The last time China faced the threat of significant outflows in the mid-1990s, it did not utilize capital controls, in part because it had much tighter controls to begin with. Now is a different story.

Only in the past two months, we see regulators shoot four times, the goal is clear, cut off the capital outflow through black channels: in October, UnionPay cut off Hong Kong insurance payment channels; November, bitcoin, huge foreign investment projects, Shanghai Free Trade Area strengthen the review of overseas investment channels. Almost all the central bank’s big news are related to combat capital outflows.

We then lengthen the timeline, you will find that from the end of last year to stop some of Deutsche Bank’s foreign exchange business, to November this year, the RMB exchange rate fluctuations every time, are accompanied by capital outflows warning and regulators war.

Regulators are so battle ready for capital outflows with rarely seen power, even in the mid-1990s when China faced a serious capital outflow, that was not the case.

This “capital outflow sniper war” continues, however, it can be said that results are slowing in the last six months: in the first stage, monthly outflows fell about $50 billion, and the last seven months were reduced by about $10 billion.

Why launch a war now? Some numbers to put the situation in context:

However, it is unexpected, accompanied by the overseas investment surge, the speed is almost out of control. Reflected in the foreign exchange reserves, in June 2014 reached its peak and after a sharp turn, two years later it has dropped dropped by $870 billion.

What is the concept of $870 billion? The total resources of the IMF total $660 billion. During the entire Southeast Asian financial crisis, the world’s foreign exchange reserves fell $350 billion, and in two years, China’s foreign exchange reserves shrunk by more than 20%. Is not difficult to foresee, if left alone, 10 years later the foreign exchange reserves would be dismal.

Reserves have already declined by more than in 1997 on a percentage basis and there hasn’t been any crisis yet.

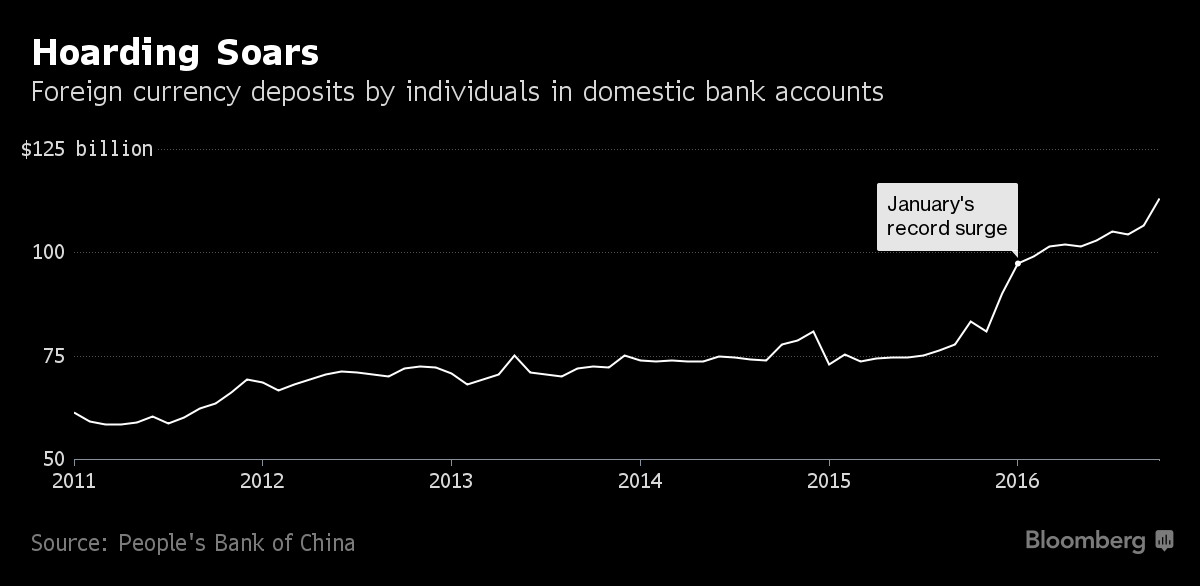

People’s Bank of China Governor Zhou Xiaochuan already has one policy headache with the currency falling to near an eight-year low. He could have an even bigger one next month.

That’s when a $50,000 cap on how much foreign currency individuals are allowed to convert each year resets, potentially aggravating capital outflow pressures that are already on the rise. If just 1 percent of China’s almost 1.4 billion people max out those limits, that’s an outflow of about $700 billion — more than the estimated $620 billion that Bloomberg Intelligence estimates indicate has already flowed out in the first 10 months of this year.

Middle class and wealthy Chinese have been converting money into other currencies to protect themselves from devaluation, exacerbating downward pressure on the yuan. Outflows could intensify if Federal Reserve interest-rate hikes fuel further dollar appreciation.

That leaves Zhou in a bind identified by Nobel-prize winning economist Robert Mundell as the “impossible trinity” — a principle that dictates nations can’t sustain a fixed exchange rate, independent monetary policy, and open capital borders all at the same time.

“At a moment like this, you have to compare two evils and pick the less-worse one,” said George Wu, who worked as a PBOC monetary policy official for 12 years. “Capital free flow may have to be abandoned in order to maintain a relatively stable currency rate.”

Advertisement

Quite right. But who said it is a “moment”? What is going to stop it? Nothing that I can see. So long as the US dollar is in a bull market it will get worse not better:

it leads developed market growth;

it leads developed market inflation;

it leads developed market tightening;

OPEC has just materially boosted all of the above, and

as this EM and China capital outflow develops, the USD will lead the world as a safe haven currency.

Advertisement

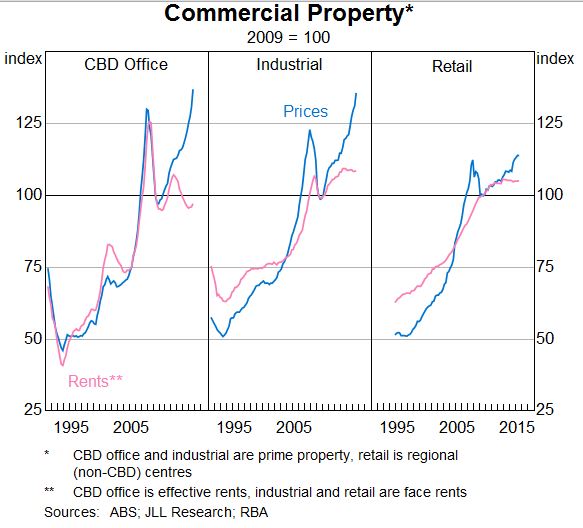

If you ask me, it’s pretty obvious that, if pressed, China will shut its capital account before it lets the impossible trinity disrupt local credit (which would destabilsie politics) so the asset price implications globally are not so much a Chinese financial crisis as they are a bubble bust for anything reliant upon the outwards flow of Chinese capital. That includes residential and commercial property in “global cities” worldwide and reserve currency bond markets worldwide.

That puts Australia’s Chinese apartment and broader commercial property bubble right in the path, with its grotesque overvaluations and poor rental returns:

Advertisement

It has already started. Apartment lot buyers are drying up, from Domainfax:

The total value of development site deals around Australia has suffered a steep 25 per cent decline in the year ending June 2016, according to Knight Frank research.

About $7.1 billion of high-density development sites changed hands during the 2015-16 year with foreign buyers buying 46 per cent of the property in Sydney, Melbourne, Brisbane, Perth and the Gold Coast, down from the previous year when they made up 51 per cent of the value of all purchases.

The decline in value appears to reflect a decline in available sites in key locations and comes as a clutch of property pundits, including the Reserve Bank of Australia, warn a glut of apartments is looming. New apartment and housing starts have also declined several months in a row, indicating a slowdown has started.

Which is why Australia’s “managed crisis” in new apartments is no such thing, from the AFR:

Advertisement

Developers are being forced to offer rental guarantees and extend settlement deadlines for newly built apartments, as lending restrictions on foreign buyers and a supply glut in Melbourne and Brisbane begin to bite.

In what has been described as a “managed crisis”, one Beijing-based real estate executive estimates about 10,000 Chinese buyers may struggle to complete apartment purchases.

Fears of steep price falls stemming from foreign buyers being unable to obtain finance has been a looming issue all year, but has so far failed to make a significant dent in buoyant property markets across the country.

Joseph Chahin, the managing director of property developer Peregrine Projects, said the issue had been kept largely under wraps by the industry, as developers seek to negotiate their way out of trouble.

“It is a managed crisis,” he said.

“This has smashed many developers’ return on investment. What was profitable is now borderline.”

While the overall Australian property market remains strong there are early signs of a pullback in Melbourne apartment prices, which fell 3.2 per cent in November from a month earlier, according to the Corelogic Hedonic Home Value Index released on Thursday.

David Wang, the vice-general manager for international sales at 5i5j, estimated Chinese buyers of Australian apartments had fallen 50 per cent in the second half of the year.

All crises are “managed” at the leading edge. Then they turn into crises for real. A one billion tonne juggernaut is bearing down on the Australian commercial property.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.