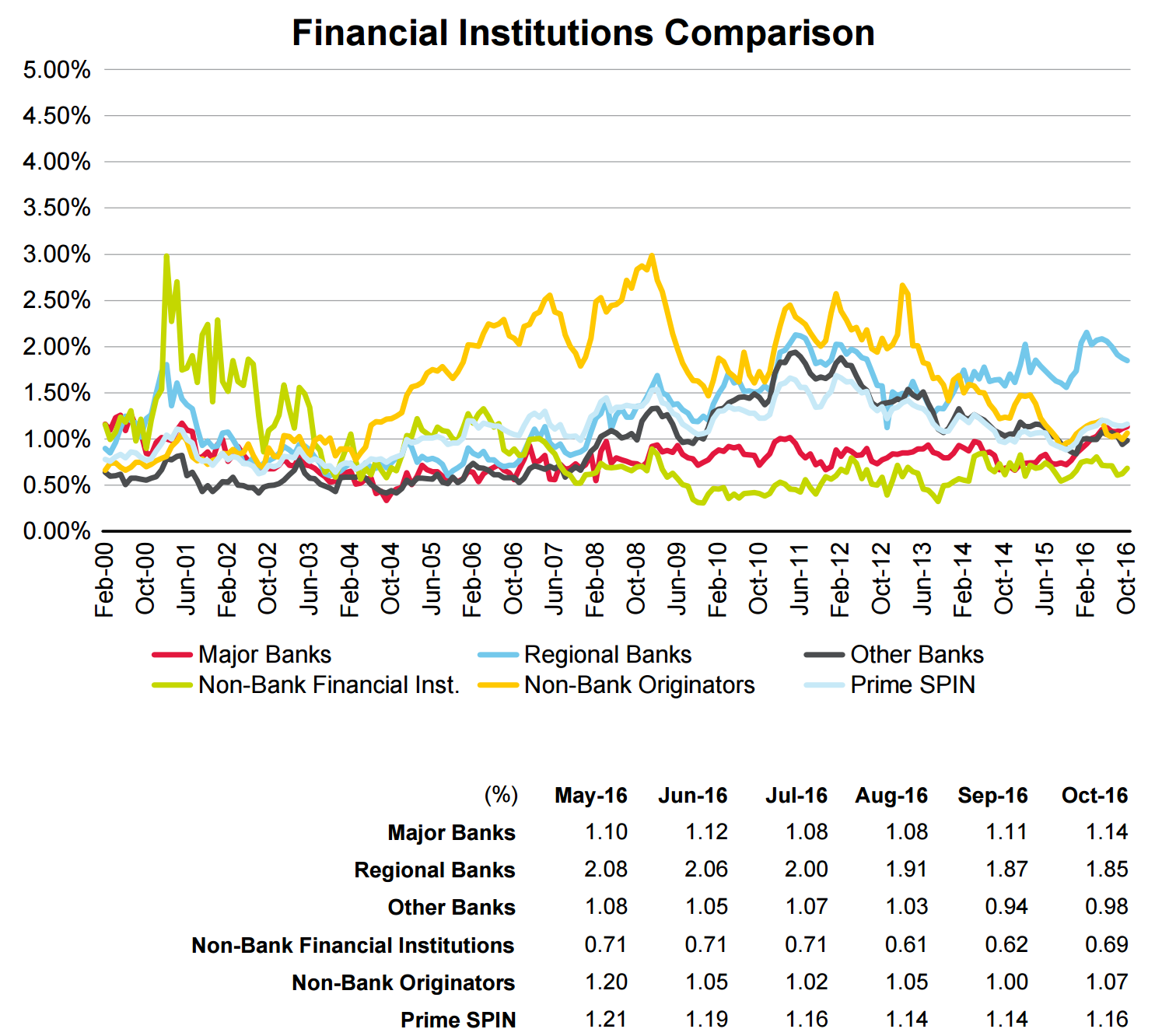

Arrears increased month on month in October for most originator categories except regional banks, which recorded a decline to 1.85% from 1.87% in September. Nonbank financial institutions continued to have the lowest arrears, at 0.69%, followed by other banks, at 0.98%, and nonbank originators, at 1.07%. Major bank arrears increased to 1.14% in October from 1.11% in September. Nonbank originators have recorded the greatest improvement in arrears during the past five years, falling 60% from a five-year peak of 2.67% to 1.07% in October, despite falling loan balances. Loans more than 90 days overdue at major banks accounted for more than 48% of their total arrears in October, up from around 40% a year earlier. This was the largest movement in the advanced arrears category.

The markets currently expect increases in mortgage rates, and we believe this would result in an increase in home loan arrears because most of the loans underlying Australian RMBS portfolios are variable rate.

Rates will fall not rise. The charts:

Another unseasonal rise. I’ll be looking for a goodly spike in the New Year. It was driven by majors:

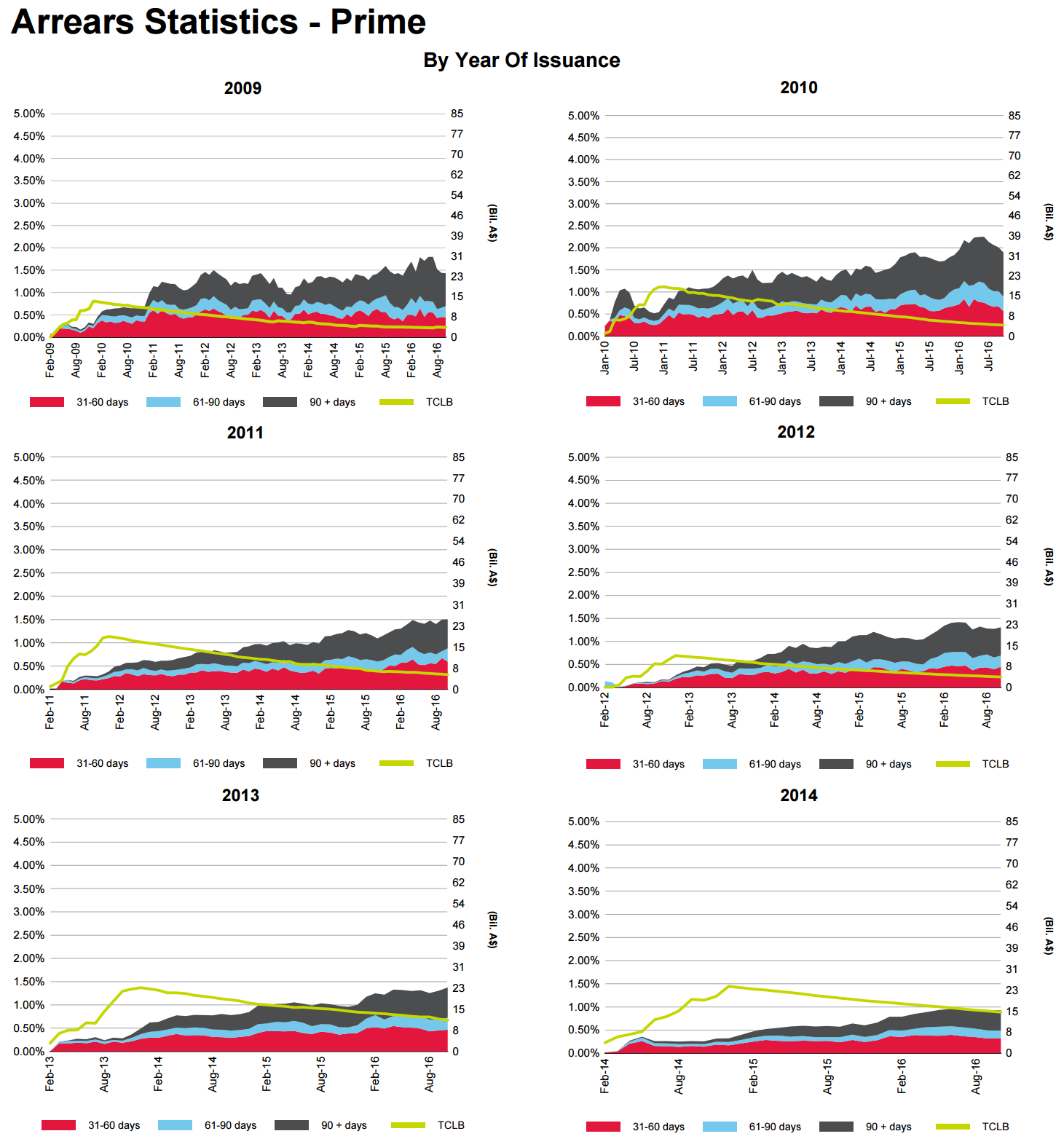

And the 2013/14 buckets:

Which says to me WA bust.