From David Uren today:

Credit ratings agencies are warning they will not accept forecasts they consider unrealistic in next week’s budget update, with one predicting weaker growth will push the combined level of federal and state debt about $50 billion higher this financial year.

…A contested area is the backlog of unlegislated measures, such as the wait for the dole and cuts to family tax benefits, that are blocked in the Senate and which the Treasurer said yesterday were pivotal to restoring the health of the budget.

“We have to get the budget back to balance and that requires passing what’s almost $20bn of other savings measures and improvement measures between now and the budget,” he said.

While the mid-year economic and fiscal outlook, to be released on Monday, will assume all these measures are passed and bring a steady improvement to the deficit, ratings agencies will be more critical. Moody’s senior vice-president for sovereign ratings Marie Diron told The Australian: “We look at the various measures being proposed, at the likelihood of them being implemented, and at the likely impact on the economy and on the government’s budget, starting from what is in the budget or the update.”

S&P is believed to share Moody’s expectation that the budget update will include some deterioration in the outlook after the economy contracted by 0.5 per cent in the September quarter, despite a surge in prices for Australia’s key export commodities this year.

Ms Diron said Moody’s expected the process of narrowing the budget deficit would be slower than the government had projected in the budget. “We expect slower nominal GDP growth that will translate into lower revenue for the government and with not much room for manoeuvre for spending cuts,” she said.

“What we do expect is the continued narrowing of the deficit.”

It’s pretty extraordinary stuff when a ratings agency – the doyen of global liars – has to warn the Australian treasurer not to lie in his outlook. But, then it is right to do so. Despite the incredible jump in the terms of trade, the real story here is that despite the huge windfall from commodity prices the Budget remains exceedingly optimistic. Here’s how it stands after one quarter:

| Budget | Actual | |

| GDP | 2.5 | 1.8 |

| Household consumption | 3 | 2.5 |

| Dwelling investment | 2 | 7.2 |

| Business investment | -5 | -8.5 |

| Private demand | 1.5 | 1.5 |

| Public demand | 2.25 | 4.8 |

| Net exports | 0.75 | -0.2 |

| Nominnal growth | 4.25 | 3 |

| CPI | 2 | 1.3 |

| Wage price index | 2.25 | 1.9 |

| Unemployment rate | 5.5 | 5.6 |

| Terms of trade | 1.25 | 15 |

What is holding the Budget together is the terms of trade explosion which is, in turn, being recycled as fiscal stimulus. Growth, income and investment are very likely to miss. Dwelling investment may do a bit better than forecast but remember that it will diminish sharply from here.

The terms of trade explosion will retrace in 2017 as China unwinds the policy error and slows at the margin. Morrison will probably leave iron ore at $60, lift thermal and especially coking coal. That will still give him a healthy boost without appearing too stupid.

He may pretend that other economic measures will lift following the ToT but they won’t. This is a profits and Budget receipts boom only. It will bi-pass the real economy. Even so, he could get away with that.

His real problem is the forward estimates. The terms of trade will resume falling and thus the acceleration embedded in 2017/18 is extremely dubious as the dwelling investment boom rolls over and sucks domestic demand down with it:

| Budget | MB | |

| GDP | 3 | 1.5 |

| Household consumption | 3 | 2 |

| Dwelling investment | 1 | -5 |

| Business investment | 0 | -1 |

| Private demand | 2.5 | 1.5 |

| Public demand | 2 | 5 |

| Net exports | .75 | .75 |

| Nominal growth | 5 | 2.5 |

| CPI | 2.25 | 1.5 |

| Wage price index | 2.75 | 1.8 |

| Unemployment rate | 5.25 | 6 |

| Terms of trade | 0 | -15 |

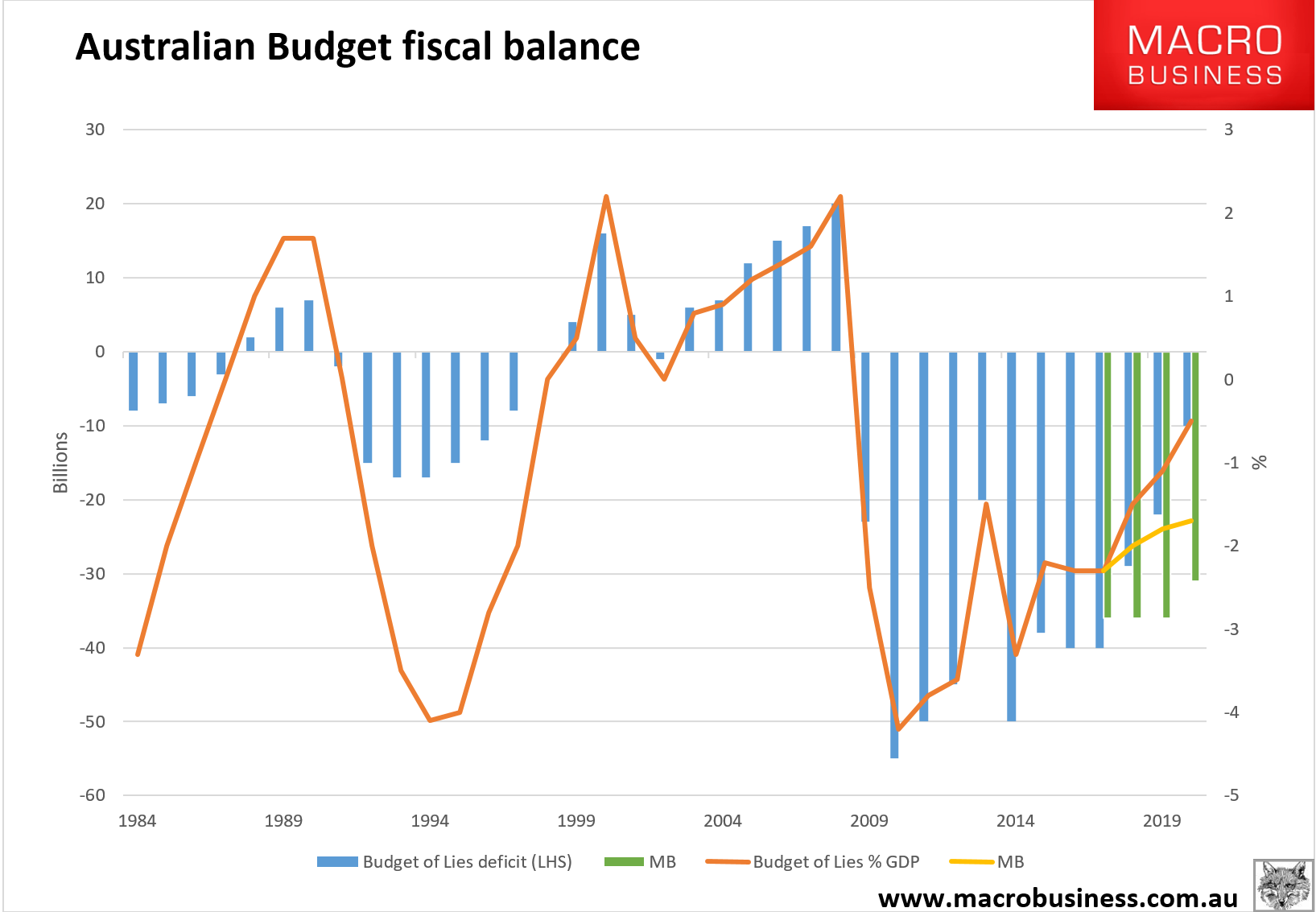

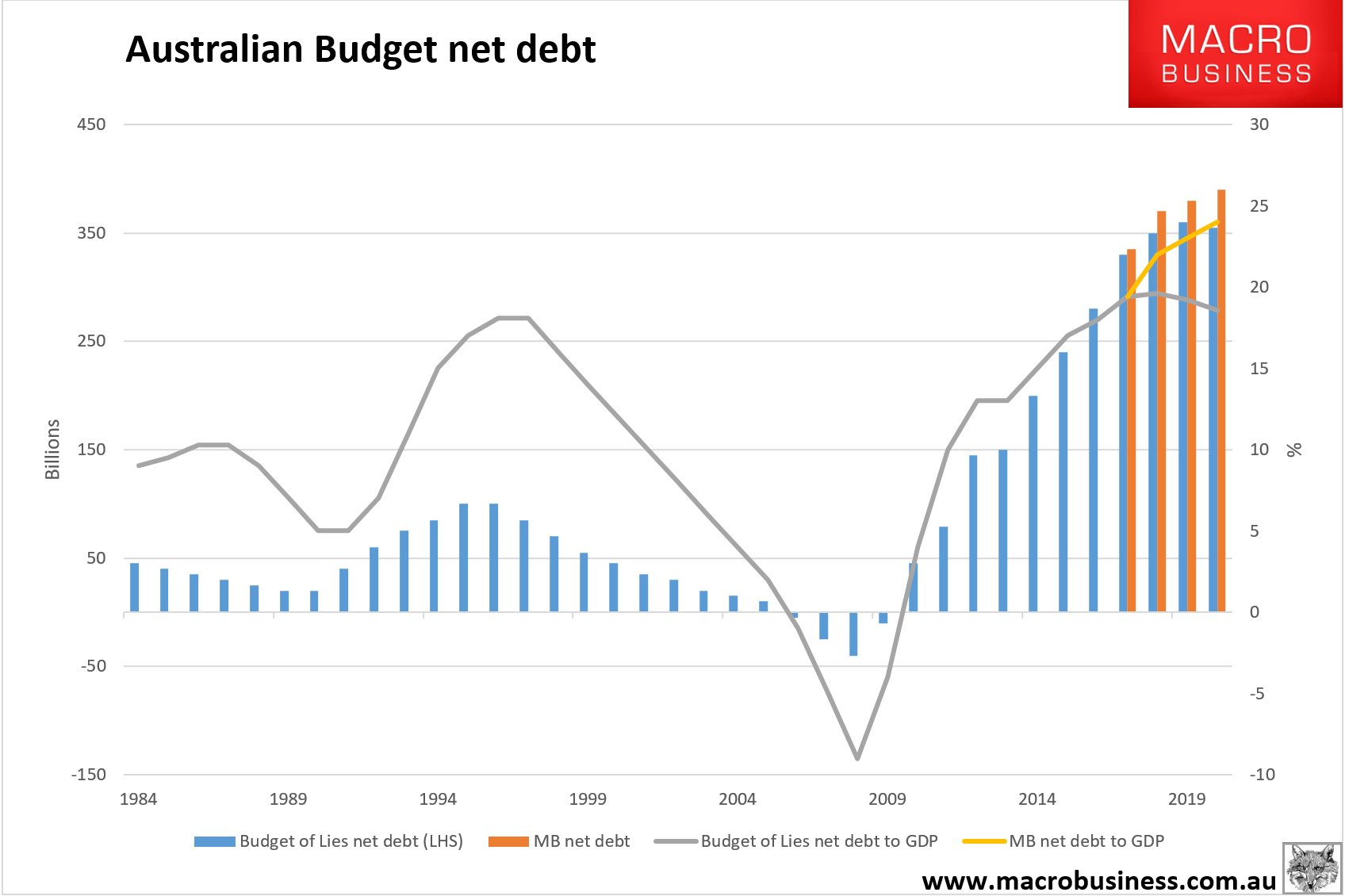

There really is only one driver of growth ahead and that is government spending, at least until the dollar falls so low that a decent tradables rebound gets underway. For us this looks like this:

So, will ratings agencies give Downgrade Morrison one more chance? I wouldn’t but Moody’s doesn’t even has us on downgrade watch so what can it do with more round of lies anyway?