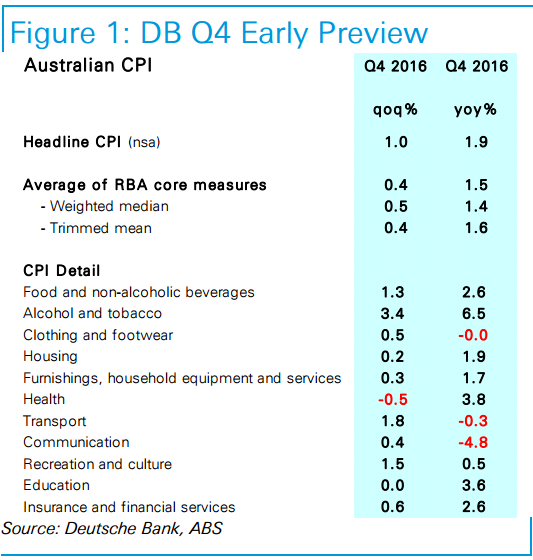

Our early pick for Q4 CPI is for a strong headline print of 1.0%qoq, leaving headline CPI at 1.9%yoy. We expect core CPI to remain soft however, at 0.4%qoq to be up 1.5% in year-ended terms. (We will refine our estimate once the full suite of price indicators becomes available in mid-January.)

The table at right details our forecasts. Broadly speaking, there are three main drivers of our relatively strong headline call for Q4. First, the 12.5% increase in tobacco excise from 1 September, which we estimate will lift the average retail tobacco price across Q4 by around 7.5%qoq compared to the average price that prevailed across Q3. Second, we estimate retail petrol prices have risen by about 6.6% in the quarter, following a fall of 2.9%qoq in Q3. Finally, early indications are that fruit and vegetable prices have actually increased a little further in the December quarter after a strong rise in Q3 (i.e. we are not yet seeing any mean reversion). The ABS noted in Q3 that fruit and vegetable prices had been impacted by significant flooding across major growing areas. We are not surprised then that prices have shown some resilience into Q4, given that it will likely take more than a quarter for more normal supply conditions to resume.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.