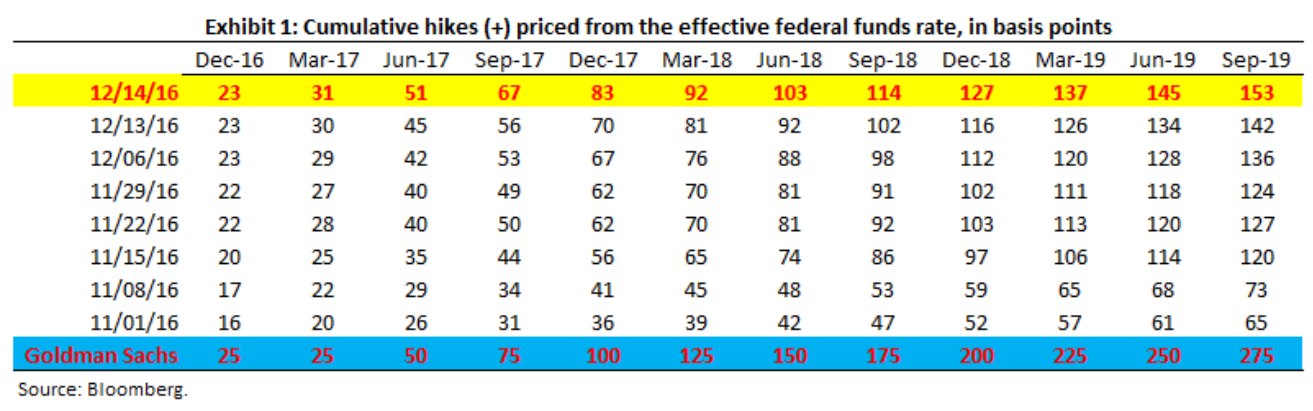

1. Ahead of today’s FOMC meeting, we argued that front-end interest rates, even with the sharp repricing since the election, were underpricing the changed circumstances since the election (“Less “Room to Run” for the Fed”, Global Markets Daily, December 14, 2016). As of yesterday, the market was pricing 70 bps cumulatively through end-2017, including the 25 bps hike that we got today. This meant that the market was still pricing less than two hikes for next year, i.e. too low of a risk premium relative to the one hike per year that has now occurred in 2015 and 2016 (Exhibit 1). It seemed to us that the market should have – at the very least – been pricing between two and three hikes for next year and we revised up our $/JPY 12-month forecast ahead of today’s FOMC. In the event, the dot plot showed a rise in the median “dot” for next year from two to three hikes, with four “dots” moving from two hikes or below to three hikes, a solid move that almost certainly leaves at least some of the FOMC leadership with a three-hike baseline (“FOMC Raises Rates, Officials Increase Pace of Hikes for ‘17”, USA, December 14, 2016). In the event, the dot plot also revised up the long-run median target rate to three percent, a number that had been cut to 2.875 as recently as the September meeting when the low R-Star debate was still in vogue. The press conference on balance validated our view that today’s FOMC would mark a turning point, with less “room to run” for the Fed and its repeated moves to scale down the tightening cycle. This FX Views briefly reviews today’s price action and discusses the Dollar trajectory going forward, which we see as tightly linked to how risk appetite and escalating RMB devaluation expectations evolve in the period ahead.

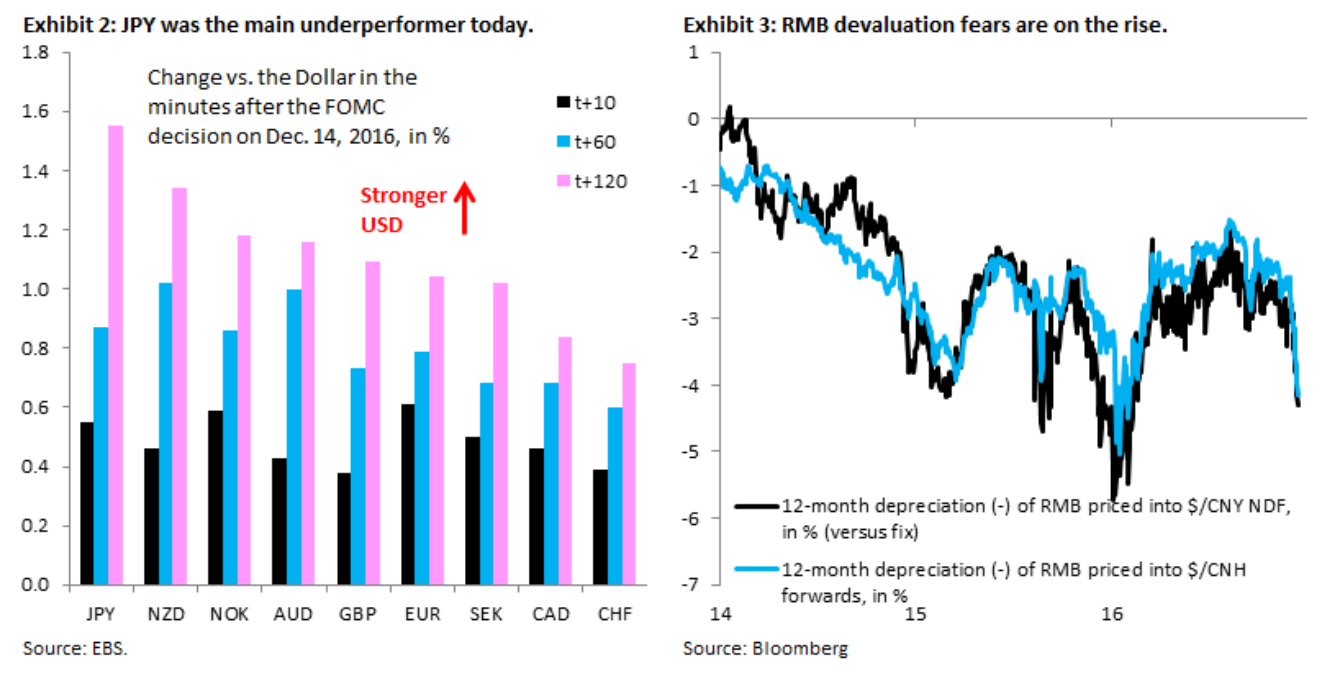

2. In the G10, today’s main underperformer versus the Dollar was the Yen (Exhibit 2), reflecting the clarity of the BoJ policy framework in a setting of rising global interest rates. We continue to see Yen underperformance ahead, with our forecast at 118, 120 and 125 on a 3-, 6- and 12-month horizon. We also see EUR/$ falling, though the ECB decision to taper purchases at last week’s meeting in our view translates into a less rigid anchoring of Euro zone interest rates, so that we believe that EUR/JPY should continue to move higher. While the market has turned its back on GBP/$ downside for the moment, amid conflicting messages over soft versus hard Brexit from UK government figures, we believe GBP/$ downside remains one of the main themes for early next year, as triggering Article 50 moves back into focus. Our short GBP and EUR top trade versus USD remains very much a theme for the coming year, in our view. Today’s developments obviously argue for $/CAD higher and this remains our bias as well. But the cross-currents from higher oil prices mean that this is less compelling in terms of direction. We continue to see AUD/CAD lower as policy normalization and fiscal stimulus in the US benefit Canada more than Australia.

3. Coming days will show how risk appetite digests this Fed meeting. In addition, RMB devaluation fears had been on the rise even ahead of today, something that may further escalate in coming days. Our short RMB top trade is already halfway towards its target and we see potential for this repricing to continue in the short term (Exhibit 3). In our view, Chair Yellen in the press conference did a good job threading the needle between acknowledging a more hawkish policy backdrop, given the prospect of fiscal stimulus in an economy operating close to capacity. She repeatedly stated that the degree of policy accommodation is low, her way of saying that the pace of tightening will remain contained. The biggest risk at this juncture in our view is that markets get ahead of themselves and push the Dollar much stronger in short order, which could cause capital outflows from China to pick up further and once again destabilize the RMB and global risk appetite. Our bias remains for an orderly move higher in the Dollar, but an escalation of China fears and a repeat of the risk sell-off in Q1 of this year are the main risks to our outlook.

Recall the impossible trinity, that a country can only choose two out of the following three:

control of a fixed and stable exchange rate

independent monetary policy

free and open international capital flows

China has been trying to run this gauntlet by sustaining an overly high growth rate via loose monetary policy and recently liberalised capital markets plus exchange rate. But it can’t have stability in all three and so is in full reverse on the last two to prevent a currency rout.

If you ask me, it’s pretty obvious that, if pressed, China will shut its capital account before it lets the breaking trinity disrupt local credit (which would destabilsie politics) so the asset price implications globally are not so much a Chinese financial crisis as they are a bubble bust for anything reliant upon the outwards flow of Chinese capital. That includes residential and commercial property in “global cities” worldwide and reserve currency bond markets worldwide. It might also include commodities though that question is complicated by the Chinese rush to buy futures as a yuan hedge. Then again, they would surely crash anyway if China were forced to shut its capital account.

This remains a tail risk. More likely, China will pop the commodities futures bubble and take pressure off inflation for everyone worldwide, and give the Fed more time. But the risks are rising.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.